While much attention has been focused on specific banks since the failure of Silicon Valley Bank (SVB), our challenge has been to project how the effects of SVB’s crisis could disrupt the broader economy. We can now see that skittish bank depositors are redirecting their money into short-term investment products, with uncertain implications for growth.

Money market funds (MMFs) are open-ended mutual funds that invest in liquid, safe assets like U.S. Treasuries and high-rated short-term corporate debt. These funds should not be confused with “money market accounts” that banks offer to consumers, which are FDIC-insured.

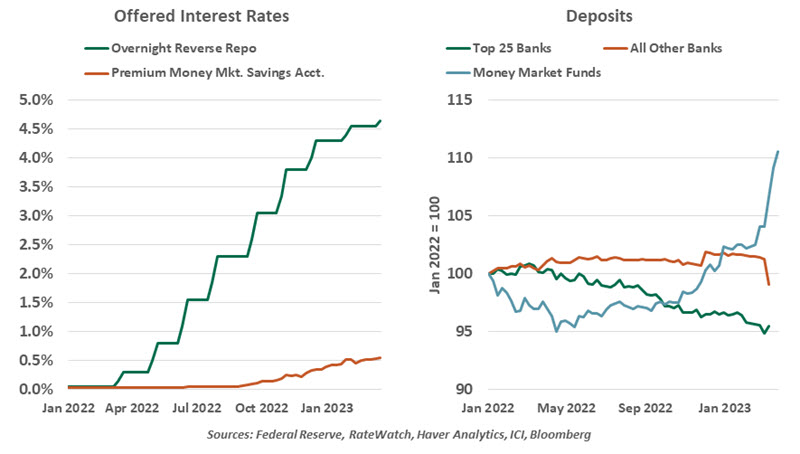

Through 2022, as interest rates rose, money market fund returns grew. MMFs can place their cash overnight in the Federal Reserve’s reverse repo facility, currently paying 4.8% annualized interest with no risk. Amid a difficult year in markets and with interest rates paid on bank deposits low, MMFs became very attractive. The failure of SVB has only built on this momentum. In just the two weeks following the SVB-related volatility, more than $230 billion flowed into MMFs.

Though some are questioning the safety of bank deposits, money market funds are not obviously safer. They carry no insurance or guarantee of positive returns. They were a culprit in the acute phase of the financial crisis in September 2008: a leading fund “broke the buck”—that is, took

losses that brought its price below $1—due to its exposure to Lehman Brothers’ debt. Investors’ confidence was shattered as stress emerged in what was thought to be a safe asset class. Following the financial crisis, management practices evolved and regulations were updated.

The shift from deposits to MMFs could impair the flow of credit to private sector borrowers. MMFs are far more restricted than banks in the investments they can make, with commercial or consumer loans well outside their boundaries. Those segments may not get the same level of capital at the same price that they would have had deposits stayed at home.

The shift of deposits to money market funds did not start with SVB.

Tempering the interest paid on reverse repo placements could be a part of the Fed’s policy normalization, but this is unlikely to help stem the flows of funds outside of the banking system. The gap between money market funds and deposits would still be very large, and concern over the safety of uninsured deposits remains an issue.

The shift from deposits to MMFs is not structural and need not endure. Money market funds are designed to be short-term, liquid instruments; the new money inflows can easily flow back out. But until the financial sector settles, fund flows will continue to set new high water marks.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust