The Northern Trust Economics team shares its outlook for U.S. growth, employment, interest rates, and inflation.

The outlook for the American economy has been clouded by concerns over the health of the banking sector. Shaken by a handful of failures, investor confidence in regional banks remains low. In turn, those institutions have cut back on credit extension, which adds a headwind to growth.

The debt ceiling deadlock is adding to the uncertainty. Even a short-lived stalemate that brings a technical debt default and reduced government expenditures will have wide-ranging ramifications for the economy.

Tight monetary policy and lending conditions will constrain consumer spending, hiring, and investment, leading to weak growth in the remainder of the year. Recession is a possibility, but not our base case.

Enduring apprehensions over financial stability, improvement in inflation readings, and early signs of loosening labor market conditions have likely brought the Fed’s current tightening cycle to an end. However, the disinflationary trend is progressing far too slowly for the Fed to pivot before the end of the year.

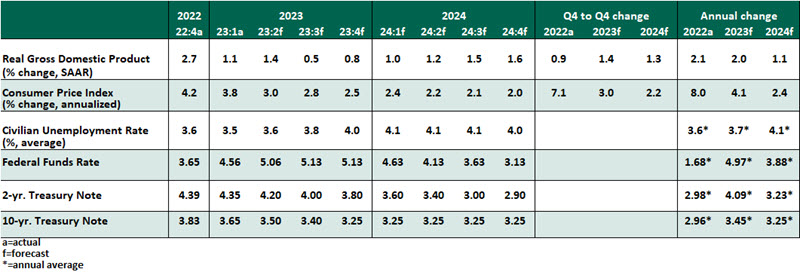

Key Economic Indicators

Influences on the Forecast

· After a few weeks of calm, more regional banks have come under pressure, raising fears of financial system instability. Regulators’ selective approach to backstopping depositors has not stemmed the tide of money movement. The ongoing uncertainty is likely to weigh on credit conditions; the Federal Reserve’s Senior Loan Officer Opinion Survey shows the tightest standards in a very long time.

· The debt ceiling is another source of anxiety for financial markets; the “X Date,” that time when the federal government will be unable to pay all its bills in full, could arrive as soon as early June. The risks are wide, with the consequences varied and unpredictable. A stalemate leading to a technical default could trigger a recession. The potential for political miscalculations remains, but we are hopeful for a resolution, as the parties are still engaged in finding a middle ground.

· Real gross domestic product growth cooled to 1.1% annualized in the first quarter of 2023, after a solid 2.6% expansion at the end of 2022. But the weaker growth was a result of a large drag from the volatile inventory component, as consumption grew at the strongest pace since the second quarter of 2021. Going forward, consumers and businesses will pull back spending amid tighter lending conditions, elevated interest rates, and persistent inflation.

·We continue to expect slow growth, but not quite a recession. Such a slow outlook could get knocked into contraction by any downside risk, raising the stakes of a prolonged debt ceiling impasse or further stress among regional banks.

· U.S. headline inflation measured 4.9% year over year in April, the first reading below 5% in two years. However, the core metric continues to be stubborn, slipping only a tenth to 5.5% year over year. A closer look at the report shows that the breadth of inflation has started to soften. Rents are now rising at a slower pace than earlier in the year. Services inflation excluding energy and shelter eased last month.

· Amid the continued improvement in inflation dynamics, the Fed is likely to hit the pause button at the June meeting. However, cuts in 2023 are unlikely given that inflation is expected to stay well above the 2% target for the rest of this year.

· The April jobs report surprised to the upside, with the unemployment rate dipping further to 3.4%, wage growth accelerating one-tenth to 4.4% year over year and nonfarm payrolls rising by 253,000 – much stronger than expected.

That said, there are signs that labor market rebalancing is underway. Job growth for March and February was revised downward, and the four-week moving average of initial jobless claims is holding at its highest level since November 2021. Overall, labor market conditions continue to offer support to our call for a soft-ish landing for the economy this year. Higher unemployment is not desired by anybody but is a necessary step toward a cooler economy and inflation.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust