Income-driven repayment will ease the burden of resuming student loan payments.

Last week, the Supreme Court blocked the Biden Administration’s program of student debt relief. We are not legal scholars, and cannot comment on the merits of the case. We can say that it will have an important economic impact.

We’ve discussed America’s problem with educational debt several times (notably here, here, and here). The sheer size of the borrowing represents a significant burden to both students and society. About one-quarter of young people who start college don’t finish, leaving them with debt but no degree. Others struggle to keep up with their payments, with consequences for access to credit, labor markets, family formation, and housing, among other things.

Forgiving debts may leave those who kept up with their obligations feeling aggrieved, and so it is not a step to be taken lightly. But debts are often forgiven in discussions between borrowers and lenders, and they are routinely expunged during bankruptcy. (Student loans are an exception to this latter practice; debtors typically have to take additional steps to get them reduced.) So there is precedent for relief.

The Biden plan had a series of design flaws. It used blunt income thresholds to determine the degree of forbearance, as opposed to basing relief on financial hardship. It did not address the root causes of the problem, which include outsized increases in tuition, the lack of performance-based criteria for qualifying colleges, and appropriate steering/screening for students before they borrow.

But 26 million Americans had either applied for or been pre-approved for relief prior to the court’s decision. Along with other borrowers, they will soon have to resume payments after a three-and-a-half-year hiatus. The average monthly bill is around $380, enough to force spending reallocations for many households, especially those earning more modestly. This will create a drag on consumption.

The administration is hoping to replace the stricken program with one featuring income-driven repayment (IDR). At present, student debtors have to prove hardship to scale their payments to their earnings; proposed revisions to the IDR system would make this the default. After some period of time under an IDR, the remaining balance of loans would be forgiven. A number of other countries, including England and Australia, use this approach.

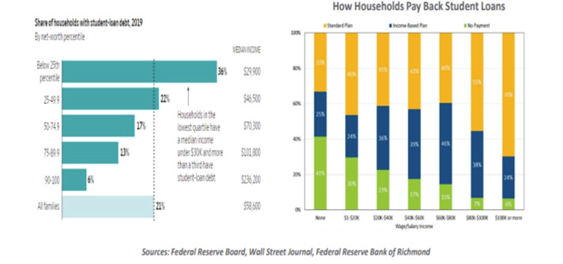

A study from the Federal Reserve Bank of Richmond found that more than one-quarter of borrowers and almost one-half of student loan balances have transitioned to income-based payment arrangements. The revised proposal would merely ratify and extend what is already in place. Timing will be an issue: initial drafts of the IDR have been criticized as overly complicated, which will make implementation challenging. It could be a number of months before relief reaches its intended destination.

IDR systems encourage investment in human capital and prevent student debt from becoming overly burdensome. But they do not create direct pressure on providers to hold down the costs of education or improve access to and understanding of student loan programs by collegians. A broader solution is still needed.

Prospects of achieving one are not bright, given the partisanship of today’s politics. To work around gridlock in a number of areas, recent administrations have increasingly employed rulemaking interpretations to implement programs when legislative routes are blocked.

These interpretations are often subject to legal challenges. This ultimately places courts, not Congress, at the center of policy debates.

The debt incurred to acquire education in the United States is far too large and presents risks to individuals and to the economy. The status quo cannot be sustained. But lasting reform of the federal student loan system (among other programs) must come from the government, not the judiciary. With that, we rest our case.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our white papers.

© Northern Trust

Read more commentaries by Northern Trust