Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

Getting lost in the moment is easy to do. When planning and executing your fixed income portfolio, looking long term is more likely to get you to your goal. Fixed income portfolio allocations are often meant to first protect principal and second, to optimize income and cash flow per your specific circumstances.

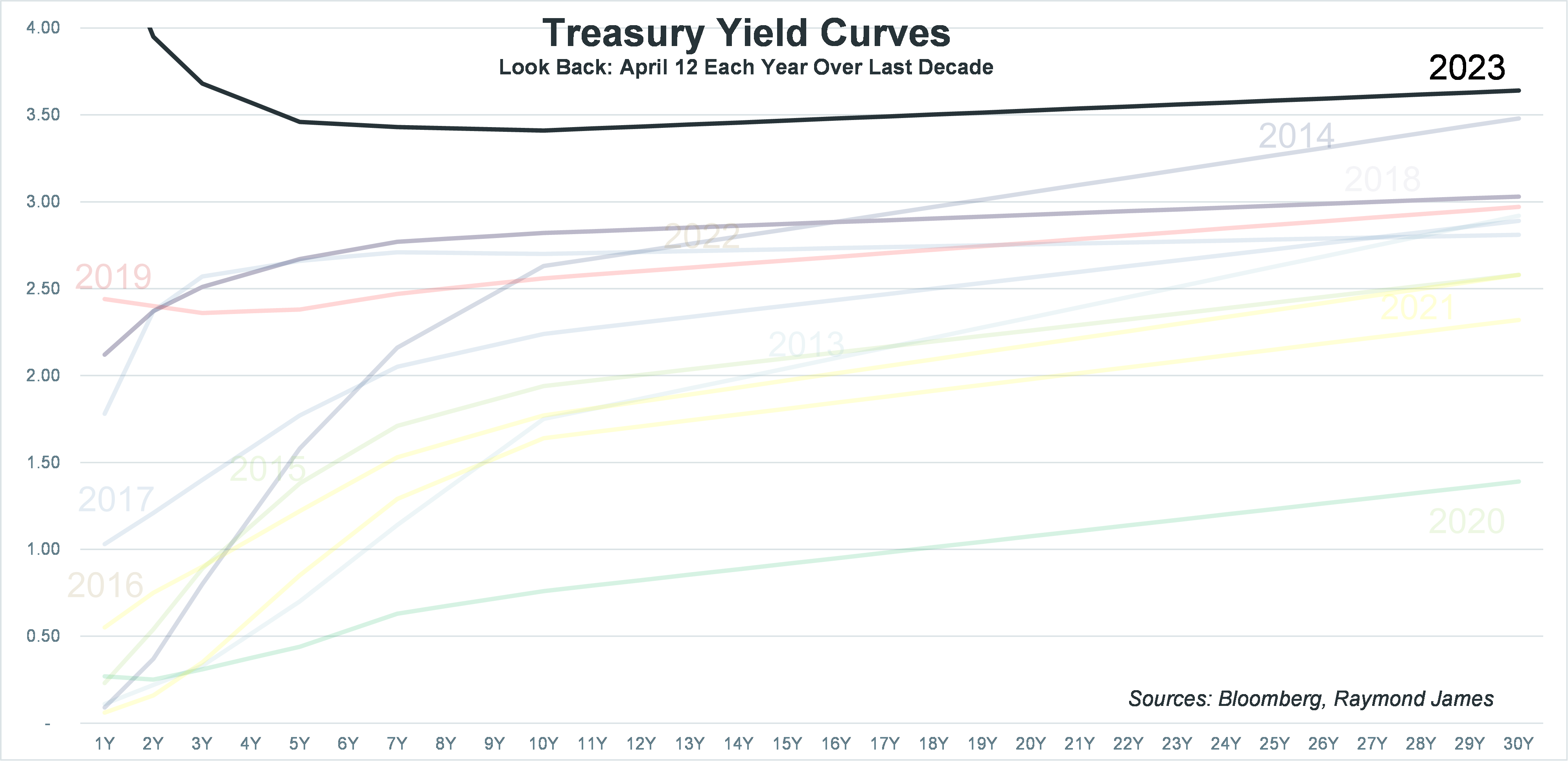

The Treasury curve is inverted creating the urge to buy short and receive higher yields versus extending out on the curve and taking on greater interest rate risk. However, this may not optimize your long term income. The graph below depicts the Treasury yield curve annually on the business day closest to April 12 for each of the last ten years. They are all faded out except the current curve. Over the last decade, rates have traded in a wide range and although we are not at the recent highs, clearly we are at rates higher than we’ve seen over most of the past decade.

Longer maturity bonds lock in yield and cash flow for a longer period of time while still providing a known date for a bond’s face value to be returned, regardless of interest rate fluctuations. As long as you hold an individual bond to maturity and barring a default, the only change you will see is the price on your statement and whether that turns red or black, your realized cash flow and income are not changing. If a recession occurs, it is logical to conclude that interest rates will fall. The window of opportunity may be limited depending on continued Fed actions and economic output. The one certainty is that rates are as favorable as they have been for most of the last decade. Lock in for longer… add duration.