The Federal Reserve is responsible for monetary policy, with a mandate to keep inflation close to 2%. It also regulates banks, with a mandate to sustain financial stability. One of its key programs may be placing those two goals at odds with one another.

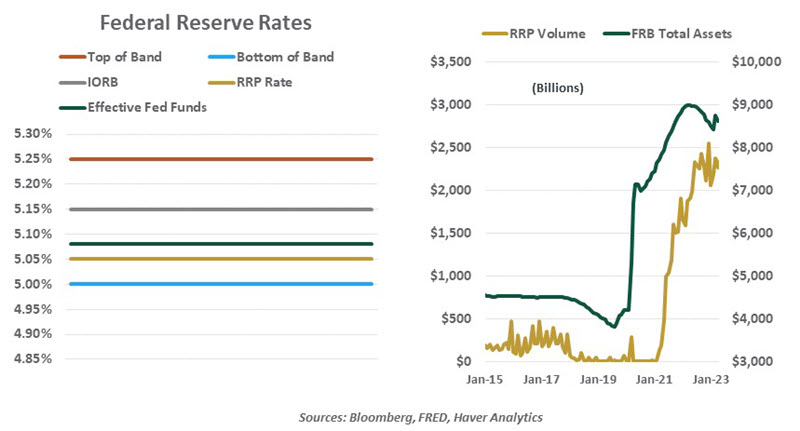

Ever since 2008, the Fed has expressed its target for interest rates as a 25 basis point band. At the conclusion of this week’s Federal Open Market Committee (FOMC) meeting, that range was 5.00% to 5.25%. Actual interest rates are set by the markets, based on the supply and demand for money. The Fed’s task is to keep yields within its goal posts.

To keep a lid on the overnight rate, the Fed offers interest on deposits placed with it by banks. The theory is that banks will purchase funding from markets if they can earn a spread by reinvesting it. The interest rate on reserve balances (IORB) therefore contains the rates that banks are willing to pay for overnight borrowing. The IORB has typically been set near the top of the Fed’s targeted range.

To prevent overnight rates from falling below the bottom of the target band, the Fed established a reverse repurchase program (RRP) in 2015. Under this facility, the Fed takes in excess funding from select market participants for short periods, paying them an interest rate that is linked to the bottom of the target range. Those eligible would not be willing to sell their excess liquidity for less than the rate offered by the Fed, so the RRP places something of a floor on the cost of overnight money.

The Fed’s RRP program started slowly, but volumes have mushroomed since the pandemic. The liquidity injected into the financial system by the Fed since 2020 has been far more than could be lent, and so trillions of dollars have settled in the short-term investment markets. In essence, a significant amount of monetary stimulus ended up doing a round trip and ending up back on the Fed’s balance sheet, now yielding a safe return of over 5%.

Money market funds find themselves in the middle of this circuit, accounting for almost all of the volume in the Fed’s RRP facility. Reverse repos with the Fed account for about 40% of the holdings of U.S. money funds.

These holdings make money funds much safer than they were during the financial crisis of 2008 when these products were invested in a broader range of asset classes. As an example, the Reserve Fund had concentrated holdings in Lehman Brothers commercial paper; when Lehman failed, the fund was forced to “break the buck,” thereby casting doubt over the whole sector.

A key Federal Reserve program is providing stiff competition for bank deposits.

By contrast, money funds are seen by investors today as a safe haven. As we discussed here, they have gained balances since the beginning of March, while bank deposits (especially at smaller institutions) have declined. In this sense, reverse repurchases have been seen as contributing to disintermediation at a time when the Fed is seeking to reestablish financial stability.

This is certainly not the Fed’s intention. And there is very little that the Fed can do to alter the result. Lowering the RRP rate slightly will not be enough to make bank deposits competitive. Lowering the RRP rate by a lot might cause overnight rates to fall, producing an unwanted easing of monetary policy. Over time, the RRP should shrink in concert with the Fed’s balance sheet, but this will happen only gradually.

The best thing for the Fed to do under current circumstances is to keep up its active surveillance of developments in the banking system and sustain its communication about its general soundness. Efforts to reinforce the oversight of risks facing financial firms will also provide a measure of reassurance.

Ultimately, the cure for what ails the system may be time. A few months without bad banking headlines would be a very welcome development.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust