Both domestic and external forces may limit China's growth prospects.

It had been four years since I visited Beijing. The spring weather and the spring flowers made the city sparkle. The air was clear, in more ways than one.

The time spent last week in China and Hong Kong was impactful. My partners and clients are enjoying a renaissance after two and half years of COVID caution, which was followed by two and a half months of extreme contagion. Both were harrowing and will not soon be forgotten. But the relative freedom now afforded to those living in the two places has lifted spirits and economic activity.

I didn’t want to spoil the mood, but the experience of other countries suggests that the initial months of post-pandemic exuberance will give way to a slower and more sustainable pace of spending and production. COVID-19 will almost certainly have the same kind of lasting impact on China’s society and its economy that other countries are experiencing. And the competitive and geopolitical landscape is much more complicated than it was in 2019, creating stronger headwinds to China’s progress.

China was first into the pandemic and the last one out. The outbreak prompted an aggressive response: lockdowns, contact tracing, and forced quarantine for the sick were applied everywhere the virus appeared. China was slower than other countries to initiate vaccination, and when they did, their vaccines proved to be less effective.

The breadth and severity of public health restrictions impaired the Chinese economy in a range of ways. Factory shutdowns and logistic interruptions caused severe supply chain distress. The consequences were felt the world over Chinese manufacturers struggled to sustain output while their export clients experienced delivery delays and high inflation. These networks have recovered, but the experience may have long-term costs for China as re-shoring gains momentum.

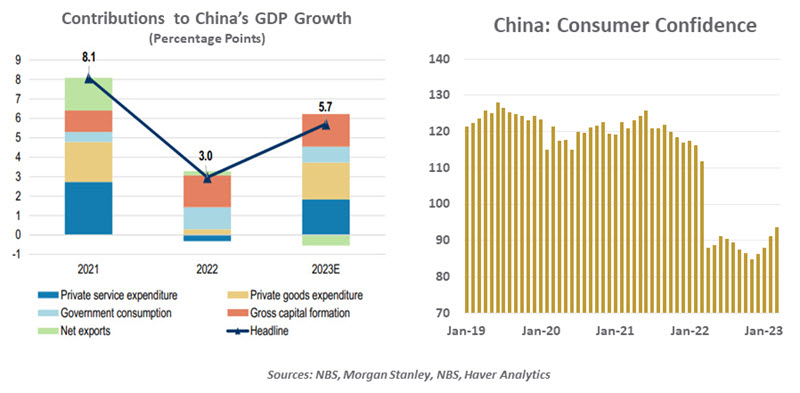

Chinese consumers were also impaired. Lockdowns, and fear of being locked down, limited mobility and hindered commerce. The national mood didn’t help: Chinese consumer confidence plunged early last year and has only recently begun to recover. Overall, real economic growth in China was just 3% in 2022, one of the worst performances of the past 50 years.

With the pandemic now in the past, there is a sense of excitement about China’s prospects for the balance of 2023. Renewed freedom and pent-up demand combined to create powerful growth in Western countries in 2021; we are seeing similar developments in China. Spending on services like travel is growing rapidly; regional destinations are the most popular.

At its “Two Sessions” gathering in Beijing in March, Chinese authorities committed to a target of “around 5%” real growth this year. To augment its chances of reaching this level, selected policy measures have been implemented to boost activity.

China is enjoying a post-pandemic recovery, but its longevity is in question.

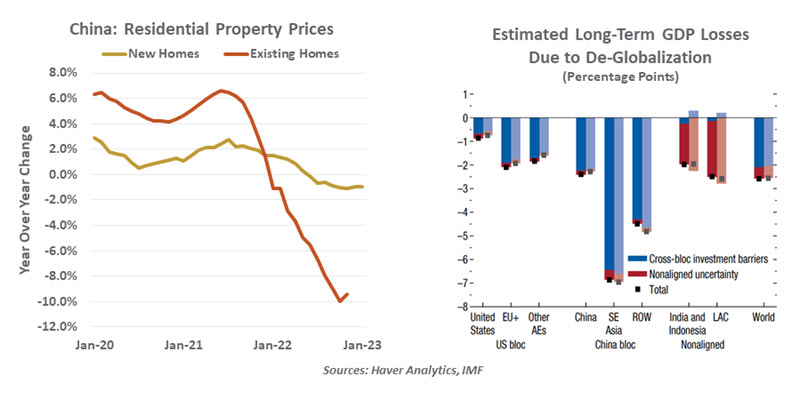

Achieving this objective may be difficult. Developed countries around the world are looking at very modest growth prospects, with recession a distinct possibility. Sluggish economic activity in the United States and Europe will limit demand for Chinese exports. At home, Chinese consumption will almost certainly taper off after the post-pandemic boom. Many parts of the country are still coping with the consequences of a property market crash that has damaged household balance sheets. Some additional savings will be necessary to replenish the money lost.

Looking longer-term, however, China is coping with a series of challenges. Among them are:

- The gathering momentum behind de-globalization. A confluence of factors is contributing to this trend: concerns that free trade isn’t fair trade, a desire for more resilience after pandemic-induced supply chain disruptions, and the vulnerability of sources to international sanctions.

- China has been at the center of all three of these elements and stands (along with its Southeast Asian neighbors) to be the biggest loser if there is further fragmentation in international commerce. And as we have discussed, diminished export prospects could lead to debt distress among some emerging markets.

- It is extremely unlikely that companies and countries will seek a complete divorce from China, given the scale and efficiency of its manufacturing sector. But even a modest loss of export market share would make it very difficult for China to sustain its recent economic pace.

- China’s advantage as an exporter has been diminished by rising labor costs and the perceived risk of operating there. The government’s moves to rein in selected foreign and domestic firms have diminished the confidence of potential foreign investors.

- China’s demographics are very challenging. The nation’s population fell last year for the first time in more than 60 years; birth rates remain very low; and the country does not attract many immigrants. The ratio of retired to working people is rising rapidly and with it the cost of pension and health systems.

- Productivity growth can compensate for a diminished labor force. The latest generation of artificial intelligence (AI) offers hope on this front. However, the advancing technology embargo imposed on China by the United States may limit the development of new capabilities. Concern centers around the potential strategic applications of AI, as apart from its economic utility.

- China is a heavily indebted country, which will limit its ability to use government spending to sustain growth. On the other side of the lending ledger, China has been a significant source of credit to other countries, largely through its Belt and Road Initiative (BRI). Many BRI loans have gone into default, and require restructuring. The process is delicate, and China is likely to realize some losses.

Slow growth in population and productivity may limit China’s growth prospects.

An afternoon visit to the Forbidden City reminded me that China has a long and rich history that is filled with triumphs and tragedies. But China’s growing international profile means that its fortunes, both financial and societal, are closely bound up with ours. There can be no smooth runway for anyone if friction with China cannot be reduced.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust