I live next door to a couple of car fanatics. One worked for more than thirty years as an engineer at an auto assembly plant, and the other owns a small manufacturing company. The vehicles in their driveway are never more than three years old, and they are meticulously maintained. If a neighborhood child hits one of them with a frisbee, insurance information is exchanged.

By contrast, I have a 13-year old clunker whose onboard navigation doesn’t include a number of roads which have been constructed during its lifetime. There is dirt on the exterior that could be considered “vintage.” It drives the neighbors crazy.

I’ve been considering getting a new ride for a while, but it hasn’t been the best time to be in the market for a car. The auto industry has been plagued by shortages that led to sky-high prices for new and used vehicles. While short-term limitations have eased somewhat, the sector finds itself in the middle of several long-term, secular evolutions. Cars provide a case study on several of today’s biggest economic cross-currents.

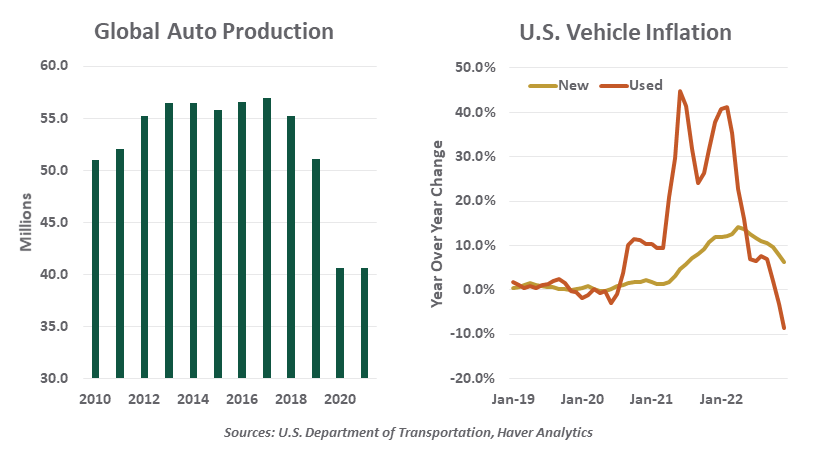

The pandemic had a seismic impact on vehicle production. The average car has 30,000 parts, which come from a range of suppliers. Value chains and assembly lines are organized to tight tolerances, which were deeply disrupted by COVID-19. Social distancing and worker absenteeism affected labor; shipping interruptions hindered the delivery of components to factories. Circuitry was a particular problem, as chip demand driven by the transition to remote work made it difficult for auto makers to secure allocations.

At the same time, demand for vehicles jumped. Commuters apprehensive about crowds needed conveyance, and low financing rates made payments more affordable. In the U.S., stimulus checks helped. The intersection of scarce supply and surging demand led to huge price increases.

Slowly but steadily, production friction has eased. Auto output is not yet back to pre-pandemic norms, but inventories have improved. An increased flow of new vehicles has also helped take the pressure off used car prices, and rising interest rates have taken some of the starch out of demand for both. Once a source of hyperinflation, the auto sector is now a leading contributor to disinflation.

Secular trends prompted by the pandemic are having lasting effects on vehicle demand. Hybrid work arrangements are reducing commuting for many (although those who continue to commute are more likely to drive). Reductions in business travel are limiting demand for auto rentals. The broad, negative impact of COVID-19 on demographics is affecting the number of drivers.

Auto production has recovered, but is still well short of pre-pandemic levels.

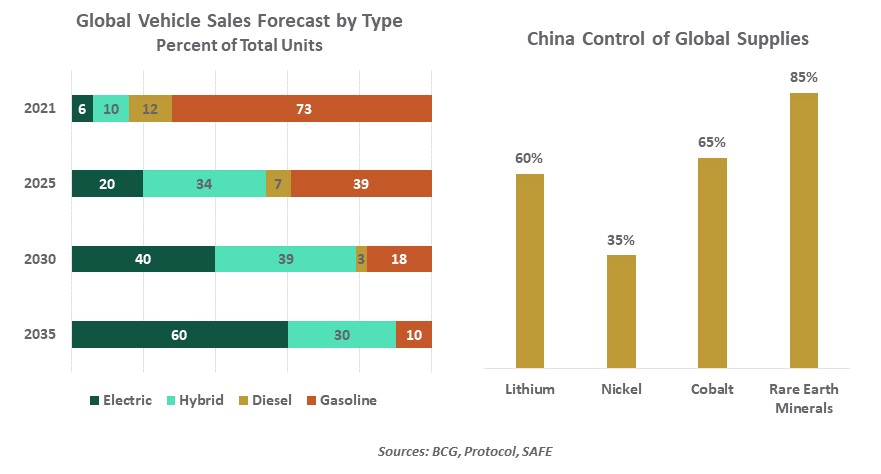

Two other long-running evolutions are also impacting the auto industry. The first is climate change, which has prompted additional demand for “greener” vehicles. Many areas around the world have adopted regulations or targets aimed at phasing into cars that have a more modest carbon footprint. The United States and Europe are engaged in a minor trade battle on this front, as each aims to gain the pole position in electric vehicle (EV) production.

The changing mix of car production presents both opportunities and challenges. Electric vehicles may look similar to their gasoline-powered brethren, but they have very little in common under the hood. Batteries are the most significant difference: the storage cells used in EVs are much larger and heavier, and they rely on raw materials that are not always near at hand. In recent years, China has made strategic investments around the world to secure control over a number of the basic metals and minerals that are critical to battery-powered propulsion.

There is also a chicken and egg situation surrounding EVs and charging stations. Motorists often cite “range anxiety” when considering the switch to a cleaner car, even though most trips are well within battery capacity. Government programs around the world are attempting to increase and improve the number of charging stations in operation.

Consumers have increasing interest in EVs, but availability is modest and prices are high. The average EV still costs $10,000 to $15,000 more than a traditional vehicle, although tax rebates and operating costs compensate for a lot of this differential during the car’s useful life.

Manufacturers of EVs also find themselves in the middle of debates among investors about how they fit into environmental, social and governance (ESG) models. The electricity required for power is almost certainly gentler on the atmosphere than burning fossil fuels in an internal combustion engine. But mining the minerals needed for vehicle batteries is a messy process, and some of the places that produce them do not follow the highest labor or environmental standards.

Electric vehicles are the future, but the road to get there could be bumpy.

Automakers are also on the front lines of the reshoring movement. Seeking to reduce dependence on Chinese suppliers, manufacturers are considering alternatives that are closer to their customers. A number of new chip fabrication facilities are under construction in North America, and exploration for new sources of critical raw materials has stepped up. North American makers stand to gain from geographic realignment, given existing supply chains and a free trade agreement among Canada, Mexico, and the United States.

The urgency of finding alternatives to Chinese supply escalated this month. The discovery of surveillance balloons above the continental U.S. provoked restrictions on technology sales to Beijing. In response, China has limited the export of technology essential to the processing of rare earth minerals. Instability of supply provides motivation to find alternatives.

The auto industry is not the only one having to navigate shifting conditions in trade, climate, policy, and tastes. But the elements faced by carmakers are among the most difficult that any industry has to face.

With prices moderating, I have resumed my search for a new car. The process is a little intimidating: the electronics on today’s vehicles are miles ahead of what I am used to. Maybe I will just keep my old clunker and sustain the satisfaction of annoying my neighbors.

© Northern Trust

Read more commentaries by Northern Trust