I am a city kid, but my wife grew up in the suburbs. We had a brief discussion about where we would live after we got married, and ended up less than a mile from my in-laws. My influence over family decisions has always been very modest.

From that point, I became a heavy user of regional mass transit. The elements of routine became deeply ingrained over the course of more than 35 years: taking the same trains, sitting in the same seats next to the same people almost every day. I was able to monitor construction projects along the tracks brick by brick as we passed by each day, and I knew all of the conductors by name.

I took the train this week for the first time in a long while. The car was nearly empty, and I didn’t recognize any of the other occupants. The half-hour ride left me nostalgic, and just a little bit sad.

The melancholy I felt is nothing compared to the desolation that must pervade the management meetings at commuter rail lines. The pandemic hit this sector very hard, and prospects for a full recovery are dim. Emergency support for the sector is scheduled to diminish over the next few years. Financial pressure is building on the carriers, their passengers, their pensioners and the communities that rely on them.

According to the Census Bureau, about 8 million workers used public transportation each day to reach their jobs prior to the pandemic. This represents about 5% of the labor force, with those numbers heavily concentrated in the country’s largest urban areas.

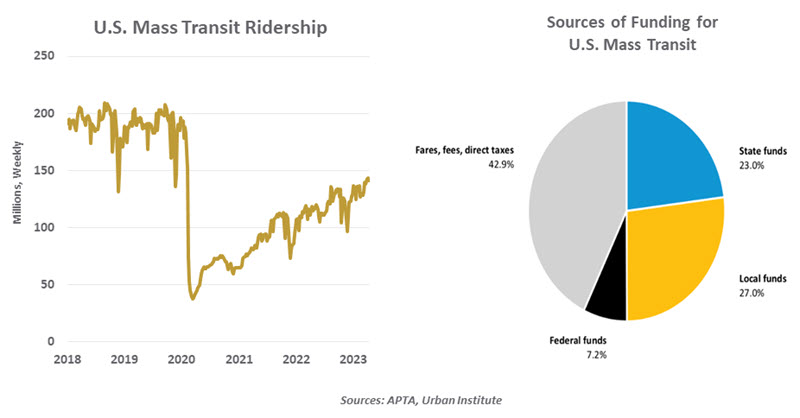

In aggregate, ridership on mass transit in the United States is only 75% of the pre-pandemic level. Public health is no longer a deterrent, but hybrid work has become fully established in the post-pandemic era. Employees are in offices less often, and less likely to take mass transit to get there.

Reacting to the decrease in passengers, systems have reduced schedules, which also serves as a deterrent to usage.

Mass transit has never been financially self-sufficient. Its solvency relies on revenue sources other than fares, which account for less than a quarter of overall income. Portions of sales and property taxes are directed to regional carriers; direct subsidies from state and local governments are also an important part of the equation.

The federal government stepped forward in a substantial way in the wake of COVID-19. $69 billion in relief for mass transit was included as part of three separate bills aimed at dealing with the consequences of the pandemic. The Infrastructure Investment and Jobs Act set aside additional money for transit systems through 2026.

But the aid will not be enough to prevent substantial operating deficits from reappearing. A Bloomberg study of the country’s top eight U.S. transportation agencies concluded that they will face a $6.6 billion shortfall through fiscal year 2026. The finances of state and local governments are limited, and it is highly unlikely that they will be able to fill a hole that large.

To make matters worse, U.S. transit systems have an estimated $31 billion of unfunded pension liabilities and $18 billion of other unfunded post-employment benefits. Unlike private-sector retirement plans, these obligations cannot be reduced or reassigned in the event of financial distress.

Absent additional support, fares will be raised and service will be cut. Those steps will decrease ridership even more, furthering a downward spiral that will strand passengers and strain taxpayers. The implications for urban labor forces could be significant, and the challenge of revitalizing urban centers will become more difficult. Mass transit subsidies can be justified in a number of ways, but support for them will be limited by the fact that most Americans rarely ride a train or a bus.

I closed my eyes on the ride home. I could still envision my younger self sitting with friends, recapping the day and sharing a laugh (not to mention an occasional refreshment). When I returned to the present, I saw rows of empty seats and heard no ambient conversation. As Tom Wolfe might observe, you can’t go home on the train again.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust