The banking problems that dominated the news last month have largely faded into the background. Analysts are watching first-quarter earnings reports from the industry, looking for further signs of weakness, but the risk to the financial system seems to have eased.

That should mean that central banks can return their focus to the fight against inflation, which remains stubbornly high. Yet the Ides of March may still have an influence over monetary policy.

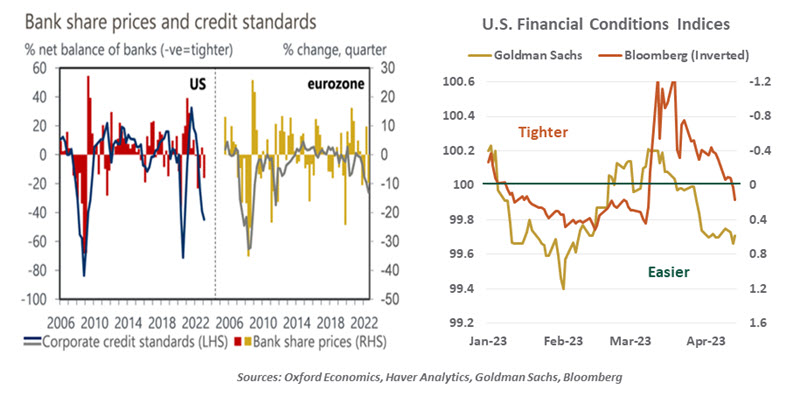

Banks are still under some measure of stress: indices of bank stock and bond prices are still depressed. Deposit movements have hindered liquidity at some firms. This combination of circumstances typically causes conservatism in lending.

The most comprehensive reports on bank credit conditions come from central banks. The Federal Reserve’s Senior Loan Officer Opinion Survey and the European Central Bank’s (ECB’s) Bank Lending Survey pose a series of questions that cover terms, pricing and demand across a range of loan types. The most recent editions of both reports came out in February, before Silicon Valley Bank (SVB) and Credit Suisse hit the headlines. Both indicated that conditions had already become quite restrictive, amid rising interest rates and recession probabilities. The next releases of the reports are in early May, coinciding with the next meetings of the Fed and the ECB.

Additional conservatism on the part of banks will slow economic activity. The degree to which this occurs depends on how reliant borrowers are on banks: European borrowers get about 60% their credit from this source. Encouragingly, the forced merger of Credit Suisse is generally being viewed as an isolated incident. The European Banking Authority recently released its latest risk dashboard, which showed strong capital and liquidity buffers.

Markets provide the lion’s share of financing in the United States; on that front, recent news has been considerably more encouraging. Indexes of U.S. financial conditions have improved quite a bit in recent weeks, with credit spreads narrower and market volatility lower than their March extremes. Overall, access to capital is on the easier side of neutral.

The bifurcation between bank and market pricing for credit makes it difficult to determine the consequences for economic growth in the United States. Focus has been trained on small businesses in America, which rarely access capital markets and get almost 70% of their credit from smaller banks. According to the U.S. Bureau of Economic Analysis, smaller firms account for an estimated 25% of annual gross domestic product (GDP) and 35% of payroll employment. In addition, regional institutions provide the majority of the credit extended to commercial real estate. With challenges ahead for office properties, any reduction in bank lending will make a difficult situation worse.

Federal Reserve data suggests that money has been in motion ever since the SVB failure. Since the beginning of March, money market fund balances are 9.5% higher; deposits at the 25 largest banks are 0.4% greater; and deposits at the remaining U.S. banks have dropped by 3.2%. To compensate for funding loss, smaller institutions have been among the more active users of the Fed’s Bank Term Funding Program. This suggests that small and medium-sized enterprises will be the ones feeling a potential squeeze in the months ahead.

Banking stress will hinder lending…but by how much?

Demand for commercial loans has been very modest, though. And the most recent survey conducted by the National Federation of Independent Business (which was released last week) showed that 59% of firms were not looking for a loan and only 2% reported that their borrowing needs were not being satisfied.

Those brave enough to attempt to model the impact on growth find that the incremental pressure on credit standards could shave up to 0.5% from this year’s real GDP growth in the U.S. We suspect the incremental impact will be small, but the late winter banking stress will remain a topic of central bank conversation throughout the spring.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust