Applying Our Playbook to EM

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits- We favor emerging market (EM) to developed market (DM) assets on a brighter macro backdrop. We get granular and harness mega forces, per our playbook.

- U.S. bond yields slumped last week on softer CPI inflation data. We think still tight labor markets will compel the Federal Reserve to hold policy tight.

- We look to this week’s U.S. data for more signs higher policy rates are cooling production and spending. We see policy staying tight even as activity weakens.

We tapped into what proved a stealth rally in EM stocks and bonds, along with the DM stock gains this year. We still think EM assets have an edge over developed market (DM) peers in the first layer of our new playbook, the macro assessment. Inflation is cooling enough in key EMs to allow policy rate cuts. We get granular in our playbook’s second layer to find countries and sectors we like. Our third layer harnesses mega forces to capture structural shifts within EMs.

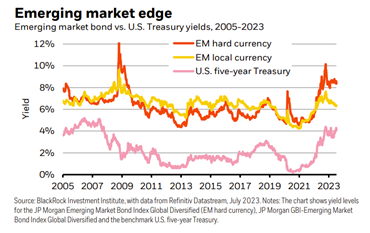

We’ve preferred EM debt to DM long-term peers for some time. We went tactically overweight EM local currency debt in March, picking up higher yields for carry and benefiting from a broadly weaker U.S. dollar plus tightening spreads this year (yellow line in chart). Higher EM yields remain attractive but tightening spreads with Treasuries (pink line) lead us to consider switching to hard currency peers typically issued in U.S. dollars (orange line). But peaking DM policy rates should support EM currencies, bolstering EM local debt for now. DM rate hikes have hit EM hard in the past, but we think they’re in a different spot now thanks to improved external balance sheets. We think that’s why we’re not seeing the EM asset volatility as in the 2013 taper tantrum. The Fed’s plan to taper bond purchases then sparked sharp EM capital outflows and currency depreciation. It’s the opposite now: capital inflows and stronger currencies are boosting returns in EM local currency bonds.

A brighter EM macro and policy picture may also be underappreciated, in our view. DM central banks inching toward the end of rapid hikes is good for EMs – but a key difference is we think EM peers are closer to rate cuts as inflation falls. EM central banks were well ahead of DM peers in hiking – and some have hiked much more to bring inflation down quickly. Take Brazil: Policy rates have risen to just under 14% from 2% in 2021. When it comes to EM investing this year, much focus has been on China’s economy losing steam. But outside China, EM equities have staged a stealth rally with double-digit gains across Latin America and other parts of Asia. We see more upside there and more attractive valuations relative to DM economies as the policy picture and EM economic growth prospects improve, even as China’s restart sputters. That’s the first layer of our new playbook in action: our macro takes in the context of what’s in the price.

The second layer of our new playbook is about getting granular. We go beyond broad EM exposures to find the brightest macro backdrops across countries and the most attractive valuations under the surface. Within EM local currency bonds, we like Mexico for its quality tilt and Brazil for its exceptional carry from still-high bond yields. Our playbook also calls for being nimble. EM is not disconnected from global growth, so we are constantly watching for how that may affect the EM backdrop.

We also get granular in sectors and regions and use the third layer of our playbook – harnessing mega forces – to capture returns now and in the future. We see five big structural forces transcending the macro backdrop: digital disruption and artificial intelligence (AI), geopolitical fragmentation, the low-carbon transition, aging populations, and the future of finance. We see abundant EM equity opportunities through these mega forces – what matters is what markets have priced. The semiconductor industry is powering AI and is a key part of the EM technology sector. A rapidly growing population in India sets the country apart from DMs. India's system of digital payments also bodes well for the future of finance there, we believe: It could pave the way for a credit boom as banks adapt lending. We think the low-carbon transition presents an important opportunity for Latin America, especially for countries that hold large reserves of key resources like copper and lithium. The rewiring of supply chains due to global fragmentation could also have significant implications for countries like Mexico that could benefit if U.S. companies bring operations and production closer to home.

Bottom line: Our new playbook leads us to favor EM over DM assets. We see a brighter policy outlook as some EMs stand ready to cut policy rates. We get granular in EM debt across countries and in EM equities by harnessing mega forces.

Market Backdrop

U.S. bond yields dropped, and stocks climbed to 15-month highs last week as markets eyed an end in sight to the Fed’s rapid hiking cycle after the softer-than-expected June CPI data. Both two- and 10-year Treasury yields posted their sharpest weekly declines since the March banking turmoil. The labor market is key for what lies ahead for inflation. We see still-strong wage growth keeping core inflation elevated, compelling the Federal Reserve to hold policy tight.

Macro Takes

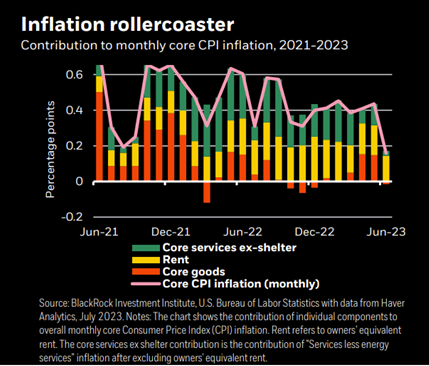

The U.S. core CPI inflation for June came in at 0.2% month-on-month, down from 0.4% in May and below expectations.

