Macro Tailwinds for Emerging Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDavid Dali, Head of Portfolio Strategy, provides his 12-month outlook for global equity markets.

Macro Tailwinds for Emerging Markets

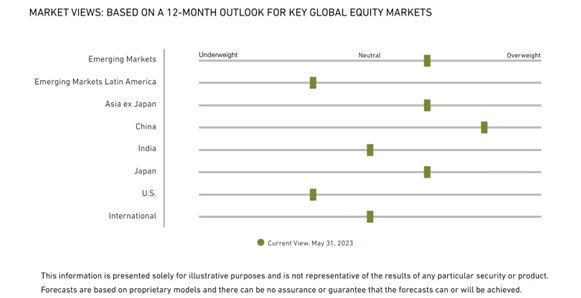

While investment sentiment has softened since January, I remain positive toward emerging markets and Japan given their relatively attractive valuations and the prospect of a more favorable macro climate ahead.

Emerging Markets

- Emerging markets (EM) have endured negative sentiment over China and heightened fears of a policy-induced global slowdown. Yet going forward I support an overweight position due to the positive trajectory of EM economies versus developed market (DM) peers, valuations that assume elevated risk premiums, relatively robust earnings expectations, and peaking in U.S. dollar strength.

- Regionally, I have an underweight stance in Latin America given the relative outperformance at the start of 2023. While Brazil and Mexico have maintained extraordinarily tight monetary policies which should support their currencies, I expect the recent outperformance of Mexico’s equity markets to wane and Brazil’s fiscal discipline to remain a formidable challenge.

- I remain more positive toward Asia ex Japan. South Korea and Taiwan are susceptible to swings in the world economy; however, barring a pronounced global downturn both should experience steady demand for their advanced technology and manufactured goods and services.

- Looking at single countries, the direction of China’s recovery, to me, seems clear and upward-sloping. The ‘valuations versus expected earnings’ equation also clearly supports higher equity prices medium term. The question remains whether geopolitical tensions will allow for an improvement in sentiment. In my view, fundamentals and earnings will prevail and China should be one of the best performers in the coming 12 months.

- India’s six-month underperformance has been significant and index valuations have moved from relatively ‘very overvalued to just ‘mildly over-valued.’ The country’s equity markets remain a beneficiary of U.S.–China tensions and its economy is resilient and robust.

Developed Markets

- In the U.S., inflation-led pricing power has allowed companies to avoid a hit to earnings so far; however, regional bank stress will likely restrict credit just as higher rates begin to hamper consumer demand. As a result, I would expect a more difficult earnings environment in the next 12 months amid already elevated valuations.

- Japan has been buoyed by China’s re-opening and relaxation of international travel restrictions. In addition, Japan is increasingly becoming a ‘friendly’ destination for advanced technology manufacturing. The central bank’s potentially smooth exit from its yield curve control (YCC) policy and the attractively valued currency make Japan one of the most defensive developed markets.

- Europe faces macro headwinds, including volatile energy prices, the impact of the war in Ukraine, tightening financial conditions, and lower earnings-growth consensus. Companies in defensive sectors such as health care or those exposed to recovering economies in Asia should fare better during a global slowdown.

David Dali has spent much of his career in broad emerging markets as a macro-focused portfolio manager, investing in equities, fixed income, currencies, and derivatives.

Notes:

Emerging Markets is based on the MSCI Emerging Markets Index, which captures large and mid-cap representation across 24 Emerging Markets countries. Constituents include Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and the United Arab Emirates.

Emerging Markets Latin America is based on the MSCI Emerging Markets Latin America Index, which captures large and mid-cap representation across five Emerging Markets countries in Latin America, including Brazil, Chile, Colombia, Mexico, and Peru.

Asia ex Japan is based on the MSCI AC Asia ex Japan Index, which captures large and mid-cap representation across two of three Developed Markets (DM) countries, excluding Japan, and eight Emerging Markets (EM) countries in Asia. DM countries include Hong Kong and Singapore. EM countries include China, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan, and Thailand.

China is based on the MSCI China Index, which captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips, and foreign listings (e.g. ADRs).

India is based on the MSCI India index, which is designed to measure the performance of the large and mid-cap segments of the Indian market.

Japan is based on the MSCI Japan index, which is designed to measure the performance of the large and mid-cap segments of the Japanese market.

U.S. is based on the MSCI USA index, which is designed to measure the performance of the large and mid-cap segments of the U.S. market.

International is based on the MSCI World ex USA index, which captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries-- excluding the U.S. DM countries include Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the U.K.

You should carefully consider the investment objectives, risks, charges, and expenses of the Matthews Asia Funds before making an investment decision. A prospectus or summary prospectus with this and other information about the Funds may be obtained by visiting matthewsasia.com. Please read the prospectus carefully before investing.

Investments involve risks, including possible loss of principal. Investments in international, emerging, and frontier markets involve risks such as economic, social, and political instability, market illiquidity, currency fluctuations, high levels of volatility, and limited regulation, which may adversely affect the value of the Fund's assets. Additionally, investing in emerging and frontier securities involves greater risks than investing in securities of developed markets, as issuers in these countries generally disclose less financial and other information publicly or restrict access to certain information from review by non-domestic authorities. Emerging and frontier markets tend to have less stringent and less uniform accounting, auditing, and financial reporting standards, limited regulatory or governmental oversight, and limited investor protection or rights to take action against issuers, resulting in potential material risks to investors.

Investing in small- and mid-size companies is more risky than investing in larger companies as they may be more volatile and less liquid than large companies. In addition, single-country funds may be subject to a higher degree of market risk than diversified funds because of their concentration in a specific industry, sector, or geographic location. Pandemics and other public health emergencies can result in market volatility and disruption.

Fund holdings are subject to change and risk. For current holdings, please visit each Fund’s individual overview page.

ETFs may trade at a premium or discount to NAV. Shares of any ETF are bought and sold at market prices (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

The views and information discussed in this report are as of the date of publication, are subject to change, and may not reflect current views. The views expressed are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific investment vehicles.

The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information. Matthews International Capital Management, LLC is the advisor to the Matthews Asia Funds.

Matthews Asia Funds are distributed in the United States by Foreside Funds Distributors LLC.

Matthews Asia Funds are distributed in Latin America by Picton S.A.

© 2023 Matthews International Capital Management, LLC.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All