China's re-opening surge did not last.

In May, I returned home from my trip to Asia concerned that China’s post-pandemic economy would be weaker than expected. Developments since then suggest that the outlook may have been overly optimistic.

Second-quarter growth in China’s gross domestic product (GDP) fell below 1%, after exceeding 2% in the first quarter. Producer prices in China have dropped by more than 5% over the last year, and consumer prices are flat over that interval. China has seen increasing unemployment, especially among recent university graduates.

China’s manufacturing sector is contracting, with exports limited by slowing growth among its major trading partners. Efforts by countries and companies to reduce their reliance on China (re-shoring or de-risking) are continuing, and efforts by the U.S. government to restrict technology transfer are hindering China’s plans to become a global leader in that space.

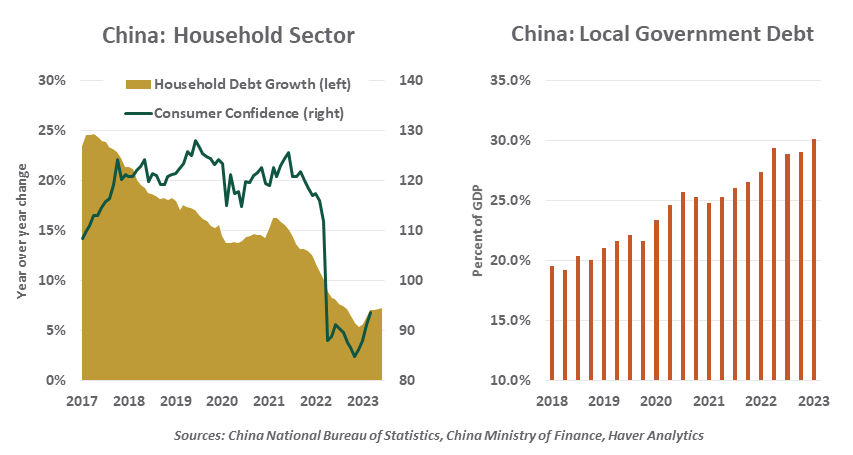

With COVID-19 no longer a significant threat, households were expected to increase their spending through the spring and summer. But consumer confidence and consumption have diminished, despite the lifting of pandemic-era restrictions. Many families are over-indebted, with real estate borrowing a main contributor. As China’s property markets correct, households are deleveraging.

China has been engineering reductions in corporate debt for some time. State-owned enterprises have been a particular focus of this effort. As well, Beijing has been trying to bring national government debt under better control. When the major sectors of an economy are all moving to reduce borrowing, economic activity slows. This is known as a “balance sheet recession.”

There is one exception to China’s drive to de-lever. Local and regional governments in China have been going ever more deeply into debt and may experience challenges servicing it. The practice of borrowing to purchase land for development has passed its peak, and slowing economic growth has reduced tax receipts in some parts of the country. Costs related to the pandemic also burdened regional budgets.

Regional banks are important providers of local government debt, so any provincial duress could cascade through the financial system. No defaults have occurred yet, but a substantial amount of borrowing comes due in the next two years. Capital will be used to plug holes in the balance sheets of regional governments, not for more promising investment opportunities.

Beijing has taken a series of steps to bring more transparency and discipline to the finances of local governments, but more is needed. These efforts will help financial stability, but they will be a further headwind to growth. For now, banks are being encouraged to extend maturities on loans to regional governments, at manageable interest rates. But policymakers are continuing work on structural reforms aimed at reducing this source of systemic risk.

China must now decide what to do about its spreading economic malaise. Credit conditions have been eased in several steps this year but to little apparent effect. Making borrowing more attractive has limited benefits for an economy that is engaged in balance sheet repair.

Some short-term fiscal support is likely, but Chinese authorities prefer to remain focused on the long term. They have signaled a willingness to accept more modest rates of growth, but that could have consequences for employment and investment. A meeting of the politburo later this month is expected to produce specific strategies.

China’s reopening was expected to provide economic momentum as the post-pandemic surge in Western countries faded. But instead of providing a boost to global growth, China presently needs a boost of its own.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust