As fourth-quarter earnings rolled in with mixed results, the stock market opened the year in rally mode. Carrie King, Global Deputy CIO of BlackRock Fundamental Equities, weighs in with three observations for stock investors.

1. Inflation’s toll on corporate profits

Margins were the big concern leading into the Q4 earnings season as still-high inflation threatened to erode company profits. Strong post-pandemic consumer demand and limited supply had so far allowed companies to pass on higher input costs. But household spenders have their limits and inventories have swelled. Fourth-quarter results showed consumers balked at higher prices. Combined with elevated inventories at retailers, this painted a challenging picture for sales.

Overall, we observed the expected drop in margins, with the S&P 500 Index’s aggregate operating margin on a step decline since mid-2022. The current level is still above the 12.5% average of the past 30 years, but margin degradation shaved 10 percentage points from S&P 500 earnings growth in Q4, resulting in a mid-single-digits earnings decline.

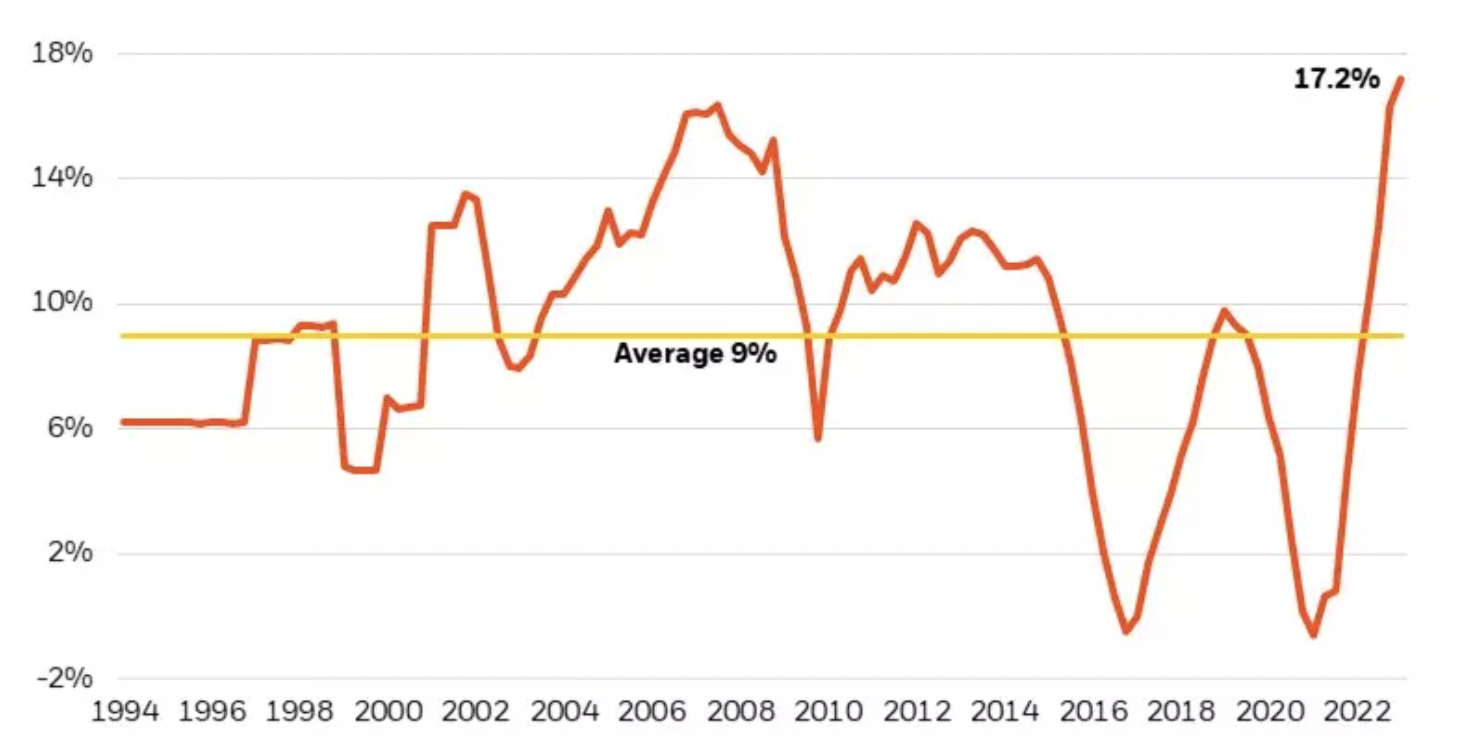

Margins were little problem for the energy sector, which saw operating income grow more than 50% versus Q4 2021. Profit margins for energy companies currently stand at a historical high, having notched their fastest rebound from trough levels in 30 years. See chart below. We continue to see opportunity in the energy sector even after stellar performance in 2022, but stock selection will be more important now.

Energy sector margins at an all-time high

Aggregate operating (EBIT) margins, 1994-2023

2. A ‘cloudy’ read on the economy

The three giants of the tech sector began to show weakness in their Q4 results. Together, Google, Amazon and Microsoft command roughly three-quarters of the cloud market and we find the soft results for all three to be a potential canary in the coal mine for the economy.

Why? The scale of usage is so broad that demand for cloud computing services is a good gauge of companies’ fiscal sentiment. While cloud offers long-term cost efficiencies to businesses across sectors, company managements also have the flexibility to rein in their usage when economic conditions appear challenged. Our global technology team expects to see cloud softness continue through mid-year, with potential for reacceleration in the second half.

Despite the slowdown in cloud spending and its potential economic inference, tech stocks notched early-year gains. We see two reasons for this disconnect: tech stocks had significantly underperformed in 2022, and markets have been cheered by cost cutting in the sector. We believe a sustained rally in technology requires demand growth to accelerate across the tech universe.

3. Readying for fundamentals to take the lead

Stocks’ early-year rally came amid hopes for declining inflation and a pause in Fed rate hikes ― even as earnings were largely ho-hum. The muted share price response for earnings beats and misses suggests that these macroeconomic factors remain the dominant driver of investor sentiment. In addition, over the past five years, we’ve only seen two quarters in which the frequency of positive earnings surprise was lower. And still, the market was up.

We expect the focus to shift from the macro picture to company fundamentals once greater clarity emerges around the Fed’s rate path. This, we believe, presages a positive backdrop for bottom-up stock pickers.

One area of emphasis across our global Fundamental Equities platform is healthcare, where positive earnings surprise was comparable to the market average yet the sector underperformed. Healthcare stocks look relatively inexpensive today and we see potential for performance upside given the sector’s history of recession resilience and a strong demand outlook amid aging populations worldwide.

© BlackRock

Read more commentaries by BlackRock