Central banks around the world have been raising short-term interest rates aggressively for almost a full year now. All of the tightening has, however, put central banks into a kind of hole.

Over the past 15 years, central banks have become some of the largest asset managers in the world. Portfolios accumulated under quantitative easing (QE) now total an estimated $44 trillion worldwide. For the Federal Reserve, the Bank of England (BoE), and the European Central Bank (ECB), holdings are entirely composed of bonds; elsewhere, central banks invest in a range of asset classes. The Bank of Japan, for example, owns more than 60% of the country’s exchange-traded funds.

The interest on central bank portfolios is used to pay the organization’s expenses, with any excess remanded to the host government. Over the last five years, the Federal Reserve has shared an average of $78 billion annually with the U.S. Treasury, while the BoE has forwarded £100 million annually to the British Treasury. Since last March, however, those positives have turned negative.

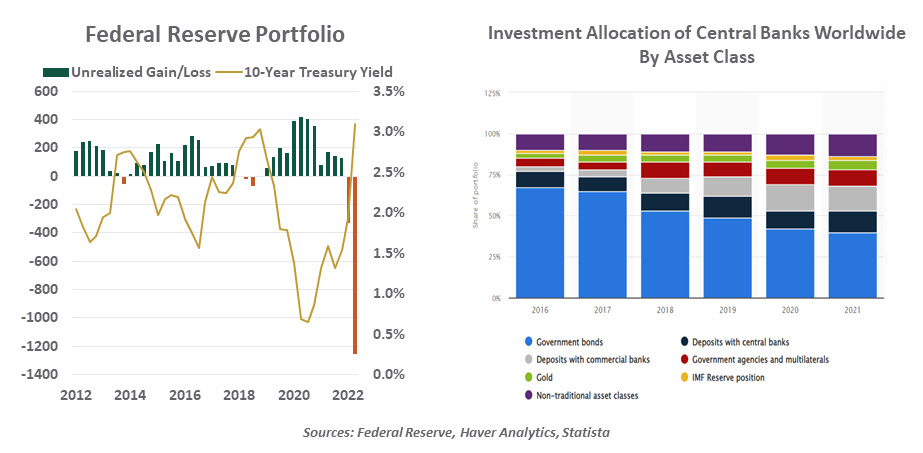

That’s what’s going on above the surface. In the background, last year’s falling asset prices diminished the market value of central bank portfolios. It is estimated that the Federal Reserve’s holdings are underwater by $1.3 trillion; the ECB’s positions are worth an estimated $800 billion less than their face values.

To be sure, these paper losses will only be realized if securities are sold. (Bond values converge to their face values as maturity approaches.) Many central bank portfolios are in runoff mode now, and the hope is that balance sheets can decline naturally. But if there is a need to accelerate balance sheet reductions, sales will be required. And that will trigger gains or losses.

The Federal Reserve has expressed an intention to maintain a Treasury-only investment portfolio, which would require the Fed to liquidate $1.5 trillion of mortgage backed securities which have very long maturities. Those bonds currently carry an unrealized loss of $431 million.

Central banks with more diverse holdings are more directly exposed to gains and losses. Their portfolios often have to be rebalanced to meet stated objectives, which can produce wide swings in results. The Swiss National Bank, for example, lost $143 billion last year. On the other side, the Bank of England took a tidy profit of £3.5 billion on securities purchased to stabilize the U.K. gilt markets last fall.

Central banks prefer to operate quietly in the background. They are guardians of financial stability, not creators of instability. When a central bank takes gains or losses, however, it raises a host of questions. How does a central bank choose which assets to own? Who oversees the investment activities, and what policies govern them? Do their choices favor some over others? Why should a central bank invest outside of its home market? Are taxpayers on the hook for losses?

There are good answers to all of these queries, and central banks should be providing talking points to all of their stakeholders. Addressing one in particular, any gains or losses generated by central bank investments go into the same account that is ultimately remanded to the Treasury. If the central bank is in a net deficit position, that amount is recorded as payable to the government in the future.

Losses, especially unrealized ones, are not a threat to the solvency of central banks. As owners of the printing press, they have a direct way of covering shortfalls. But depreciating portfolios could heighten calls for more checks on central bank independence. As the numbers escalate, so will the level of concern.

Ultimately, returns on central bank investments should be judged by their impact on economic activity, not portfolio returns. QE was initiated to provide liquidity during stressful times, and today’s unrealized losses are not unexpected. However, some will find it hard to look past the P&L.