The economy and markets that have emerged from the pandemic fundamentally changed. For equity investors, we believe this means a different opportunity set than the one that prevailed over the past decade and a half ― and one that favors alpha (excess return) over beta (market return).

Key takeaways

- The era of easy money is ended. The post-pandemic era is setting up to be more volatile with greater differentiation across individual stocks.

- Beta, or market return, is sufficient when a rising tide lifts all boats. In the more traditional investing landscape now forming, we see alpha at the center.

- A more discerning market that prices stocks on their underlying fundamentals is an opportunity for skilled stock pickers to outperform.

It’s not 2019 anymore … or any of the 10 years that preceded it. The pandemic period, inclusive of the crisis response and aftermath, roused an entirely new set of circumstances upon which the economy and markets are just now establishing their footing. For equity investors, we believe this burgeoning regime change means a different opportunity set than the one that prevailed over the past decade and a half ― and one that favors alpha (excess return) over beta (market return).

"We see stock selection becoming more important as individual companies adapt to a higher-inflation, higher-rate world with varying degrees of dynamism and success."

The end ― and beginning ― of an era

Capturing the essence of the market regime now in formation requires context and reflection on the dynamics that existed prior to the current moment. The years following the 2008 Global Financial Crisis (GFC) were marked by 1) fragility and 2) accommodation. Households and businesses were recovering from a deep recession and fallout from financial and corporate failures. For its part, the Federal Reserve (Fed) cut rates to stimulate the economy and help consumers and businesses heal, propping up markets in the process.

Fast forward to 2020 and the COVID-19 crisis, a time marked by a global economic shutdown and restart and an unprecedented infusion of monetary and fiscal support that was far greater than that seen during the GFC even as the earlier crisis imposed a more potent shock to GDP. Consumer pockets were padded with stimulus money and demand for goods was great ― but supply was limited, having been disrupted by pandemic-related closures.

Today, economies are bearing the burden of supply-side inflation ignited by the crisis, accommodated by fiscal and monetary stimulus, and exacerbated by the war in Ukraine. Central banks are now vigilantly raising rates to combat soaring prices. Sticky elements of inflation, such as wages, will be harder to bring down, setting the stage for higher inflation and interest rates for longer, just as stock valuations also are higher.

Investment implications: An alpha imperative

We believe the post-pandemic investment regime characterized by higher inflation, rates and valuations will require a new approach to equity investing. One implication of this new backdrop is lower market return, or beta, suggesting that a higher portion of equity portfolio returns will need to come from alpha or excess return.

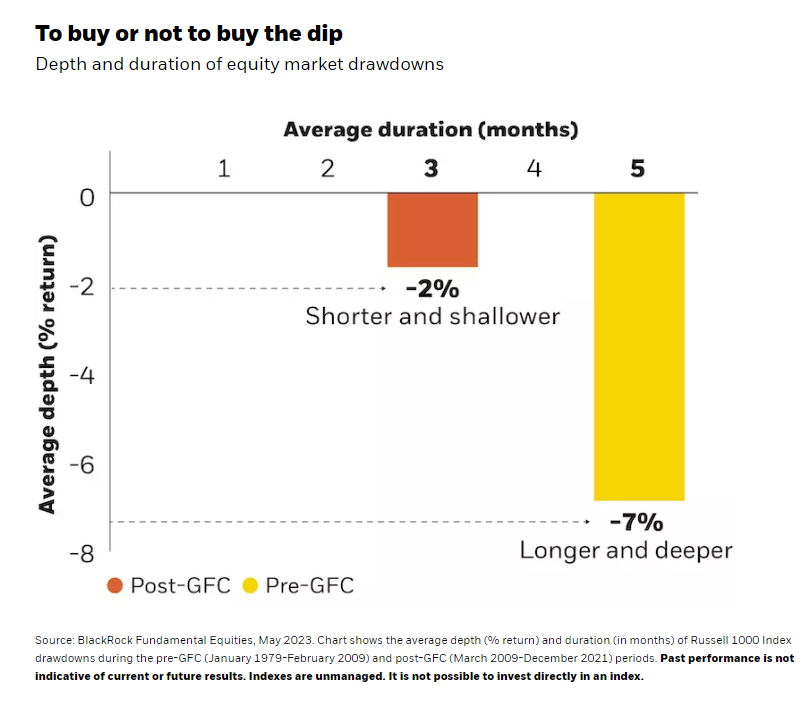

For the 12 years following the GFC, the beta was abnormally high as valuations moved from very low to normal, and the differentiation in returns between individual stocks was slim. Investors bought the dips and, as a result, the drawdowns were quite short and shallow. The Fed also was willing to come to the rescue in the case of any wobbles. Beta was king, as well-supported markets provided extreme performance, resulting in an average annual S&P 500 return of 15% over calendar years 2010 to 2021.

In contrast, the era before the GFC featured longer and deeper equity market drawdowns, as shown below, meaning more volatility as well as greater opportunity for skilled stock picking to deliver above-market returns (or alpha). We see this dynamic returning and the outlook for alpha turning more positive.

Five factors favoring stock picking

While there are no crystal balls in investing and markets are notoriously unpredictable, we see various market dynamics taking shape that support the case for an alpha-centric approach to equity investing:

- Equity market volatility is more likely to increase than decrease.

- Stock dispersion normalizes from narrow levels, separating winners from losers.

- Stock specifics (vs. factors) have a greater influence on return dispersion.

- Currently, the narrow market breadth is poised to widen.

- Artificial intelligence driving opportunity and disruption.

We dig into each of these in the full report.

The return of differentiated returns

In the regime now forming ― the post-pandemic era ― stock valuations, inflation and interest rates are all higher. Supply is being constrained by demographic trends (aging populations and fewer workers), decarbonization and deglobalization, all of which are inflationary as companies spend to adapt. Going forward, the Fed is more likely to be in a position of having to fight inflation rather than bolster the economy, a less friendly scenario for financial markets.

Equities historically have been the highest-returning asset class over the long term, and we see nothing to alter that precedent. However, higher stock valuations than at the start of the prior regime plus higher interest rates mean less return from markets broadly (beta). We see more dispersion in earnings estimates, valuations and stock returns ― and this suggests a greater opportunity for skilled active managers to generate more alpha. The result, in our view, is that the years ahead will see active return being a bigger part of investors’ overall return profiles.

Investing involves risk, including possible loss of principal. Stock values fluctuate in price so the value of your investment can go down depending on market conditions.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of July 2023 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

You should consider the investment objectives, risks, charges and expenses of any BlackRock mutual fund carefully before investing. The prospectus and, if available, the summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or from your financial professional. The prospectus should be read carefully before investing.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

Read more commentaries by BlackRock