The case for a central bank digital currency has many shortcomings.

Readers of our columns will be familiar with my dislike of cryptocurrencies. (Rants can be found here and here.) Just to reiterate: cryptocurrencies have wildly unstable values, are used extensively for illicit activity, and are easily stolen from virtual wallets. Oh, and the networks they run on take immense amounts of electricity, which enlarges their carbon footprints. Other than that, they are fine.

Another reason I have been down on cryptocurrencies is the possibility that leading central banks would go virtual. A digital pound, euro, yen, or dollar would have a range of natural advantages, including a level of credibility and control that cannot be achieved by private sector alternatives. The International Monetary Fund has come out in favor of the concept, and many nations are moving steadily down this track. But while central bank digital currencies (CBDCs) have a number of benefits, I don’t think that we will see a digital dollar anytime soon.

At the outset, some of you are probably wondering whether a digital dollar is already here. Electronic transactions dominate commerce, to the point where an increasing number of businesses have gone cashless. But your payments at points of sale still have to pass through an interchange process that adds an average of 2% to the cost of transactions in the U.S. The interbank settlement process operates overnight, relying on decades-old protocols designed for checks.

A successful digital currency that operates on a single electronic ledger would reduce those costs and could make settlement instantaneous. Central banks are in an ideal position to provide that digital currency, given their existing role in national payments systems and their responsibility for maintaining financial stability. As monitors and managers of macroeconomic trends, access to the data produced by a CBDC would aid in setting monetary policy.

The electronic ledger that supports a digital dollar would be hosted by the Federal Reserve. Under one CBDC model, individuals could have their own accounts with the Fed, bypassing private institutions. This could expand access to banking services (the FDIC estimates that nearly 6 million Americans do not have a checking or savings account) and reduce the concentrations of deposits held by the biggest banks.

A CBDC would allow individuals to have accounts at the central bank, which would be good…and bad.

Another advantage of this design is that accounts at the Fed would not need to be covered by deposit insurance. The FDIC is bracing for another round of review in the wake of its handling of Silicon Valley Bank, with issues of moral hazard and taxpayer expense front and center.

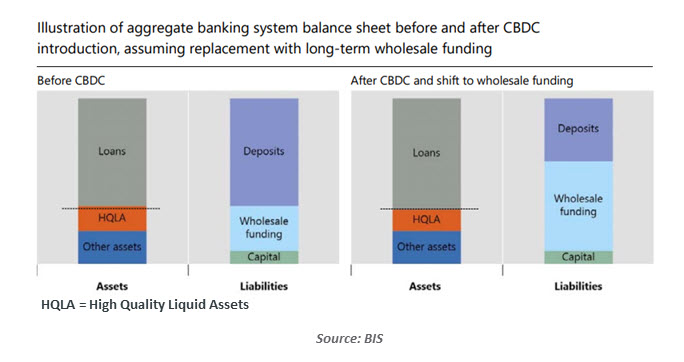

But this CBDC structure could also lead to disintermediation of the banking system. Commercial banks would no longer have the deposits needed to make loans; central banks certainly do not want to get into the underwriting business. Alternative models for CBDCs preserve the role of private sector institutions, but it isn’t clear whether they would compete with or collaborate with central banks.

Any kind of hybrid model where both private-sector banks and central banks offer deposits might not perform well during stress. The bank run prompted by the failure of Silicon Valley Bank could have been much more serious if firms and individuals had been able to park money directly with the central bank.

Apart from design challenges, CBDCs face other headwinds. Privacy guardians are concerned about governmental entities having access to detailed transaction records on citizens. A central bank digital currency would also make it easier to enforce the tax code, which is not universally popular. On this basis, some U.S. states have advanced legislation to preemptively halt adoption of a digital dollar.

The fact that central banks are not formally part of governments does not provide any degree of comfort to critics. Nor does the fact that a great deal of transaction data is already available to the Fed, thanks to its existing role in the payment system.

Last year, the Federal Reserve published background on a digital dollar. Momentum was being provided by Fed Vice Chair Lael Brainard, who has since departed. The material is worded in a very cautious manner; the Fed has stated that it will not move forward with plans in this area without legislative approval, although it is not clear whether Congressional action is required.

Given current apprehensions and political polarization, the path to a digital dollar seems long and bumpy. The Federal Reserve’s plate is full with other matters requiring immediate attention, so I wouldn’t expect them to push too hard for a CBDC.

The issues and politics surrounding a digital dollar make adoption unlikely.

Allowing for careful contemplation is certainly warranted. But as other countries move with greater speed in this area, the dollar is at risk of losing ground in the global payment system. The U.S. dollar’s share of international reserves stands at about 60% today, 10% lower than it was in the year 2000. Further slippage could add to U.S. inflation and borrowing costs.

Failure to create a digital dollar will also allow private cryptocurrencies to attract attention, which means that I could get more questions about them. I am almost hoping that inflation stays high, so that I can run out the clock during presentations by talking about the price level.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust