When selecting topics for our commentary, we endeavor to avoid repeating subjects in short order. The global economy offers no shortage of fodder for research and analysis. But we will waive the rule for urgent circumstances, and the U.S. debt ceiling certainly qualifies. Since our review two weeks ago, the immediate circumstances are little changed, but the stakes and consequences are becoming clearer.

As we go to press, negotiations toward some sort of deal continue. Comments from participants have ranged from constructive to frustrated. Last Friday, Republicans walked away from the table in the morning, but returned in the afternoon. President Biden and House Speaker McCarthy have both given assurance that the U.S. will not default, without an accompanying plan to actually prevent default.

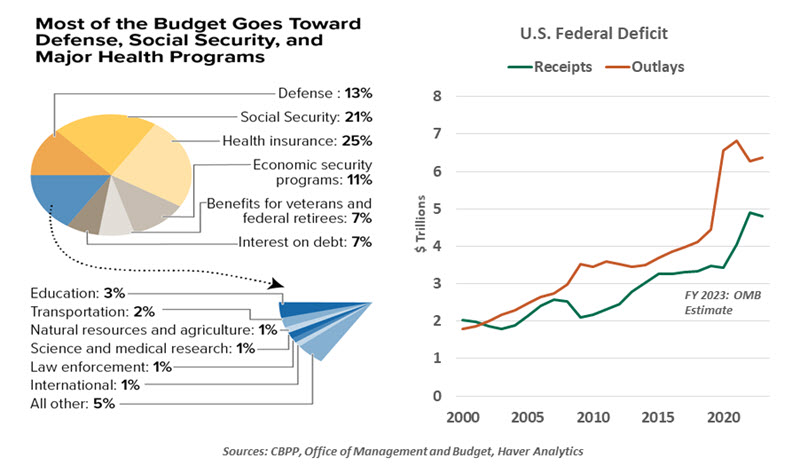

Sticking points in the standoff center on the level of spending in fiscal year 2024, and caps on spending growth thereafter. The “Limit, Save Grow Act” (LSG) bill, the basis for Republicans’ negotiations, called for returning funding of federal agencies to fiscal year 2022 levels, a reduction of $131 billion (8%) to discretionary spending. However, as written, that would entail a cut to military spending, a contentious idea in an era of higher geopolitical risks. Focusing cuts on just non-defense discretionary spending puts only about 12% of the federal budget in scope for reduction. Cuts to programs in agriculture, education, transportation, science and energy may prove unpopular.

Once a baseline of spending is agreed, negotiators will then determine the caps to apply to spending growth. LSG proposes a limit of 1% annual spending growth for the next decade; with inflation likely to exceed 1%, the cap would be a spending reduction on a real basis. Caps can be reconsidered in future budget negotiations if they prove unworkable.

Negotiators are also deliberating the duration of the debt limit extension. LSG’s proposal was only an extension through March 2024, a timeline that would set the stage for another round of budget drama in just ten months. Neither party would benefit from a return to this controversy nor a risk of default in an election year. We anticipate a longer extension.

The urgency for a deal is high and growing. Treasury Secretary Janet Yellen affirmed an expectation that Treasury may be unable to service all obligations as soon as June 1. Most private forecasters concur that a real risk looms in early June, which starts next week. Given the series of approvals that will be needed and the debate that will accompany them, many think an accord will have to be hammered out by the end of the holiday weekend.

Deferring just a few days of non-interest obligations could allow the Treasury to limp to the June 15 corporate tax collection date, at which time the infusion of cash will restore solvency. This action might face legal challenges, though, and could prompt downgrades of U.S. government debt.

The negotiations do reveal a structural shift in the role of government spending and fiscal policy. The debate has focused on the extent of spending caps, and less on cuts. Unlike the popular sentiment that led to the 2011 showdown, this year has not featured a Tea Party caucus advocating for smaller government and major reductions of government programs.

A sustainable solution to balancing the budget will take more than a hurried package of spending concessions. The Debt Fixer budget calculator published by the Committee for a Responsible Federal Budget demonstrates the difficulty of balancing the books. Balancing the budget overnight is not feasible. Reducing debt over a span of ten years would require a broad, deep and contentious array of spending cuts, or a mix of cuts and tax increases.

Given the limited room to reduce spending, we anticipate the consequences of the eventual deal will not be especially damaging to economic prospects. This was a key concern in 2011: The concessions made to lift the debt ceiling raised fears of an economic slowdown. The rescinded COVID funds will not be a regrettable loss; with the pandemic emergency formally concluded, any money not spent was an over-allocation. Holding spending steady is a fair outcome after a 15% increase in non-defense discretionary outlays from fiscal year 2019 to 2022. The caps will not alter the domestic project funding allocated in the Infrastructure Investment and Jobs Act, CHIPS Act, and Inflation Reduction Act.

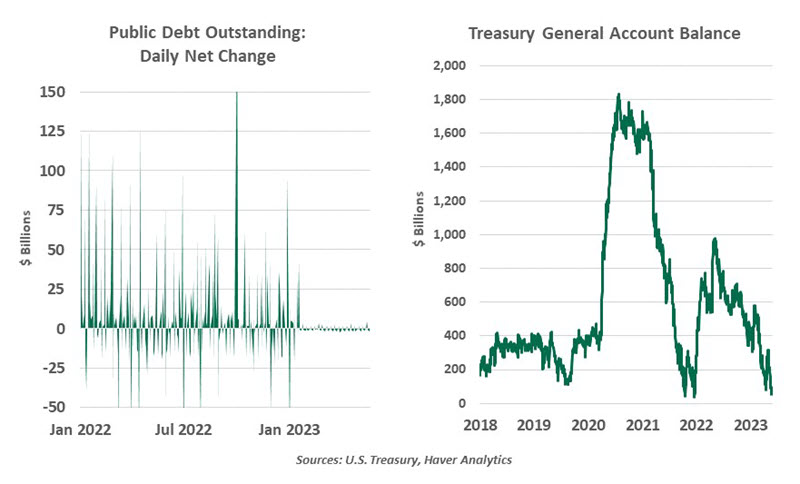

When and if a deal is agreed, it will be back to business as usual for the federal government. For the Treasury, that will mean a return to issuing debt, making up for months of no net issuance since extraordinary measures began in January. Rebuilding the Treasury General Account just to its pre-COVID level will entail over $300 billion of Treasury security issuance, with much greater amounts likely to follow in the balance of the year.

Those new securities will absorb some of the liquidity that remains awash in the system. This may prove to be competition for flush money market funds and struggling bank deposit balances. Another source of outsized flows will add to volatility in the financial sector at an inopportune time.

We hope that today’s negotiations will yield an agreement that defers any need to revisit the debt limit for a very long time. The longer we can go without revisiting this topic, the better for everyone.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust