Doug Drabik discusses fixed-income market conditions and offers insight for bond investors.

As long as the opportunity exists, we are compelled to present it. Yields in spread products are comparatively favorable looking back more than a decade in time. CDs, corporate bonds, and municipal bonds all have favorable curve positions appealing to a wide array of investor needs. Although the primary function of fixed income is often protection of principal and an offset to growth asset risk, market conditions have provided relatively high yields and coveted cash flows for investors ready to take advantage of this. How long this window stays open is in question and perhaps suggests a hastening of action.

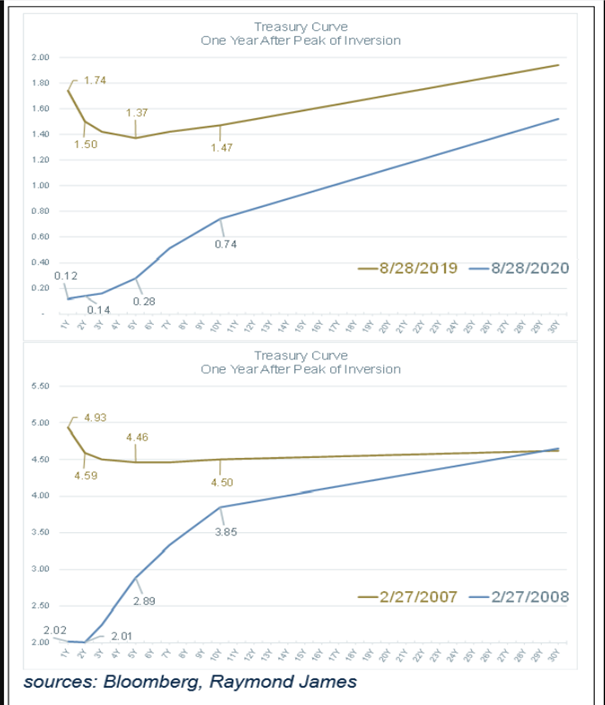

The FOMC committee met last week and raised the Fed Funds rate by another 25 basis points (bp), bringing the total rate hike to 500bp over just 17 months. This is an extreme change in a short period of time. For the first time in this cycle, the Fed included language to suggest that the hike cycle may or may not continue. This is important because until now, they were unwavering about their stance to continue raising rates until inflation was under control. Although inflation numbers have fallen substantially, they are pointedly far from target levels. The Fed’s actions have created an inverted Treasury curve as short-term rates have pushed higher while intermediate and long-term rates have not kept pace.

The graphs show previous yield curve inversions (gold lines) at their widest inversion and compare how the yield curve looked one year later (blue lines). These graphs represent the inversions prior to the Great Recession and to the COVID recession. Previous inverted curves offer similar outcomes. Inverted Treasury curves are an indicator of lower future rates.

The window to lock in higher yields for longer (extend duration) is now. How long the window stays open is uncertain.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein were obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include an analysis of sectors, securities, and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions that may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk, and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.

© Raymond James

Read more commentaries by Raymond James