One element of that was unsurprising: the drag from goods prices. See the chart. We expected goods prices to fall as consumer spending normalized following a surge in goods consumption during the pandemic. Some of that started in the second half of last year (see the orange bars in the chart) and it recurred in June, driven by a decline in used car prices. We see more goods deflation ahead, reinforcing our view that overall inflation will be on something of a rollercoaster in the coming months.

The real surprise was that core services inflation excluding housing was flat on the month. We think this could be a one-off and unlikely to happen again this year: It’s difficult to see how core services inflation can be so low with wage growth remaining strong. We still think core inflation is proving persistent at levels well above the Fed’s 2% target. And that’s why we think the Fed will still hike rates later this month.

Investment themes

1 Holding tight

- Markets have come around to the view that central banks will not quickly ease policy in a world shaped by supply constraints – notably worker shortages in the U.S.

- We see central banks being forced to keep policy tight to lean against inflationary pressures. This is not a friendly backdrop for broad asset class returns, marking a break from the four decades of steady growth and inflation known as the Great Moderation

- Economic relationships investors have relied upon could break down in the new regime. The shrinking supply of workers in several major economies due to aging means a low unemployment rate is no longer a sign of the cyclical health of the economy. Broad worker shortages could create incentives for companies to hold onto workers, even if sales decline, for fear of not being able to hire them back. This poses the unusual possibility of “full employment recessions” in the U.S. and Europe. That could take a bigger toll on corporate profit margins than in the past as companies maintain employment, creating a tough outlook for DM equities.

- Investment implication: Income is back. That motivates our overweight to short-dated U.S. Treasuries.

2 Pivoting to new opportunities

- Greater volatility has brought more divergent security performance relative to the broader market. Benefiting from this requires getting more granular and eyeing opportunities on horizons shorter than our tactical ones. We go granular by tilting portfolios to areas where we think our macro view is priced.

- We think dispersion within and across asset classes – or the extent to which prices deviate from an index – will be higher in the new regime amid the various crosscurrents at play, allowing for granularity. That offers more ways to build portfolio “breadth” via uncorrelated exposures, in our view.

- We think it also means security selection, expertise, and skill are even more important to achieving above-benchmark returns. Relative value opportunities from potential market mispricing are also likely to be more abundant.

- Investment implication: We like quality in both equities and fixed income.

3 Harnessing mega forces

- Mega forces are structural changes we think are poised to create big shifts in profitability across economies and sectors. These mega forces are digital disruption like artificial intelligence (AI), the rewiring of globalization driven by geopolitics, the transition to a low-carbon economy, aging populations, and a fast-evolving financial system.

- The mega forces are not in the far future – but are playing out today. The key is to identify the catalysts that can supercharge them and the likely beneficiaries – and whether all of this is priced in today. We think granularity is key to finding the sectors and companies set to benefit from mega forces.

- We think markets are still assessing the potential effects as AI applications could disrupt entire industries.

- Geopolitical fragmentation, like the strategic competition between the U.S. and China, is set to rewire global supply chains, we think.

- The low-carbon transition caused economies to decarbonize at varying speeds due to policy, tech innovation, and shifting consumer and investor preferences. Markets have historically been slow to fully price in such shifts.

- We see profound changes in the financial system. Higher rates are accelerating changes in the role of banks and credit providers, shaping the future of finance.

- Investment implication: We are overweight AI as a multi-country, multi-sector investment cycle unfolds.

BlackRock Investment Institute

The BlackRock Investment Institute (BII) leverages the firm’s expertise and generates proprietary research to provide insights on macroeconomics, sustainable investing, geopolitics, and portfolio construction to help Blackrock’s portfolio managers and clients navigate financial markets. BII offers strategic and tactical market views, publications, and digital tools that are underpinned by proprietary research.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation, or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This material may contain estimates and forward-looking statements, which may include forecasts and do not represent a guarantee of future performance. This information is not intended to be complete or exhaustive and no representations or warranties, either express or implied, are made regarding the accuracy or completeness of the information contained herein. The opinions expressed are as of July 17, 2023, and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

In the U.S. and Canada, this material is intended for public distribution. In the European Economic Area (EEA): This is issued by BlackRock (Netherlands) B.V. and is authorized and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded. In the UK and Non-European Economic Area (EEA) countries: this is Issued by BlackRock Advisors (UK) Limited, which is authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL, Tel: +44 (0)20 7743 3000. Registered in England and Wales No. 00796793. For your protection, calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorized activities conducted by BlackRock. In Italy, for information on investor rights and how to raise complaints please go to https://www.blackrock.com/corporate/compliance/investor-right available in Italian. For qualified investors in Switzerland: This document is marketing material. This document shall be exclusively made available to, and directed at, qualified investors as defined in Article 10 (3) of the CISA of 23 June 2006, as amended, at the exclusion of qualified investors with an opting-out pursuant to Art. 5 (1) of the Swiss Federal Act on Financial Services ("FinSA"). For information on Art. 8 / 9 Financial Services Act (FinSA) and on your client segmentation under Art. 4 FinSA, please see the following website: www.blackrock.com/finsa. For investors in Israel: BlackRock Investment Management (UK) Limited is not licensed under Israel’s Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder. In South Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorized financial services provider with the South African Financial Services Board, FSP No. 43288. In the DIFC this material can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is regulated by the Dubai Financial Services Authority (DFSA). This material is only directed at 'Professional Clients’ and no other person should rely upon the information contained within it. Blackrock Advisors (UK) Limited - Dubai Branch is a DIFC Foreign Recognised Company registered with the DIFC Registrar of Companies (DIFC Registered Number 546), with its office at Unit 06/07, Level 1, Al Fattan Currency House, DIFC, PO Box 506661, Dubai, UAE, and is regulated by the DFSA to engage in the regulated activities of ‘Advising on Financial Products’ and ‘Arranging Deals in Investments’ in or from the DIFC, both of which are limited to units in a collective investment fund (DFSA Reference Number F000738)In the Kingdom of Saudi Arabia, issued in the Kingdom of Saudi Arabia (KSA) by BlackRock Saudi Arabia (BSA), authorized and regulated by the Capital Market Authority (CMA), License No. 18-192-30. Registered under the laws of KSA. Registered office: 29th floor, Olaya Towers – Tower B, 3074 Prince Mohammed bin Abdulaziz St., Olaya District, Riyadh 12213 – 8022, KSA, Tel: +966 11 838 3600. The information contained within is intended strictly for Sophisticated Investors as defined in the CMA Implementing Regulations. Neither the CMA nor any other authority or regulator located in KSA has approved this information. The information contained within does not constitute and should not be construed as an offer of, invitation, or proposal to make an offer for, the recommendation to apply for, or an opinion or guidance on a financial product, service, and/or strategy. Any distribution, by whatever means, of the information within and related material to persons other than those referred to above is strictly prohibited. In the United Arab Emiratesis only intended for - natural Qualified Investors as defined by the Securities and Commodities Authority (SCA) Chairman Decision No. 3/R.M. of 2017 concerning Promoting and Introducing Regulations. Neither the DFSA nor any other authority or regulator located in the GCC or MENA region has approved this information. In the State of Kuwait, those who meet the description of a Professional Client as defined under the Kuwait Capital Markets Law and its Executive Bylaws. In the Sultanate of Oman, sophisticated institutions that have experience in investing in local and international securities, are financially solvent and have knowledge of the risks associated with investing in securities. In Qatar, for distribution with pre-selected institutional investors or high net worth investors. In the Kingdom of Bahrain, to Central Bank of Bahrain (CBB) Category 1 or Category 2 licensed investment firms, CBB licensed banks, or those who would meet the description of an Expert Investor or Accredited Investors as defined in the CBB Rulebook. The information contained in this document does not constitute and should not be construed as an offer of, invitation, inducement, or proposal to make an offer for, the recommendation to apply for, or an opinion or guidance on a financial product, service, and/or strategy. In Singapore, this is issued by BlackRock (Singapore) Limited (Co. registration no. 200010143N). This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. In Hong Kong, this material is issued by BlackRock Asset Management North Asia Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong. In South Korea, this material is for distribution to Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations). In Taiwan, independently operated by BlackRock Investment Management (Taiwan) Limited. Address: 28F., No. 100, Songren Rd., Xinyi Dist., Taipei City 110, Taiwan. Tel: (02)23261600. In Japan, this is issued by BlackRock Japan. Co., Ltd. (Financial Instruments Business Operator: The Kanto Regional Financial Bureau. License No375, Association Memberships: Japan Investment Advisers Association, the Investment Trusts Association, Japan, Japan Securities Dealers Association, Type II Financial Instruments Firms Association.) For Professional Investors only (Professional Investor is defined in Financial Instruments and Exchange Act). In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not take into account your individual objectives, financial situation needs, or circumstances. In China, this material may not be distributed to individual residents in the People’s Republic of China (“PRC”, for such purposes, excluding Hong Kong, Macau, and Taiwan) or entities registered in the PRC unless such parties have received all the required PRC government approvals to participate in any investment or receive any investment advisory or investment management services. For Other APAC Countries, this material is issued for Institutional Investors only (or professional/sophisticated /qualified investors, as such a term may apply in local jurisdictions). In Latin America, no securities regulator within Latin America has confirmed the accuracy of any information contained herein. The provision of investment management and investment advisory services is a regulated activity in Mexico and thus is subject to strict rules. For more information on the Investment Advisory Services offered by BlackRock Mexico please refer to the Investment Services Guide available at www.blackrock.com/mx

©2023 BlackRock, Inc. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits