Fed Preview: The End is Near

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Federal Open Market Committee (FOMC) will gather next week to take stock of monetary policy. The meeting will likely mark a turning point, and so we are devoting this issue to an in-depth preview of the discussions.

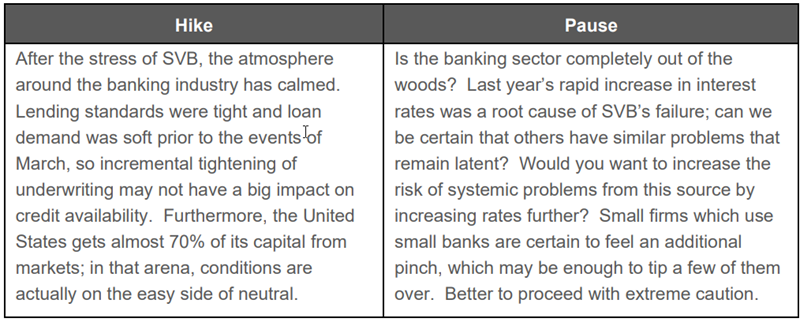

Public statements from some Fed officials suggest that stress in the banking sector justifies pausing the tightening program. Other participants have sustained a laser-like focus on inflation, which remains above desired levels. Arriving at a sound diagnosis and issuing the correct prescription will be especially challenging.

Following are the factors the group will consider, with arguments on both sides of each topic.

Economic Growth

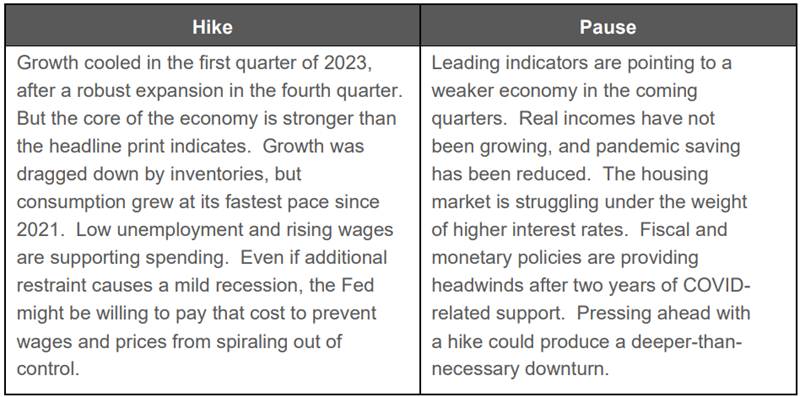

Following a strong rebound in 2021, the U.S. economy slowed last year in the face of elevated inflation, higher interest rates, weaker investment and disruptions caused by the Ukraine war. Growth is set to slow to a crawl, but enough to avoid the label of recession. Tighter monetary policy has impaired growth, but the expansion still has room to run.

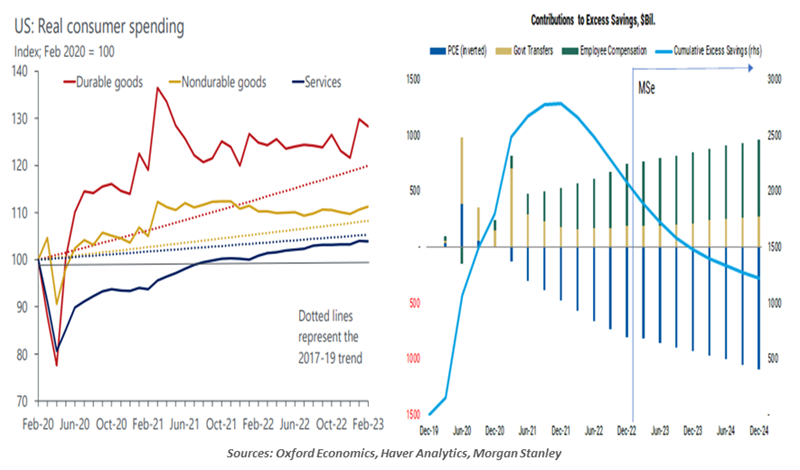

The U.S. economy has been surprisingly resilient. After real gross domestic product (GDP) declined during the first half of 2022, output has expanded at a 2.3% annualized rate since then. Absent new shocks, recession is still not our base case.

Inflation

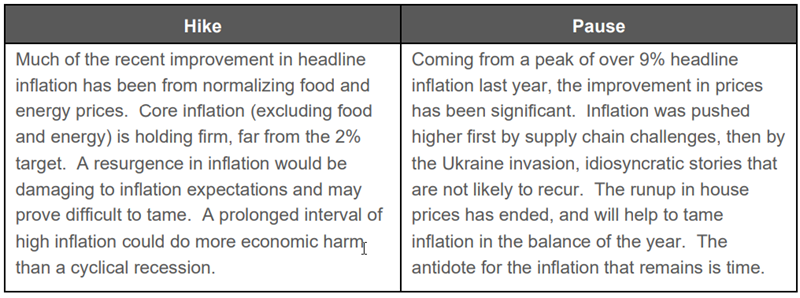

As inflation shifted from a transitory phenomenon related to the COVID reopening to a systemic challenge, the Fed changed its posture assertively. The Fed Funds target rate rose by nearly five percentage points in the span of a year, and quantitative tightening was initiated. Nonetheless, inflation persisted.

