What Changed with the Pandemic (And What Didn’t)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

1. Digitalization Accelerated and There’s No Going Back—Businesses that developed digital techniques to serve customers and organize workforces created big competitive advantages. They should thrive as the pace of technological advancements continue.

2. Dangers of the Herd—The pandemic re-emphasized the pitfalls of following the herd. Easy money can cause problems and dull the senses to the need to diversify and invest in quality companies that may be out of favor.

3. The Value of Mass Markets—Some companies targeted niche rather than mass markets even though they initially pitched them as huge total addressable markets (TAMs). We are mostly interested in identifying companies that are successfully addressing realistically large TAMs.

4. E-commerce Growth Didn’t Endure—E-commerce exploded in every country during the pandemic but it’s no longer growing fast in every emerging market. Being selective about e-commerce opportunities is critical.

5. Renewable Energy Is a Mining Opportunity—It’s clear that in the move to the new energy economy, a lot more old-economy materials will be needed. Mining companies located in emerging markets have to be part of the solution.

6. Navigating Inflation and Capital Needs—As the pandemic grew, countries around the world turned to monetary and fiscal stimulus. In our view, the fiscal and monetary responsibility demonstrated by emerging markets indicates that these markets can provide steadier investment opportunities than in their distant past.

It’s been around three years since COVID began to shake up the world’s societies, economies and markets. As the pandemic unfolded in 2020 and 2021, it seemed its effects on human behavior would be profound and long term. While the full impact of COVID will likely take years to grasp, it’s a good moment to think about the changes to global equity markets that could be here to stay as well as the changes that may not be as long lasting as we thought.

Here I consider six themes that emerged in the pandemic. Some investors were led astray by them, and some investors used them to their advantage. But all these themes, I believe, can serve as anchor points in our search for emerging market-growth opportunities.

1. Digitalization Accelerated and There’s No Going Back

The most important change from the pandemic, in my view, was acceleration of digitalization. As we found ourselves locked into our homes, working from there and having our kids educated from there, we began to inhabit the digital world more fully and more quickly than we had imagined. Businesses that could digitally reach and serve customers and connect and organize their own workforces, found themselves at a huge advantage. Two very different companies that embraced the pandemic’s digital calling were Globant, a fast-moving software company based in Buenos Aires, and Prudential Plc, a financial bastion of the City of London.

Globant was perfectly placed in the pandemic. It was founded about 20 years ago in Buenos Aires by ‘four friends in a bar,’ as the company put it, to help companies build software that enhances their digital customer experience. Today, there are more than 27,000 highly skilled “globers” in more than 25 countries who serve a blue-chip customer base including American Express, Coca-Cola, Electronic Arts, Pernod Ricard and Unilever.

When the pandemic took hold, Globant quickly pivoted to the needs of working from home. I remember wondering whether its tightly knit ‘studios’ and product work groups could smoothly transition to collaborating remotely, but the company pulled it off. The business accelerated dramatically: from mid-20s percentage revenue growth in the years before the pandemic, to 59% growth in 2021, and 37% growth in 2022. Growth will settle into a lower level in the post-pandemic world in our view but at a still very healthy pace. For Globant and other companies like it the pandemic appears to have reset them to a higher plateau from which they should continue to grow rapidly.

As an aside, Globant has for years has been building tools that help its own coders produce code more easily and efficiently with the potential goal of making these tools available to outside clients. This was also one of the original goals of OpenAI, the entity behind ChatGPT, the application that has become a lightning rod for the use of artificial intelligence in recent months.

Prudential Plc, the 175 year-old pan-Asian insurer headquartered in the City of London, credits its digital strategy Pulse with not only helping the company bridge the gap to re-opening during the pandemic years but for improving the way the whole business is run.

“Pulse is not just about customer acquisition,” the company told us in a recent meeting at our offices in San Francisco. “Pulse is an enabler for our agents throughout the value chain. There are tools within Pulse designed to enhance the process of recruiting and training our agents, to help manage their day-to-day activities, help their sales activity and all the way through to fulfillment of policy sales and servicing of clients.”

Companies, big and small, that innovated digitally during the pandemic thrived and are in strong positions for what comes next. It showed the ability of markets to surprise and delight consumers and there’s no doubt the pandemic hot-housed digital innovation with long-term implications for the way consumers behave and companies operate.

2. Dangers of the Herd

The ‘greed and fear’ polarity of market behavior is understandable and probably will never change. There are always incentives to follow the herd, but we believe failing to diversify and anchoring to herd behavior—no matter how powerful—is ultimately dangerous and bound to lead to poor investment results.

The consequences of following the herd are still playing out. In the case of failed U.S. lender Silicon Valley Bank (SVB), it is stunning to contemplate how a combination of easy money from pandemic stimulus and skyrocketing growth stocks turbo-charged the startup ecosystem in Silicon Valley, leading deposits at SVB to surge to $189 billion in 2021 from $49 billion in 2018. As an emerging markets investor who has studied banks my whole career, I question the wisdom of any bank that is completely dependent on one sector for its deposits and its lending business. If I ran an oil company, I would never park my deposits in a bank that only served the petroleum industry. When oil is $100 a barrel and oil companies are flush with cash, such a bank could look stable. But we all know that oil can go to $50 tomorrow—and if it did, that bank would suddenly be unstable as many depositors would be forced to take their cash out to fund operations.

It's difficult to imagine that a business model like SVB—embraced by depositors, investors and regulators—could exist in an emerging market. That’s not because emerging markets are less profit-oriented or less naturally prone to herd-like behavior; it’s because investors, depositors and regulators there have learned common sense lessons about what works and what doesn’t.

Our core emerging markets portfolio tends to be growth-oriented, and we owned growth stocks during their strong run in the peak pandemic period of 2020 and 2021. But we also owned plenty of quality stocks in sectors that were temporarily out of favor, like materials and consumer markets. The pandemic reinforced some hard lessons for businesses and investors alike about the consequences of not diversifying and blindly following the herd. They can be summed up by three propositions:

- Don’t blindly follow the herd

- Reduce your potential risk by diversifying

- Too much easy money will cause problems

3. The Value of Mass Markets

In the pandemic period, markets became excited about developments that, in my view, appeared to address small, niche markets. The realistic Total Addressable Markets (TAMs)—the overall revenue opportunity that is available for a product or service if 100% of market share is achieved—of these activities may turn out to be more limited than what their proponents argued during the pandemic. Examples of high-flyers included cryptocurrencies, digital banks, the metaverse, non-fungible tokens (NFTs), food delivery companies, and even electric vehicle (EV) startups. In each case, these companies look to be addressing niche markets and not mass markets, even though they were initially pitched to have massive TAMs.

Take EVs. There’s no question that the global auto market is a large TAM—perhaps more than $3 trillion today. If all of that auto market is eventually realized for EVs, and if one or two companies can dominate that TAM, it would seem that they should be able to create a lot of value for their shareholders. But there are several problems with this line of reasoning, namely:

- Sales aren’t profit

- Profit margins and return on investment (ROI) in the auto industry have generally been low, consistent with a commoditized industry

- EVs are expensive compared to internal combustion vehicles and they’ve become more expensive in the last year as some battery material prices rose dramatically

- Much of the world can’t afford expensive cars and EVs aren’t yet available for mass markets in the developed or emerging world

- Chinese companies are producing some affordable, relatively simple EVs but it can be intensely and even destructively competitive

The TAM of the EV industry isn’t a meaningful metric—we need to narrow the scope. For example, if we define the TAM of EVs as sales which produce a good margin and ROI, we reduce that $3 trillion number by a huge discount—perhaps by more than 90%. If we consider how that number may change over time, and the number of EV producers and which ones will maintain a sustainable competitive edge, the realistic addressable market may be even lower. Call that the TAAM—the Total Addressable Attractive Market and it’s fair to say that resembles more of a niche market than a mass market.

Elon Musk has yet to become the Henry Ford of EVs. Until his very recent cost cuts in some markets, Teslas were only affordable to premium car buyers. If a Henry Ford of EVs emerges—selling cars profitably to the mass market—they may come from China, a possibility we are studying.

Another industry where niche and mass markets became a little blurred was banking. A number of digital banks have sprung up in emerging markets over the last three years, attracting millions of active users. Some digital banks have even demonstrated that certain loans can be made on the strength of data and algorithms versus using traditional underwriting methodologies. But it is unlikely that these banks will ever make as much profit as incumbent banks do, or even close to it. If net income is divided by active users, the best digital banks today are earning $1-$5 of annual net income per user. But incumbent banks make $30, $50 and even $80 of net income per user because they are embedded very broadly in the economies they serve, and they have been targeting the largest profit pools in those economies’ banking sectors for decades.

While digital banks have succeeded in improving the online/mobile banking user experience and have begun to reduce some of the fees which incumbent banks have been charging, they have also spurred the most able incumbents to adopt digitalization, reduce expenses and maintain a firm hold on the most profitable banking segments of their economies. Digital bank challengers may have in fact made many incumbent banks stronger. The future of banking may therefore lie more in the digitalization of traditional banks and the incremental improvements this brings to customers, as opposed to a new set of powerful digitally native banks.

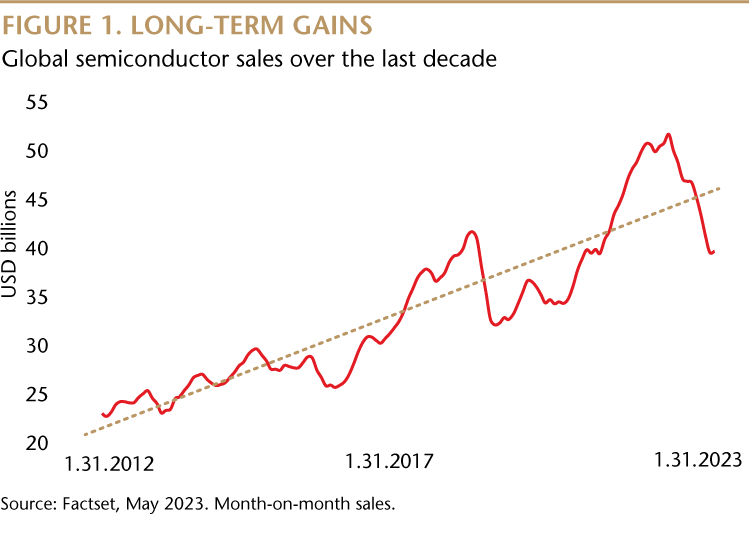

A more attractive structural industry than EVs and digital banks is advanced semiconductors. The TAAM of semiconductors is large because companies have built competitive advantages which may endure, whether they are Taiwan Semiconductor Manufacturing Co. (TSMC), Samsung Electronics, or one of the many thriving equipment makers. It’s true that the industry is prone to cyclicality and it certainly went through a massive up-cycle during the pandemic—another consequence of the acceleration in digital applications around the world. But this cyclicality is around a long-term upward trend. If a semiconductor company can maintain a technological advantage, there is a good chance the company will add value to the world and thus value to its shareholders. The semiconductor market has companies that have built strong portfolios of assets capable of producing superior free cash flow and ROI over time. They are providing materials which are already embedded in our everyday lives and will become even more so over time.

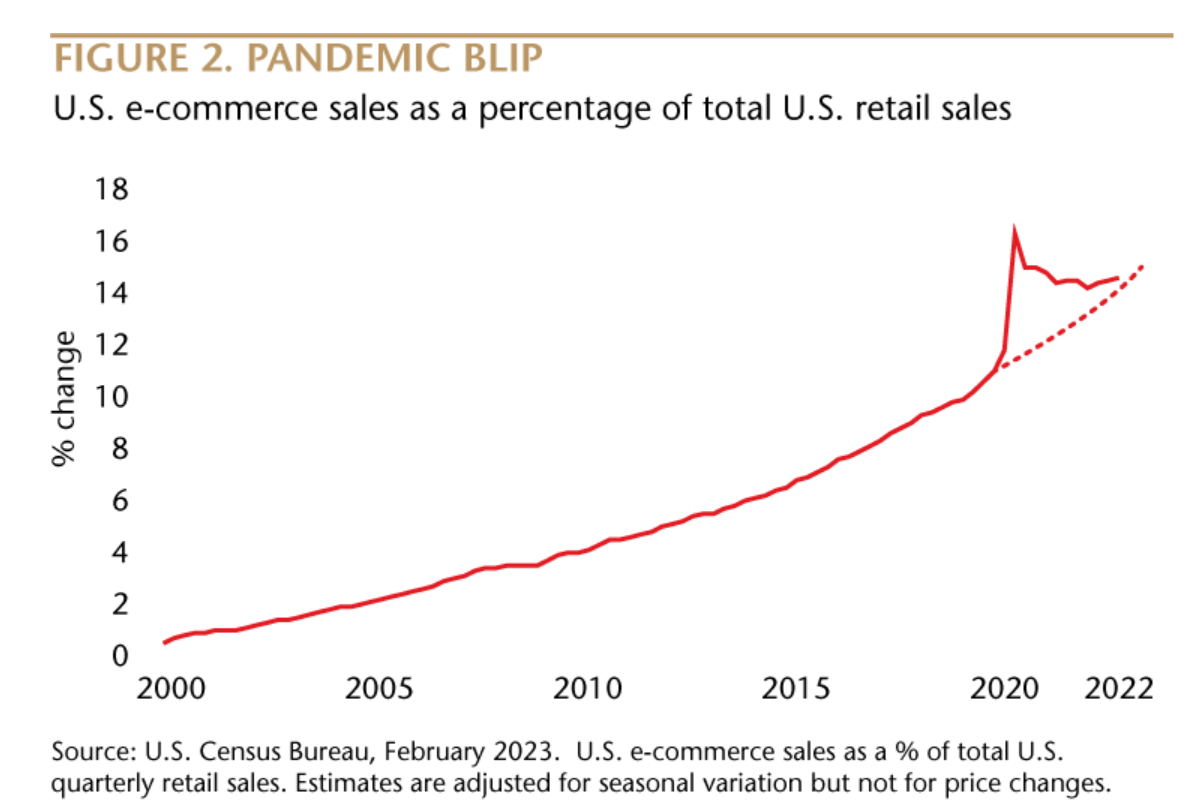

4. E-commerce Growth Didn’t Endure

Locked in our homes with stores shuttered, we embraced e-commerce in the pandemic. Grandparents became Amazon Prime members. As e-commerce skyrocketed, it felt like retail had been re-made forever and that e-commerce—convenient and fast—would continue to gain a big share of wallet even after the pandemic. But by the summer of 2022, the hangover had started. The dawning realization that e-commerce growth was fading fast was summarized by Tobi Lutke, the CEO of Shopify, a Canadian distribution platform for retailers. In a letter to employees he explained that during the pandemic the company made a bet that the surge in e-commerce adoption rates it was seeing was a permanent rather than a temporary leap forward. The bet didn’t pay off, Lutke concedes, and the company had to retrench.

Today, e-commerce revenue growth in many developed and emerging markets is settling into a growth rate which is similar to, or perhaps marginally above, nominal GDP growth. E-commerce companies are becoming retailers, as retailers become e-commerce companies. Analyzing the outlook of e-commerce companies will be more like analyzing a traditional retailer than a technology company.

But we are still watching for particular opportunities. There may be pockets in e-commerce where growth will be fast for a while and margins could be attractive. That’s not likely in China, where e-commerce penetration is above that of many developed markets and, as in many sectors in China, competition is fierce. But e-commerce penetration in Latin American markets is low and leaders are solidifying their positions. In addition, parts of Central Europe, Central Asia and Southeast Asia may also catch up for a while. And there may also be companies which produce creative, valuable solutions within sections of the e-commerce value chain.

