Risks to Growth Are Ample but May Prove Surmountable

Authors and artists face a challenge with every work: Knowing when their piece is finished. A self-critical creator can always find a thought to tweak or a color to change, but at some point, the pens and paintbrushes must be set down.

Central banks are working through that dilemma now. After a hard, year-long battle against inflation, the end of rate hiking cycles is in sight. While the rapid ascent is over, some nations are struggling to ensure they have passed the climax of their inflationary story. More rate hikes may yet be in store but without the size, frequency, and urgency of decisions made in 2022.

Challenges extend beyond inflation. Nations must reckon with slower domestic demand, higher borrowing costs, constrained labor supply, trade decoupling, an ongoing war, and banking sector uncertainty. We are living in a story with a long and complicated plot.

Here are our up-to-date perspectives on how major economies are poised to perform during this year and next.

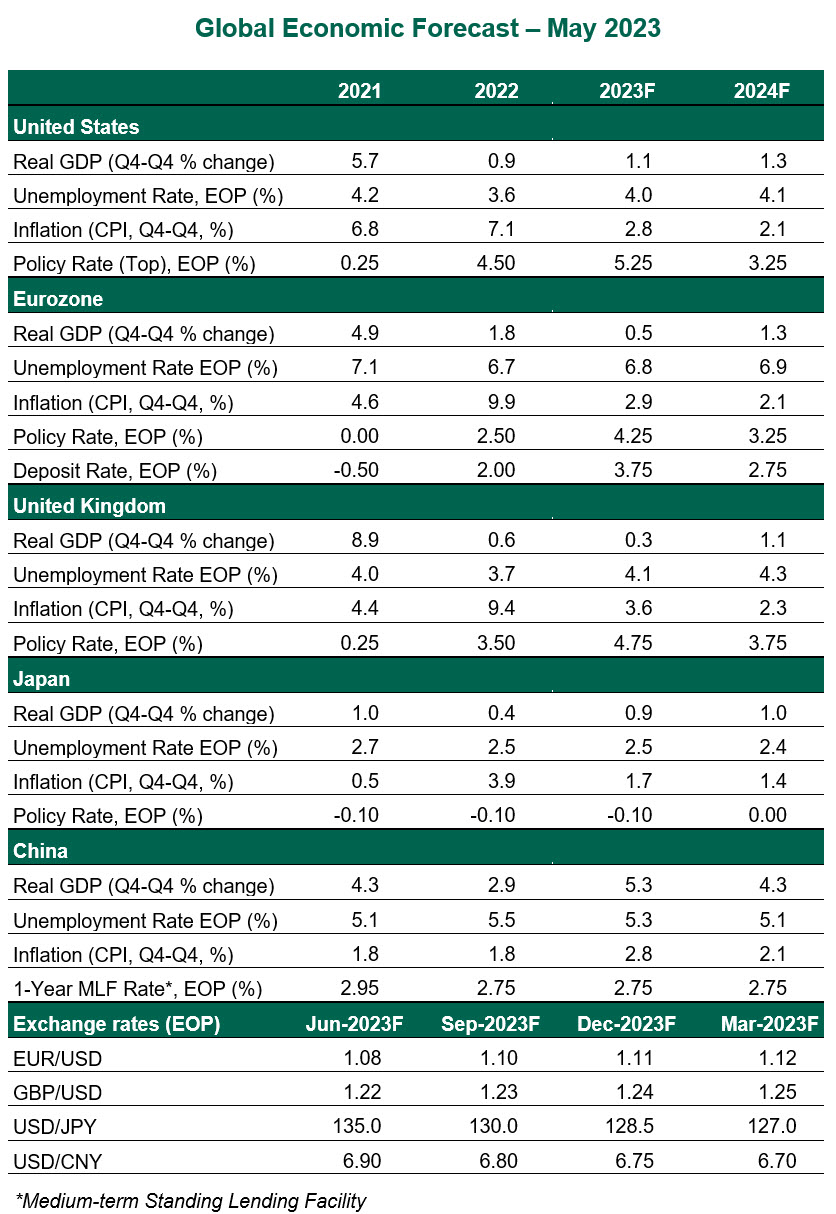

United States

- U.S. inflation is just barely improving. Core consumer price inflation measured 5.5% year over year in April, still too high. Taming house prices and a long-awaited cooling of services inflation offered hope for further improvement. Labor markets remain strong, with the unemployment rate at 3.4%. Job openings are declining, and initial unemployment claims have increased slightly. With prices calming and labor markets rebalancing, we expect the Federal Open Market Committee’s increase in May was the last policy hike, but cuts are not yet in sight.

- The debt ceiling debate has introduced legitimate fears of a financial crisis, contributing to a pervasive sense of worry. Financial sector instability and the end of pandemic support are putting U.S. consumers through a difficult transition back to normalcy. Consumer spending has been the defining element of the sustained U.S. recovery; if employment holds up, so can spending.