Rates of price changes are on the way down, with movements over the most recent quarter quite a bit lower than the year-over-year changes. The decline in the money supply will be structurally disinflationary; cooling demand and recovering supply will also take the edge off the price level. But how far down will inflation go, and how long will it take to get there?

Inflation is heading down, but its ultimate destination remains unclear.

Uncertainty around the answers to those questions will make it difficult to conclude the tightening cycle. The mistakes of the 1970s, when policy was eased prematurely, are ones that the Fed does not want to repeat.

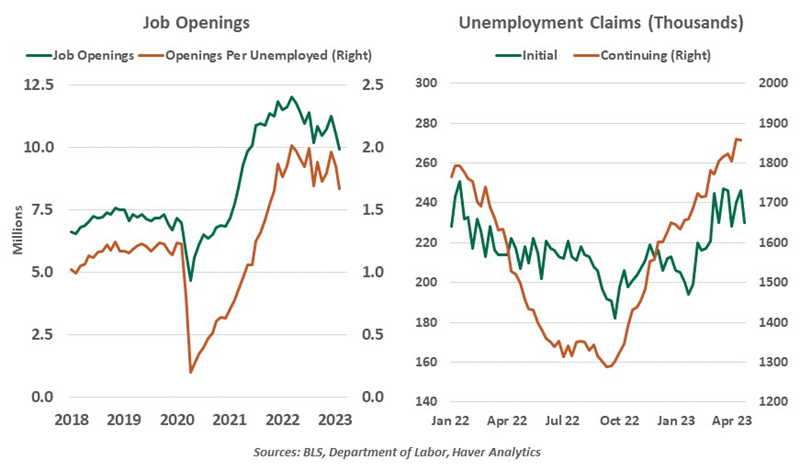

Employment

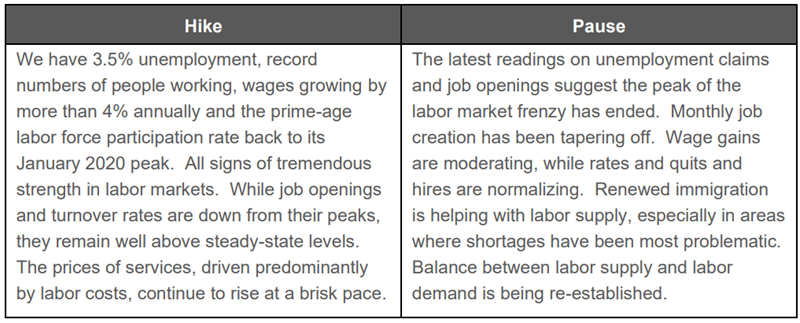

The job market has very likely turned a corner. The story extends beyond the conventional data we usually study; the first quarter was marked with a spate of layoff announcements from a slate of high-profile employers. The absolute numbers of layoffs have been small, but the enthusiasm in the job market has subsided.

The labor market is cooler, but still hot.

But if labor markets are the canary in the coal mine of a pending recession, this bird is still alive and well. Some further moderation will likely be needed for the Fed to head to the sidelines.

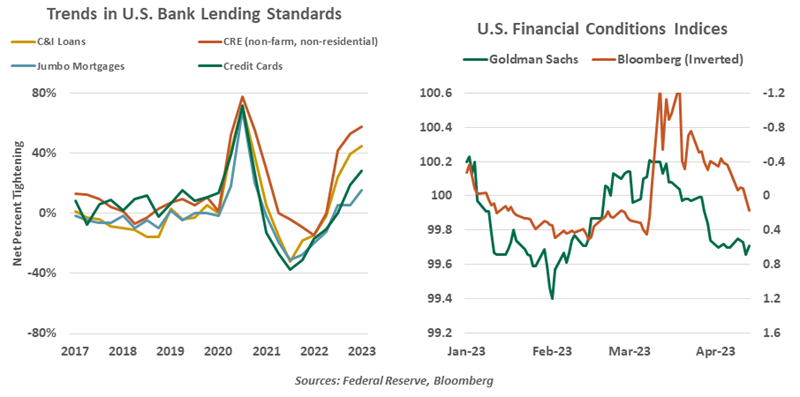

Financial Conditions

This week’s headlines surrounding First Republic Bank are not pleasant, but the bank has been teetering for almost two months. Its travails have not yet spread to others; first quarter earnings reports for banks have provided no smoking guns. This isn’t to say that the industry isn’t still under a microscope, but the threats it presented six weeks have receded.

Late last year, the Fed was concerned at the easing of financial conditions, and suggested that they might have to be more restrictive in compensation. That point is sure to be raised next week; for some FOMC participants, the idea that markets are easing will make it easier for them tighten.

Taking all of this onboard, we expect the Federal Reserve to raise overnight rates by a quarter-point next week. To acknowledge the deceleration of inflation and lingering anxiety about the financial system, the message accompanying the move will likely be somewhat dovish.

Bank lending conditions are tight, but financial conditions in markets are easy.

But the language will probably also discourage markets from assuming cuts later on this year. This may not go down well, as bond prices presently imply 75 basis points of retreat between now and December. We saw something similar in February; two year yields increased by almost 100 basis points in the month following tough messaging from the Fed.

The FOMC will not release any new projections at this upcoming meeting, so incremental information will largely come from the press conference. In addition to the traditional topics, Chairman Jay Powell will almost certainly be asked about the debt ceiling debacle and its impact on monetary policy. We’ll be leaning forward in our seats for the answer to that question.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All