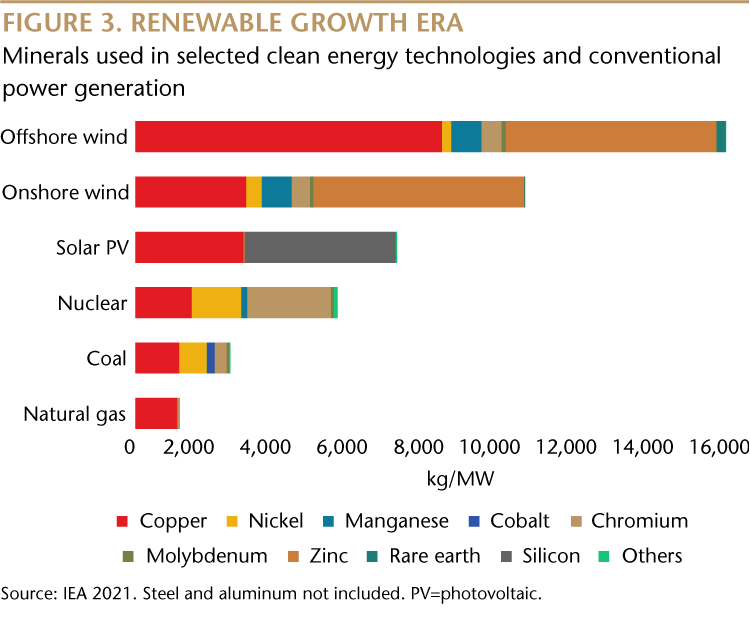

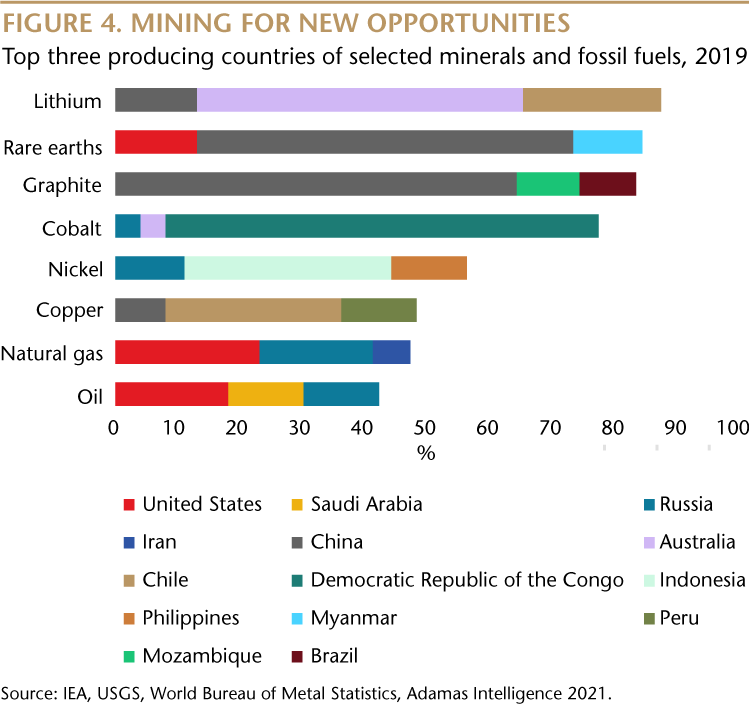

5. Renewable Energy Is a Mining Opportunity

Though energy prices spiked during the pandemic, political leaders, company managements and boards continued to advocate for a transition away from fossil fuels. And in our view, emerging markets will play a key role in new energy transitions. Mining resources are overwhelmingly located in developing countries. In the processing of those minerals and materials into finished products, China, for example, already has an outsized presence. We believe mining companies located in emerging markets have to be part of the transition solution and that investors and consumers at large need to recognize that products designed for the sustainable space, like EVs, and methods for generating renewable energy, require old economy processes such as mining. The switch to sustainable energy will also be a phased transition. Natural gas and even oil will have a part to play in our energy needs for decades to come.

As the renewable energy market grows—the International Energy Agency (IEA) forecasts demand for renewable energy to grow strongly through 2030—it’s becoming clear that a lot more old-economy materials and energy sources will be needed. Take copper, for example. When you move from an internal combustion engine to an EV, the two main metals are the same: steel and aluminum. But there is a much bigger need for copper. There’s a copper coil in the drive motor which converts electrical energy into mechanical energy. Pure EV motors can have more than a mile of copper wiring in them. That electricity produced by motors is delivered to the car through copper wiring. And in the battery pack itself, copper is one of many materials, including steel, iron, graphite, aluminum, nickel, cobalt and lithium. Similarly, a whole range of metals and materials is needed in solar and wind installations.

We spend a lot of time studying and meeting with mining companies to understand their capital allocation decisions and outlooks and we’ve owned mining stocks since the inception of the Matthews Emerging Markets Equity Fund portfolio. I asked TotalEnergies, the French energy giant, about the impact on the energy market of the Russian invasion of Ukraine in 2022. “It was a wakeup call,’’ they said. “The hope that you can’t just turn off one system and turn on another isn’t feasible. There was a true panic in Europe as the pipelines shut down, that there wouldn’t be enough energy. Perhaps we had a little too much focus on tomorrow’s system.”

TotalEnergies, which has growth projects in liquified natural gas, crude oil, solar, wind and hydrogen, is among a growing number of large energy companies pivoting to sustainable energy sources. And the company sees developed countries playing a key role in the sustainable shift. As it says in its 2022 energy outlook document, the shift to a new low carbon energy system at a global scale “will not happen without richer countries supporting emerging ones by promoting a just energy transition’’ via investments, technology transfers and training.

6. Navigating inflation and capital needs

As the pandemic grew, countries around the world turned to monetary and fiscal stimulus in an effort to stabilize economies teetering from lockdowns. But not all stimulus was equal—in fact, wealthy countries stimulated much more. Emerging markets were generally more responsible fiscally and in some cases were more responsible with monetary policy as well. The independent actions of central banks in emerging markets, as they tightened policy in the face of inflation, was a welcome surprise for some senior banking executives we spoke to. From our own experience it was very clear that many central banks were erring on the side of caution and prudence.

At the corporate level, we find that banks in emerging markets are also generally well capitalized. And the stocks in our portfolio tend to have strong balance sheets, healthy cash flows, and a track record of successfully navigating difficult macro-economic conditions. The pandemic tested companies, markets and economies and, in our view, emerging markets displayed a resilience that continued to build on their track record of overcoming adversity.

As developed markets head into a tighter financial environment and economic growth slows, emerging markets remain generally well capitalized, with their banks and companies well positioned to navigate through and grow in the new macro world.

Savvier and Wiser

Recently, the MIT scientist and podcaster Lex Fridman speculated that there was something about the pandemic which made it even more difficult for people to overcome their biases and consider other viewpoints. As he put it, “there’s almost an emotional barrier before you even get to the intellectual error,” and this emotional barrier he says hardened during the pandemic. Being locked inside with more time to consume social media may have entrenched many people’s biases, said Fridman, and made it more difficult for them to “get out of their heads” and consider alternative points of view.

As a reaction to this, some of us are forcing ourselves to ‘steel man’ the other side’s argument. The steel man argument, as opposed to the ‘straw man’ argument, is the strongest version of the other side’s argument which one can articulate. Knocking down a straw man is easy; knocking down a steel man requires deeper thinking, and intellectual humility. It’s an approach we are embracing in our discussions and reviews of our portfolio positions. It’s critical that we are always asking ourselves what is the strongest case against owning the stocks that we do. Likewise, we ask ourselves, what is the strongest case against not owning the stocks we don’t own.

Our guiding approach to stock selection has been and remains ‘the Five Cs’, and we believe this philosophy has become even more valuable as we seek to produce superior returns for our clients in today’s challenging markets. The competitive position, capital allocation, cash flow, capital structure and character of a company will always be crucial for businesses and stocks, in our view. We find that companies which embrace healthy approaches to each of these fundamentals tend to do well—and that these fundamentals are even more important, over time, than what country or sector the company is in.

FIGURE 5: THE FIVE C’S OF A GOOD COMPANY

The economic parameters we are now living within today are very different to the ones we experienced before the pandemic, and which were magnified during the pandemic. There’s no cheap money anymore and so-called ‘growth stories’ aren’t quite so easy to spot. But, crucially, great investment opportunities remain. My six themes, I believe, are useful guideposts for successful long-term investing in a world changed, and changed not so much, by the pandemic.

Alex Zarechnak

Portfolio Manager

Matthews Asia

Notes:

View Matthews Emerging Markets Equity Fund top ten holdings. Current and future holdings are subject to change and risk.

View Matthews Emerging Markets Equity Active ETF top ten holdings. Current and future holdings are subject to change and risk.

View Matthews Emerging Markets ex China ETF top ten holdings. Current and future holdings are subject to change and risk.

Revenue growth is not a measure of future performance. Diversification cannot assure a profit or protect against loss in a down market.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky and volatile than investing in large companies as they may be more volatile and less liquid than larger companies. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All