The View From Turin

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEditor’s Note: I chaired an international economics conference in Italy earlier this month. Delegates from all over the world attended to discuss the issues of the day. Following is an abridged version of the meeting summary that I offered during the closing session.

Most of us know of Italy through study of the Roman Empire and familiarity with la cucina Italiana. In both aspects, Italy has been a force with global reach and a strong sense of its place in the world.

Between the fall of Rome and the middle of the 19th century, Italy was often a chaotic place. A hodgepodge of kingdoms, duchies, and city-states, the region was deeply fragmented and often at war with itself. Church and state were not always distinct from one another, a multitude of currencies were utilized, and there was no single mother tongue.

Turin is situated in the northwest of the country, but it played a central role in Italian reunification. It served as the first capital when the modern Italian state was formed in 1861. And so Turin offered an excellent backdrop for discussions of developments in trade, politics, economics and finance.

Paying For The Pandemic

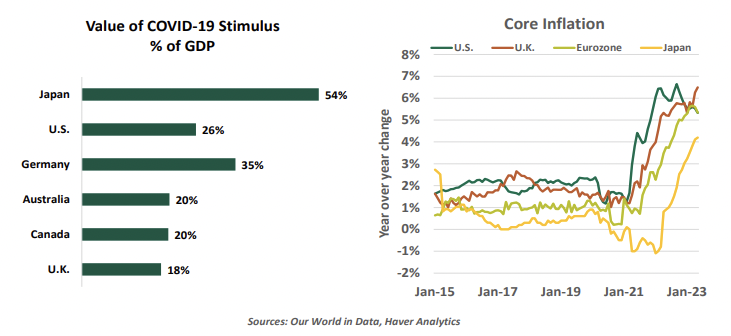

The opening segment of the conference contended that the post-COVID era had left us with three stages of economic after-effects. The most immediate of these is a higher-for-longer interest rate environment.

The root cause of the new interest rate paradigm has been levels of inflation which are the highest in decades. Immense government spending programs, intended to cushion the impacts of the pandemic, were a root cause of this development.

Fiscal policy in much of the world has moved to a much less generous posture. While the debt ceiling in America has been suspended for the coming two years, fights over individual budget bills reflect ongoing concern about the level of Federal borrowing. Rising interest bills are absorbing monies that might better be deployed elsewhere.

At the same time, nations are being challenged to tackle broad initiatives that include energy transition, technological transformation, and international security. Additional public investment in education and infrastructure may be needed to sustain productivity, a key to ongoing growth. The proper size and role of governments in economies continues to be a topic of active debate.

Europe is seeking to refresh the debt and deficit targets that bind users of the common currency. Exogenous shocks have made these objectives much more difficult to achieve, and argue for additional flexibility in the application of updated rules. Age-old differences in economic philosophy between Northern and Southern Europe are reappearing, challenging the achievement of consensus.

Outside of the major markets, fiscal policy during the past three years tended toward one of two extremes. China refrained from stimulating its economy during COVID, partly because the Chinese were reluctant to recognize the damage the virus was doing to commerce and public health. For this reason, China has been the only major world economy not to suffer from a rapidly rising price level. In fact, some are now concerned that China is at risk for deflation.

On the other end of the spectrum are some nations in South America, which have engaged in fiscal recklessness. Hyperinflation has led to political instability in many of those countries, and a few of them may struggle to avoid defaulting on their debts.

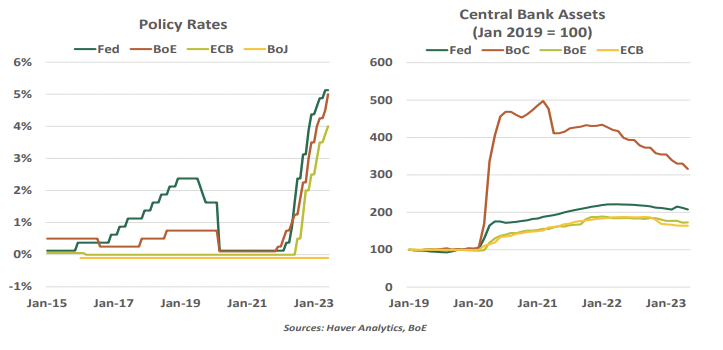

Central banks were equally responsible for the development of inflation. Using their balance sheets to assist with relief, monetary authorities loosed immense amounts of reserves on the financial system. Optimistic expectations of moderation in the price level persisted for too long, delaying corrective action.

Even after the sharpest tightening of monetary policy in 45 years, inflation is still well above acceptable ranges. Conference attendees once again anticipated that inflation has peaked and is on its way back to targeted levels. But as I listened during the week, I concluded that our confidence in forecasting and managing inflation is greatly diminished from its pre-pandemic levels.

Linkages between wages and prices have kept inflation elevated in a number of countries, as have the costs of housing. In some places, the use of indexation to drive wages and retirement benefits has perpetuated and extended price level pressure.

Even if monetary policy brings inflation back under control over the next year or two, long-run structural forces will present a new set of challenges. Decarbonization, deglobalization, and demographics all have the potential to be inflationary if not managed well.

The impact of tighter monetary policy is readily apparent in the banking sector. Regional discussions during the conference all touched on whether central banks are fomenting financial instability. The sensitivity of bank earnings, liquidity, and capital to higher interest rates is supposed to be the subject of careful oversight, but it has become apparent that neither intermediaries nor their supervisors were prepared for what has occurred.

At best, industry performance will be impaired; at worst, there could be additional stress. Outcomes will vary considerably across markets based on the structure of real estate lending, alternatives to bank deposits, and the degree to which central banks will have to go to bring inflation back under firm control. Balance sheets and business models structured to succeed in a lower for longer interest rate environment may find it hard to adapt to the new reality.

Financial stability will continue to complicate the conduct of monetary policy. Macroprudential tools have, once again, been found wanting. And while attempts will be made to rehabilitate them, they may raise costs to the industry without reducing risk.

How high will interest rates go? The answer will depend on an assessment of how tight policy is in each market, and how far inflation is from ideal ranges. We discussed the proper construction of an inflation target, how it might vary between markets, and whether a central bank could ever adjust a target without losing credibility. (The consensus on the latter question was “no.”)

During our regional discussions, the following central bank outlooks were offered:

- The U.S. Federal Reserve once again finds itself behind the curve. Hoping for what one delegate called “immaculate disinflation,” the Fed now finds itself in the awkward position of having to resume tightening after taking a pause. A key determinant of the U.S. policy path will be whether bank lending standards become overly tight: so far, there is little evidence of this.

- The European Central Bank will likely have to raise its deposit rate to 4% or higher to bring inflation back into its targeted range. One of our delegates suggested that the continent is facing a “polycrisis,” formed of slowing growth, banking concerns, energy transition, and continued exposure to war in the east. Divergent performance within the bloc may come to complicate decision-making in Brussels and Frankfurt.

- Central banks in Canada and Australia are also back to tightening after thinking that they were through. “Head fakes” of this kind are uncomfortable for policy makers, and may lead them to be overly conservative in defining the peak level of interest rates.

As policy iterates, it will be critical to keep growth in excess of interest rates, a condition that is key to living standards and debt sustainability. Some countries may have difficulty chinning that bar.

Going Separate Ways

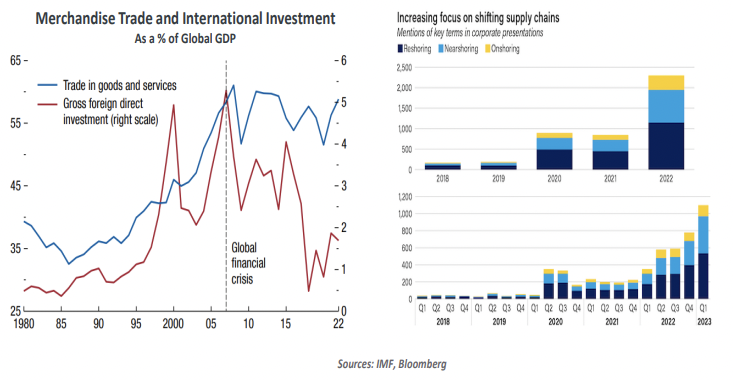

The second post-COVID theme discussed at the conference was the drift away from globalization, a trend which has been furthered by heightened international uncertainty. Geopolitical tension was identified as a leading risk in the group’s annual survey.

The war in Ukraine is the most serious expression of this. Delegates from Eastern Europe reported that there was no endgame in sight for the conflict; the economic costs to the combatants and others will remain steep. The group consensus was that sanctions have not produced the economic consequences for Russia that were forecast in the spring of 2022. Russian support for Vladimir Putin has not diminished, even in the presence of a “post-industrial” population that opposes the war.

Presenters on the topic of global trade made full use of the IMF’s April World Economic Outlook. The publication included a section on fragmentation, which illustrated the decline in international commerce, the rise in protection, the close association between geopolitical risk and interest in reshoring, and the impact to regional and global growth that results from all of the above.

Shocks and failures over the past two decades have ended “The Great Moderation” and turned hyper-globalization into “slow-balization.” Trade fairness has combined with supply insecurity and rising economic rivalry to hinder international commerce.

Some observers refer to this process as the de-risking of supply chains. Given the geopolitical tension created by fragmentation, some in our group asked whether de-risking was a misnomer. Tail risks have multiplied as countries pull away from one another; the bitterness created by a sanctions stalemate will not help Russia and the EU restore trust in one another over time. Further, moving production to domestic suppliers who are not prepared to perform can present a new set of supply chain challenges.

Reinforcing trade ties, as opposed to breaking them, might be the better way to de-risk supply chains. I found this argument convincing, but somehow I suspect that international authorities will be more hesitant to embrace them. Deglobalization will not be easy, and its benefits are unclear. But that does not seem to be deterring countries from pursuing it.

The application of industrial preferences to favor local providers has widened and deepened. Each new round prompts retaliation; the Inflation Reduction Act (which has more to do with promoting U.S. clean tech than it does with containing inflation) is a good example. The World Trade Organization stands powerless to adjudicate disputes.

Barring a reversal of recent restrictions covering international trade, Mexico is among the countries who stands to gain the most. There is considerable overlap in Mexican and Chinese exports to the U.S., which may invite substitution. But Mexican facilities closest to the U.S. border are operating near full capacity, so securing additional market share will require important amounts of investment in facilities and logistics.

Diminished Potential

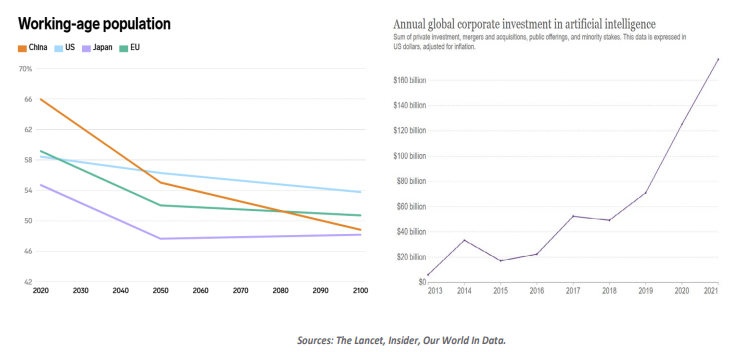

The longest-tailed after-effect of the pandemic is its impact on demographics and productivity. COVID-19 diminished birth rates, life expectancy, immigration and labor force participation, all of which will limit economic achievement in the decades ahead.

There are young populations around the world, but many of them have limited access to education and capital. They may be on the move in the decades to come, much to the chagrin of their intended destinations.

China has one of the world’s deepest demographic deficits. Its population is shrinking, and its labor force is shrinking more rapidly. The consensus estimate of 3% real growth for China in the medium term is much slower than it has sustained in recent decades, but may nonetheless be optimistic unless productivity growth reaches lofty new levels.

Overcoming the weight of aging population will require the application of advanced technology that improves productivity. The group shared perspectives on digitalization, outlining the many hurdles to the achievement of its full promise. This included a tour of the AI landscape, which illustrated its promise and its perils.

The group’s list of worries remains long, and the tone of the conference reflected those concerns. But in one sense, the inaccuracy of our consensus last year provides some comfort: we vastly underestimated the resilience of the world’s economies when we gathered in 2022. Perhaps we will be similarly surprised when we reconvene in Canada twelve months from now.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Carl R. Tannenbaum

Executive Vice President and Chief Economist

Carl Tannenbaum is the Chief Economist for Northern Trust. In this role, he briefs clients and colleagues on the economy and business conditions, prepares the bank's official economic outlook and participates in forecast surveys. He is a member of Northern Trust's investment policy committee, its capital committee, and its asset/liability management committee.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All