Japan may uniquely benefit from a wage-price spiral.

I enjoy opera, but I struggle with the language. I know some French and Italian, but it is hard to make out words and phrases when they are being sung at 100 decibels.

That is one of the reasons that my favorite operatic work is Gilbert and Sullivan’s The Mikado. Sung in English, it is a spoof of British politics set in imperial Japan. A 1983 production of the work replaced the royal court with an automobile company, and the emperor entered a shiny new Datsun. It seemed fitting: at the time, Japan and its industries were on top of the world.

As the 1980s came to a close, Japan suffered a serious fall. Thirty years of economic stagnation ensued. Today, however, prospects for Japan are looking brighter than they have in a long time.

Numbers only begin to describe Japan’s fall from grace. Its main stock market index, the Nikkei 225, remains 15% below the peak it reached at the end of 1989. Japan’s real gross domestic product (GDP) has grown at an annual pace of just 0.8% since then. The Bank of Japan (BoJ) has done so much to stimulate growth that its balance sheet is larger than Japan’s national income.

Beyond that, Japan is an aged (not aging) country that has acquired a reputation as a poor source of innovation. China rose to become a formidable competitor; its GDP surpassed Japan’s in 2010. Japan’s late prime minister Shinzo Abe attempted to breathe life into the economy with his “three arrows” program (monetary, fiscal and structural reforms) but had only limited success.

The pandemic was particularly hard on Japan, as it found itself snarled in supply chain tangles and limited by the lockdown. The 2020 Tokyo Olympics were expected to provide a much-needed economic boost, but COVID-19 forced a postponement and severe restrictions on spectators.

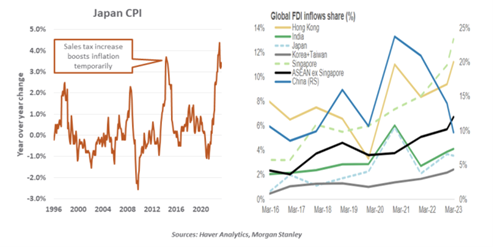

But it appears that the Land of the Rising Sun is on the rise again. Japan is likely to register the best growth of any developed economy this year, and the Nikkei 225 is up by 24% so far in 2023. The price level is rising persistently, but modestly, and the BoJ is seriously considering reducing monetary accommodation.

Strange though it may sound, the pandemic may have provided the impetus for Japan’s recovery. Japanese consumers are frugal, and its companies have traditionally lacked pricing power, both contributing to decades of near-zero inflation. But shortages of goods in 2020 and 2021 broke this cycle. Higher prices and diminished labor supply prompted workers to ask for better wage increases, a process that the government supported. In a sense, Japanese authorities engineered a miniature wage-price spiral to cure the country of deflation.

The desire of companies and countries for more secure supply chains in the wake of COVID-19 has favored Japan. To accommodate increased demand amid a very tight labor market, Japanese firms have increased their rate of capital expenditure. Foreign direct investment into Japan is rising nicely, while China’s share is shrinking. These investments will pay dividends in the form of higher growth in the coming years.

Despite the improvement in Japan’s outlook, its currency has been on the defensive. After nearing 100 versus the dollar at the beginning of 2021, the yen has lost traction, averaging 141 in June of this year. The differential between Japanese interest rates and those in other countries has been the driving factor. The weak yen has, however, been helpful in improving Japan’s terms of trade.

Given the hardships and head-fakes of the last three decades, Japanese authorities are reluctant to declare victory. The country still relies very heavily on exports; slow growth in other developed markets will limit demand for Japanese products. Demographics are a headwind; while Japan is welcoming more immigrants, better population growth will be critical to sustained economic growth. And Japan’s ability to benefit from re-shoring will be limited by the high cost of doing business there and its distance from the United States.

Still, the tone surrounding Japan’s economy is improving. And that is music to many ears.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust