May update

- Munis posted negative total returns but outperformed comparable Treasuries in May.

- Bank portfolio liquidations have been less disruptive than initially feared.

- Better valuations and improving supply and demand dynamics should spur summer strength.

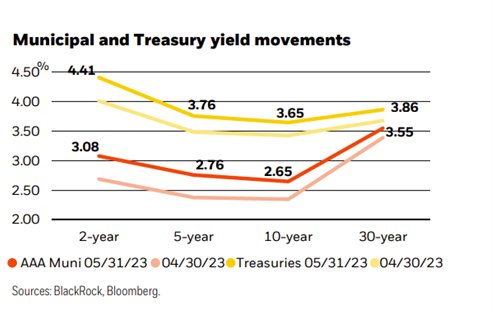

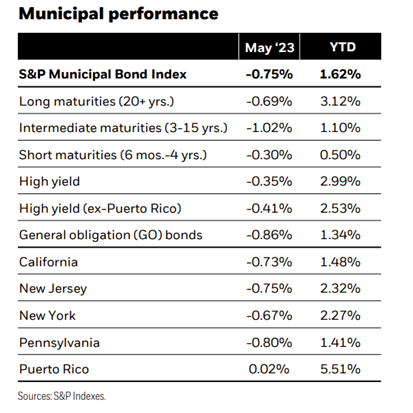

Market overview Municipal bonds posted negative total returns in May amid continuing heightened volatility. Interest rates rose throughout most of the month as banking concerns abated, economic data exceeded expectations, comments from the Federal Reserve turned more hawkish, and debt ceiling negotiations remained contentious to the very end. The Bloomberg Municipal Bond Index returned -0.75%, bringing the year-to-date total return to 1.62%. The asset class underperformed comparable Treasuries in the intermediate part of the curve but outperformed in both the front end and long end. Shorter-duration (i.e., less sensitive to interest rate changes) and triple-B-rated bonds performed best.

Fund flows remained consistently negative but were counterbalanced by manageable primary and secondary supply. The issuance was in line with historical expectations at $31 billion, 2% below the five-year average, and outpaced reinvestment income from maturities, calls, and coupons by $3 billion. As a result, deals were oversubscribed by 4.3 times on average, slightly above the year-to-date average of 4.0 times. At the same time, anticipated bank portfolio liquidations were less disruptive than initially feared. Selling was orderly and resulted in only a negligible month-over-month increase in daily bid-wanted. Lower-coupon bonds with shorter maturities made up the bulk of activity.

We have turned increasingly constructive on the asset class over the near term. Given the recent market adjustment, we believe now is an optimal time to take advantage of better valuations and put money to work ahead of more favorable seasonal supply-and-demand dynamics anticipated in the upcoming summer months.

Strategy insights

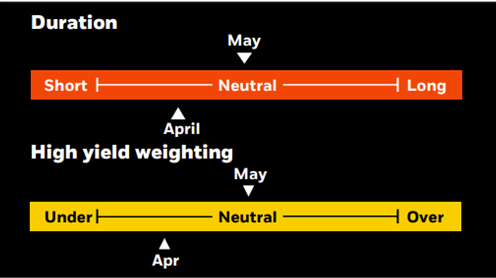

We maintain a neutral-duration posture overall but will look to add on weaknesses. We prefer an up-in-quality bias with a neutral allocation to non-investment grade bonds. We strongly advocate a barbell yield curve strategy, pairing front-end exposure with an increased allocation to the 15– 20-year part of the curve.

Overweight

- Essential-service revenue bonds.

- Select the highest quality state and local issuers with the broadest tax support.

- Flagship universities.

- Select issuers in the high-yield space.

Underweight

- Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies.

- Senior living and long-term care facilities in saturated markets.

- Lower-rated private universities.

- Stand-alone and rural health providers.

Credit headlines

The seven states (CA, AZ, NV, CO, NM, UT, WY) that rely on the Colorado River water system reached an agreement last month to conserve an additional three million-acre-feet of water through 2026. Water levels on the system have been negatively impacted by prolonged periods of drought in the western U.S., which have threatened both water availability and power generation for the region. We consider the agreement an important stabilizing development for the utilities reliant on this vital water source and supportive of a sector we view favorably due to its essentiality and steady financial performance.

Airport and toll system volumes have returned to near-pre COVID-19 levels; however, mass transit systems haven’t enjoyed the same recovery. Several large mass transit systems remain under pressure and continue to confront operational and financial challenges. Ridership recovery from the pandemic has been slow to return as work-from-home initiatives have been broadly embraced by the urban workforce. Low ridership, escalating capital needs, and the drawdown of federal COVID-19 relief funds are significant headwinds for several high-profile issuers. This month, S&P Global Ratings downgraded San Francisco’s Bay Area Rapid Transit District from AA to A+. If fare-box revenues continue to stagnate, states and local governments will need to provide alternative revenue sources to bolster these essential infrastructure assets—like the payroll mobility tax rate increase that New York passed in its FY 2024 budget, generating an additional $1.1 billion annually for the Metropolitan Transportation Authority.

Investment involves risk. The two main risks related to fixed-income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of June 6, 2023, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed accurate. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the reader’s sole discretion.

©2023 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© BlackRock

Read more commentaries by BlackRock