The Global Economy Is Suffering From Long COVID

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn many respects, COVID-19 was not a temporary disruption.

Three years ago, a biweekly trip to the grocery store was the height of entertainment. It was the only time I ventured outside of my property line, and I tried to make the most of it. I strolled slowly through every aisle to appreciate the change of scenery, even if I didn’t need anything from that particular section. Once, someone asked me to help them get an item off the top shelf; the exchange represented a 100% increase in my network of personal contacts.

Memories like that came up frequently during my trip to China last month, where I compared pandemic experiences with colleagues and clients. COVID is still fresh in their minds, so the past is still somewhat uncomfortable. I told them that each day allows a more complete embrace of normalcy and that the day will come when they’ll reflect on the past three years with some bemusement.

Recent headlines in the United States have declared an official end to the pandemic era. A defining development was the expiration of government programs enacted in 2020 to protect the population. This milestone validated what people have sensed for some time; the virus is no longer very threatening, and our routines are largely unconstrained. But the pandemic has changed life and commerce in unalterable ways. Like many survivors, the global economy is dealing with long COVID.

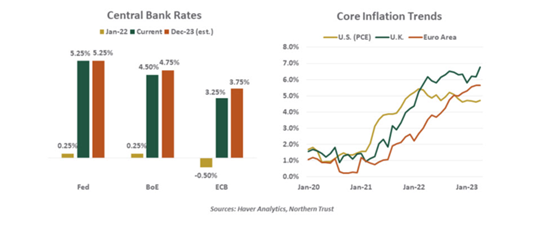

Higher For Longer

In the near term, economies are still recovering from the demand and supply shocks created by the pandemic. The inflation that resulted from the two forces has necessitated more restrictive monetary and fiscal policies around the world. Rapid increases in interest rates have proven difficult for borrowers and contributed to an outbreak of banking stress earlier this year. A higher yield environment may also eventually stress the solvency of some emerging markets.

Governments are paying much more to service their debts, creating uncomfortable discussions over the need for fiscal discipline. We see this in the euro area, where the debate over restoring budget constraints has prompted renewed dissonance between northern and peripheral members. And we saw it in Washington, where the battle over raising the debt ceiling was especially contentious. The U.S. Congressional Budget Office projects that interest will double as a fraction of federal spending by the middle of this century, surpassing Social Security and Medicare.

A higher longer interest rate environment changes the calculus for investors in many ways. Cash has become a much more interesting asset class, and higher costs of capital reduce the value of future earnings from equities. Bond and stock returns have moved more in tandem of late, counter to an enduring principle of portfolio theory.

Central banks are trying to reach peak levels of interest rates, but inflation may have other ideas. Core inflation levels around the world are still well above target, and some have actually increased in recent months. More tightening may be needed, increasing interest rate risks for borrowers and the risks of recession in developed markets. The pandemic may create an era of stress between governments and central banks, with the sanctity of inflation targets called into question.

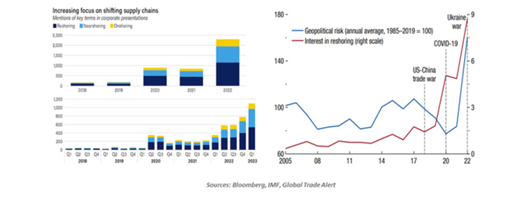

Re-Shoring

In the medium term, the pandemic will accelerate the retreat of global trade. Concerns about international commerce have been building for some time: the downside of financial linkages between countries was illustrated by the global financial crisis, and the free trade/fair trade debate was taken to the next level by the 2016 elections in the United States and Great Britain. The number of restrictive trade actions taken by countries against one another was on a steep rise by the end of the last decade; global trade as a percentage of global gross domestic product (GDP) crested fifteen years ago.

COVID-19 illustrated the level of dependence that countries still had on imports. During the pandemic, snarled supply chains limited the availability of some essential items: a CNN report estimated that 80% of the world’s supply of N95 masks is made in China. Throughout 2020, hospitals in the U.S. and Europe scrambled to get the allocations they needed.

The experience has prompted companies and countries to diversify their sources. Whether as a compliment or as a contingency, the move to “re-shore” production has gathered momentum.

The shift has taken on a strategic element. Last year’s invasion of Ukraine led to a blizzard of economic sanctions against Russia, which forced immediate sourcing shifts for food and energy (among other things). The possibility that similar penalties could be aimed at other aggressors has given momentum to “friend-shoring,” or “de-risking” of networks. Supplies of the most advanced microchips have been a particular focus of these efforts, with a number of new fabrication plants under construction outside of Asia.

COVID-19 has played a supporting, but significant role in the process of de-globalization. An improved tone of international relations could limit trade frictions and reduce the urgency to safeguard supply chains against tail risk. But anxiety over import concentrations, which was on full display during the pandemic, may prove more lasting.

If you believe, as we do, that trade has improved choice, lowered prices, raised aggregate living standards, and reduced the risk of aggression between countries, then the depreciation of the international commercial order will produce the opposite of those effects. None will be pleasant, either economically or socially.

Diminished Capacity

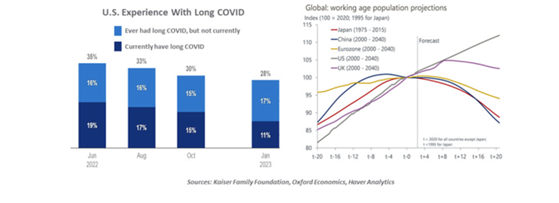

In the long term, the pandemic’s negative influence on demographics and the global labor force will produce substantial economic consequences. Consider:

- The Economist estimates that almost 22 million people had died from COVID-19 infections through May 2022. (This is well above the number officially reported; some countries substantially undercounted the number of fatalities.) That number has almost certainly increased importantly in the wake of China’s recent experience. While elderly populations proved most vulnerable, the mortality rate for working-age women and men also rose sharply.

- Analysis by the Centers for Disease Control and Prevention found that 7.5% of Americans who contracted COVID are still coping with respiratory or cognitive limitations. Similar studies by organizations in other countries have found even higher rates of “Long COVID.” A study by the BBC found that prime-aged workers are most likely to suffer from lingering symptoms. People with this affliction may not be able to work full-time, or at all.

- COVID has been shown to complicate chronic diseases, which has extended its impact on public health. Life expectancy in the United States, which has an above-average incidence of chronic illness, has declined by two full years since 2019. The pandemic has also taken a toll on mental health, with levels of anxiety and addiction higher than they were four years ago.

- Birth rates dropped sharply in 2020 and 2021 across a number of countries. The Brookings Institution estimated that the pandemic created a deficit of 300,000 to 500,000 American children relative to what might have been expected prior to the pandemic. This shortfall is not expected to be made up over time.

- A number of workers retired earlier than expected during the pandemic, with fear of illness a leading motivation. We had thought that improving public health conditions would invite many of them to return to the labor force, but rates of “unretirement” have not risen much above their historical norms.

- Borders closed to protect public health also slowed immigration to a crawl. In many countries, newcomers provide a critical source of economic energy: filling in gaps in the labor markets, starting small businesses, and contributing to innovation. Immigrants tend to have larger families, which provides another demographic dividend.

- Caregiving was disrupted when COVID descended and has never fully recovered. Parents of children and children caring for elderly parents continue to devote more time to supporting loved ones than they did prior to the pandemic.

Global demographics were not in the best shape prior to the pandemic. The current outlook is even more discouraging, and the lower trajectory of future population growth in major economies will limit potential economic growth.

Slower population growth (or outright declines) in developed markets will be in stark contrast to the significant population growth projected for emerging markets. Labor force capacity can be transferred in two ways: through immigration, and through foreign investment that improves human and physical capital overseas. The latter course would position developing countries to export goods and services that larger countries would not have the capacity to produce.

But making the most of offshore populations (and allowing them to realize their full potential) requires openness to trade and immigration, both of which have been the subject of skepticism in many world capitals. The risk for the world is that young populations without prospects may seek to find them elsewhere, producing migration crises the likes of which we have seen in both Europe and the United States.

The Pursuit Of Productivity

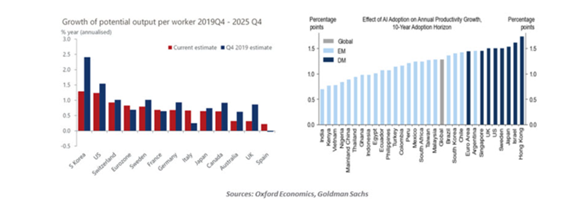

Evidence also suggests that the pandemic has had a negative impact on productivity. Output per hour among workers is growing much more slowly than it was a few years ago: productive investment was depressed during the COVID era, and the adoption of technology may have been slowed by the transition to hybrid work arrangements.

The impact of COVID-19 on education will exact a toll on productivity. Learning from home was no substitute for the classroom, and a number of young people paused (or ended) their undergraduate work. Skills not accumulated will not produce returns to students or to society.

Productivity growth is critical to raising standards of living, and to the ability of countries to keep up with the debts they have accumulated. With labor forces stagnating, it is imperative that those that remain in the workforce make the most of their time.

Perhaps that is why there is such buzz about artificial intelligence (AI). ChatGPT and its ilk brought the state of play firmly into the public consciousness, but the potential of the technology has been rising for some time. The application of AI is expanding continuously, and substantial amounts of capital are being invested in its future. The attention paid to the concept is reflected in the four-fold increase in Google searches on the topic over the last year.

Many observers have arrived at the conclusion that AI will take its place among other transformative technologies throughout history. Goldman Sachs estimates that the adoption of AI will add more than 1% to annual productivity growth across the world, which is an immense improvement.

My partner Ryan Boyle has a healthy skepticism about AI. He cites the “Gartner Hype Cycle,” which tracks how new ideas travel through five phases: triggering, inflated expectations, disillusionment, enlightenment, and productivity. The curve never finishes higher than the peak seen during the interval of inflated expectations; generative AI, in the latest rubric, marks the start of peak hype.

There are other obstacles. AI routines are computationally intensive and will require substantial investments in infrastructure. (Lots and lots of cutting-edge microchips, for starters.) AI can be used for evil as well as good, and for strategic as well as commercial objectives. For those reasons, cross-border collaboration in this area may be difficult to engineer. Ethicists are anxious about the impact of AI more broadly, with the writer Yuval Noah Hariri (author of “Sapiens”) warning that civilization may ultimately be at risk.

Nonetheless, the potential transformations that may be ahead of us are substantial. And the adoption curve may have a sharp upward slope to it. The technological transition may take place more rapidly and people will naturally transition out of the labor force, which will present management challenges. And many younger, highly educated workers will have to up their games as the more routine aspects of their jobs are given over to computers.

Much as we might wish, the pandemic is not in the past. It’s in our present, and in our future. Society has survived the worst of COVID-19, but its after-effects may linger for quite some time.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All