Debt Ceiling: High Risk, Low Reward

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat follows a technical default? We hope we will not need to find out.

History is littered with examples of unintended consequences: outcomes of an action that are unrelated to the intent of the decision. Smokestacks helped to keep ground-level air clean but polluted the sky and caused smog. Municipalities that mandated bicycle helmets in the interest of safety found they only deterred people from riding bicycles.

The list goes on, and the U.S. debt ceiling ranks high on it. In the nation’s first 130 years of independence, the Treasury could issue debt only by an act of Congress. During World War I, the high spending required for the war made this arrangement unworkable, as the Treasury inundated Congress with funding bills. In 1917, Congress remedied this with the Second Liberty Bond Act, authorizing the Treasury to issue debt freely up to a statutory limit, then return to Congress when a higher authorization was needed.

Since its creation, the ceiling has been raised or suspended over a hundred times, usually with no controversy. But under a divided government, the limit has been used for objectives far from its intended purpose. Far from its intention to be a remedy, the limit has unintended consequences that carry tremendous risks to institutional and market stability.

The United States federal government runs a structural deficit. The nation requires new debt to be continually issued in order for the government to operate. Leaders have been elected on promises to lower deficits and debt, with inconsistent results.

Lower debt is a worthy goal. Interest payments crowd out the opportunities for lowering taxes or spending on more productive government programs. Capacity to issue debt is valuable in downturns and crises, when government spending can offset declines in the private economy. Uncontrolled spending can undermine confidence in the dollar, an ingredient in the U.S.’ privileged global position. In the extreme, out-of-control debt growth has been a feature of the downfall of failed nations throughout history.

But the time to advocate for lower debt is in the annual budget cycle when spending is committed. Opportunistically using a mechanical funding mechanism to force a reduction in spending is effectively taking the economy hostage.

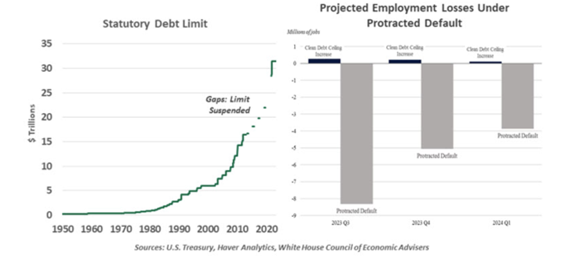

The risks are wide, with the consequences varied and unpredictable. At first blush, this sort of disruption would seem like a risk-off event that would cause an equity sell-off and a flight to quality. That was the outcome of the 2011 showdown when S&P downgraded its rating of U.S. debt: The S&P 500 index fell nearly 17% as the situation unfolded, and Treasuries rallied. Upon reflection, it does not stand to reason that U.S. debt instruments would be a safe haven when U.S. debt is the root of the issue at hand. Debt held by the public was a mere $10 trillion in the 2011 episode; today, it stands at over $24.6 trillion—hardly a lower risk profile.

In subsequent negotiations (2013, 2015, 2021), market reactions have been much more muted. Tense negotiations are no longer a surprise. However, a technical default would be a novel market shock that could bring tremendous volatility.

Cutting spending is easier said than done.

If a stalemate leads to a government shutdown, ramifications will appear quickly. The shutdown of October 2013 had wide-ranging consequences. Government workers were furloughed but then received back pay, a waste of taxpayer-funded payrolls. From the closure of national parks to delayed food safety inspection, the loss of government workers slowed the economy; S&P tallied the damage at 0.6% loss of gross domestic product. Estimating the risk of a prolonged stalemate today requires a great deal of assumptions; the White House’s worst-case scenario projects a recession with severity comparable to the global financial crisis. Industry leaders are describing it as a “seismic event” that could cause a “panic like 2008.”

The need for action has long been foreseeable. In the year to date, early negotiations took the form of loud public pronouncements of the spending that will not be cut. No politician will propose reductions to Social Security or Medicare entitlements for the elderly. No one is contemplating military cuts amid high geopolitical tensions. Defaulting on the debt is not an option. The remainder of non-defense discretionary spending is quite small. A compromise to cut that limited share of spending will necessarily be modest.

Against this sordid history, U.S. leadership began challenging bipartisan talks this week. The initial meeting between President Biden and congressional leaders yielded no results, as expected. The only good news was that neither side walked out in frustration, and meetings will continue. Any resolution is likely to come in the 11th hour. Based on recent estimates, that hour may arrive soon.

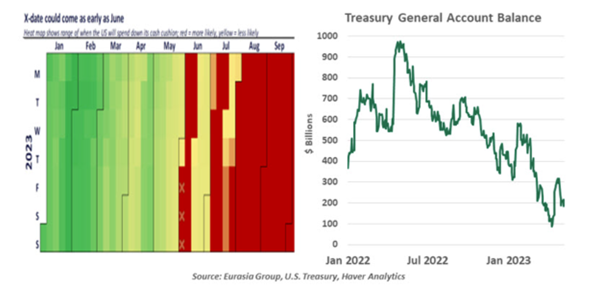

Last week, Treasury Secretary Janet Yellen testified that the “x-date” – the date at which the Treasury runs out of funds to pay obligations – may come as soon as June 1. A precise x-date cannot be forecast, as it depends on unpredictable daily cash flows in and out of the Treasury General Account (TGA), the government’s operating account. Several analysts have since updated their own estimates and arrived at dates close to Yellen’s prediction. If the nation can stay solvent through June 15, the influx of quarterly corporate tax payments will defer the x-date to late July, but that date may prove to be out of reach.

Measures to keep the government working through a default are untested.

If the limit is breached, temporary remedies might be possible. Treasury may be forced to explore payment prioritization, servicing the debt while deferring other obligations. Similarly, the Fed could intervene by accepting defaulted securities for repo transactions or buying defaulted bonds on the open market, keeping Treasury markets functioning. But these are speculations, not plans. Neither Secretary Yellen nor Chair Powell wishes to offer any notion that a resolution can be deferred.

Permanent legislative solutions to the debt limit are preferable to repeating these cycles of tensions. An outright repeal is an option, though it seems unlikely. Instead, Congress could reinstate the “Gephardt Rule:” from 1979 until its repeal in 1995, the debt limit was automatically raised when the budget was ratified. More extreme executive actions, like minting a high-value platinum coin or abrogating the debt limit under the guise of the 14th Amendment, would invite prolonged litigation and only cast further uncertainty over the economy.

All past episodes of debt limit brinksmanship have been resolved without lasting consequences. We hold out hope that cooler heads can again prevail. The risks of a technical default are too severe to cast aside, and we all must prepare for a highly uncertain, high-volatility interval. We will not welcome the stress, but a market disruption will make a clear case for reform of the debt limit. Sometimes, unintended consequences can be beneficial.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All