New findings from EBRI’s recently released 2023 Retirement Confidence Survey reveal what’s top of mind for American workers and retirees. Below, we look at two key findings – alongside ways the industry is responding.

1. Confidence and the need for income

Retirement confidence took a scary, double-digit plunge this year, a decline not seen since the 2008 financial crisis.

In a sense, it’s hardly surprising. Our Read on Retirement survey from last year found that pandemic-era hardships knocked 42% of workplace savers off track for retirement. And 2022 was a particularly rough year for the markets. Recordkeeper data suggests retirement plan balances took a 20% to 25% hit.1

Yet, for the most part, participants stayed the course. Contribution rates mostly held steady, with fewer participants taking loans or hardship withdrawals from their 401(k)s.2 To us, this underscores the stickiness of savings habits and the effectiveness of features like auto-enrollment and auto-escalation, which have become defined contribution (DC) plan mainstays.

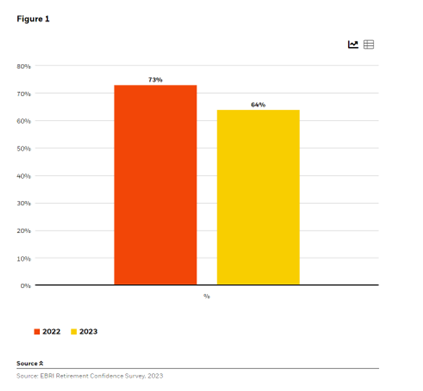

Still, a deeper dive into the confidence question reveals a different concern. One that has to do with the other side of the retirement equation – not saving, but spending. The survey found that only slightly over half of workers believe they will have enough money to last their entire lives. And just under two-thirds of workers are confident they know how much to withdraw from their retirement savings.

Worker confidence in how much to withdraw in retirement3

Correspondingly, savers ranked lifetime income products first among the most valuable potential plan improvements. What’s more, two-thirds of retirees and almost three-quarters of workers say they would prioritize income stability over preserving principal.

2. Spending and the inflation situation

The rising cost of living is a top concern for both workers and retirees. In fact, EBRI reports that two in five workers don’t believe their savings will keep up with inflation in retirement.

These concerns are understandable. Higher interest rates and tightening financial conditions (including labor shortages which, ironically, are partly due to retirement) are hitting the economy, affecting people’s ability to pay for today and save for the future.

In fact, EBRI finds that half of retirees say spending is higher than they expected, especially in categories like healthcare and housing. This tracks with a recent in-house analysis from BlackRock, which found that elderly Americans (65+) consistently spend up to four percentage points more on housing and healthcare than any other age cohort.4 And – to add insult to injury – inflation in both of these categories outpace increases in the CPI.5

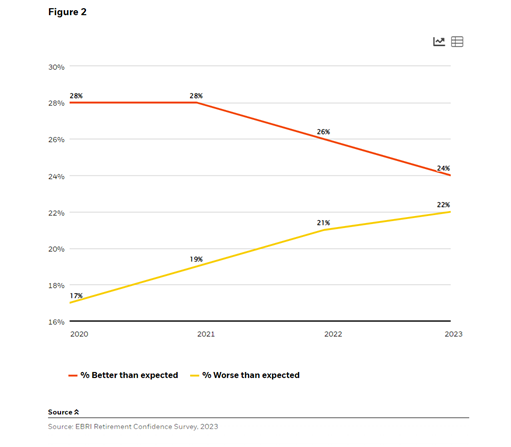

Of course, the rub with inflation is that more does not mean better. Despite the increase in elderly spending, lifestyle appears to be declining. The number of retirees who feel that their overall lifestyle in retirement is worse than expected has been growing each year, according to EBRI.

Retiree sentiment on overall lifestyle in retirement6

Where do we go from here?

At BlackRock, our investment philosophy has always been to build holistic solutions that provide consistent spending to and through retirement. That’s why we are continually seeking to address the key risks that matter at various stages of the retirement journey – from longevity and savings risks to market and purchasing power risks. In today’s environment of heightened inflation and growing demand for retirement spending solutions, these core beliefs are even more important.

And it’s clear that we also need to make it easier for more Americans to use these kinds of solutions. For the 57 million workers who lack access to a workplace plan, preparing for retirement remains a challenge.7 In fact, EBRI found that, while 25% of workers with access report having less than $10,000 in savings, this rate jumps to 70% among workers who lack access. While SECURE 2.0 included important provisions to expand access – particularly to those working part-time or for smaller businesses – there’s more we can and should do across the industry.

State-sponsored retirement plans offer one solution. Since the launch of the first state plan back in 2017 (Oregon), eight more are up and running (including Virginia’s pilot), with others set to launch soon. We applaud these efforts to expand access – without creating additional administrative burdens for small businesses. In line with this thinking, tech-enabled 401(k) plan providers like Human Interest8 and Vestwell also aim to streamline retirement plan offerings for small and medium-sized businesses. While these examples are far from exhaustive, we continue to be encouraged by efforts across the public and private sectors to build a more inclusive and secure retirement system.

1 Various recordkeepers, BlackRock analysis, 2023.

2 Bank of America, 401(k) Participant Pulse, Q4 2022

3 EBRI Retirement Confidence Survey, 2023

4 BlackRock, 2022.

5 Peterson-KFF, Health System Tracker, 2023 and The White House, An Update on Housing Inflation and the Consumer Price Index, 2023

6 EBRI Retirement Confidence Survey, 2023

7 AARP, 2022

8 BlackRock recently made a minority investment in Human Interest (link)

The 2023 Retirement Confidence Survey, co-sponsored by BlackRock, was conducted online January 5 through February 2, 2023, by the Employee Benefit Research Institute (EBRI) and Greenwald Research. All respondents were ages 25 or older. The survey included 1,320 workers and 1,217 retirees in the United States.

The BlackRock Read on Retirement provides insights from a research study of over 300 large defined contribution plan sponsors, 1,300 workplace retirement plan savers, 1,300 independent savers, and 300 retired workplace savers in the United States. The survey is executed by Escalent, an independent research company. All respondents were interviewed using an online survey conducted from March 25 through April 30, 2022.

This material is provided for educational purposes only and should not be construed as research. The information presented is not a complete analysis of the global retirement landscape.

The opinions expressed may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock, Inc. and/or its subsidiaries (together, “BlackRock”) to be reliable. No representation is made that this information is accurate or complete. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

None of the information constitutes a recommendation by BlackRock, an offer to sell, or a solicitation of any offer to buy or sell any securities, product, or service. The information is not intended to provide investment advice. BlackRock does not guarantee the suitability of the potential value of any particular investment. The information contained herein may not be relied upon by you in evaluating the merits of investing in any investment.

Investing involves risk, including possible loss of principal.

No part of this material may be reproduced, stored in any retrieval system, or transmitted in any form or by any means, electronic, mechanical, recording, or otherwise, without the prior written consent of BlackRock. This publication is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© BlackRock

Read more commentaries by BlackRock