“Bullish measures are getting really bullish.”

This is an interesting statement, given how “bearish” sentiment was in 2022. As I noted then:

“Investor sentiment has become so bearish that it’s bullish.

One of the hardest things to do is go “against” the prevailing bias regarding investing. Such is known as contrarian investing. One of the most famous contrarian investors is Howard Marks, who once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, particularly when momentum invariably makes pro-cyclical actions look correct for a while.

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

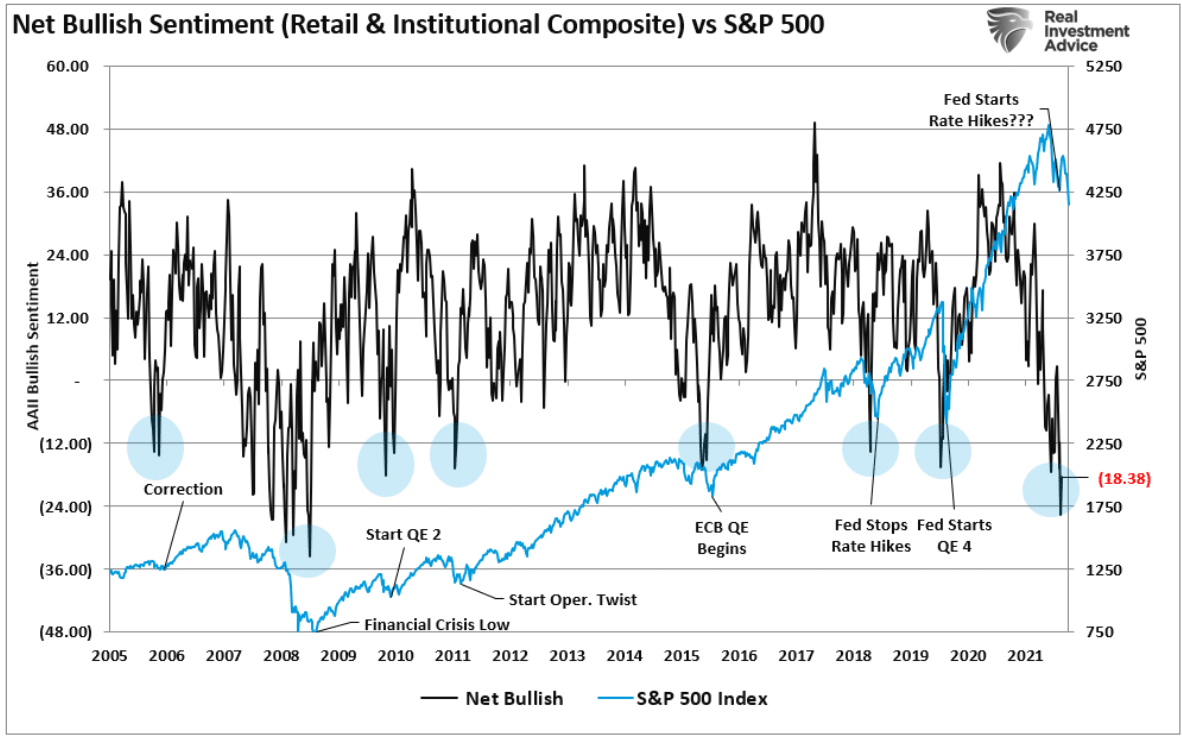

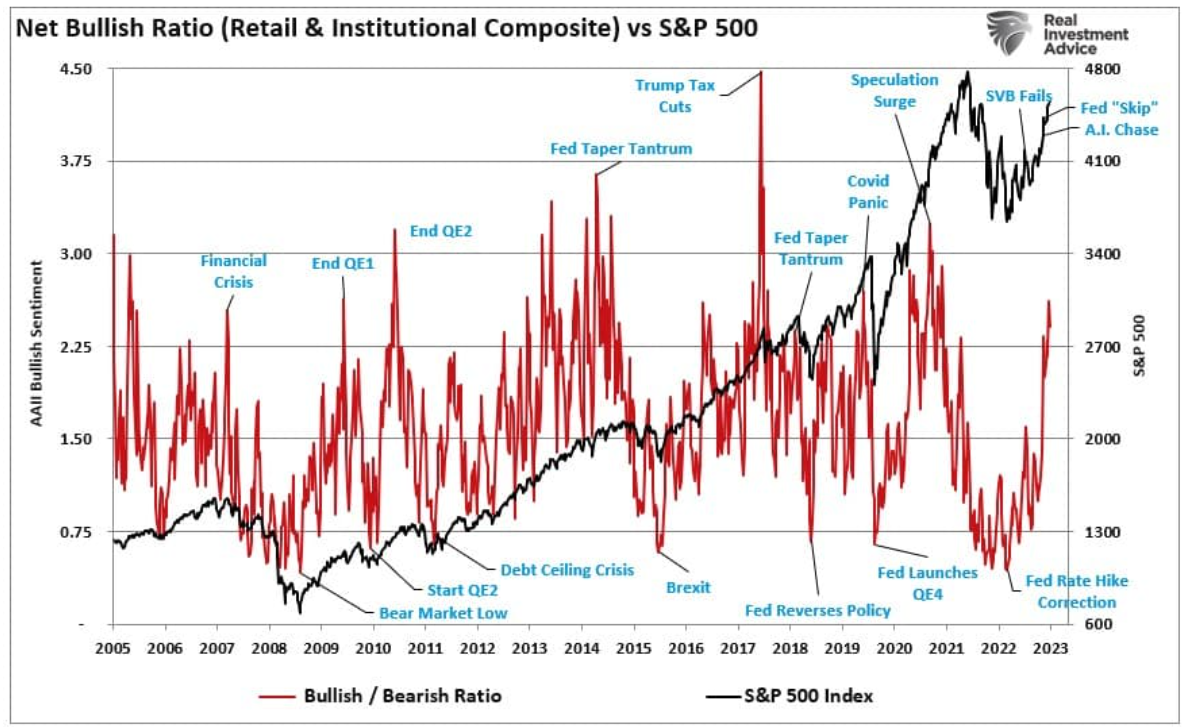

Here is that article’s composite index of retail and professional investor sentiment to visualize just how negative sentiment was then. You will note that sentiment was pushing levels of bearishness not seen since the 2008 “Financial Crisis.”

When levels of negativity reach very low levels, such historically equates to short- to intermediate-term market bottoms. Such is because excesses get built with everyone on the same side of the trade. At that time, everyone was so bearish it was a bullish measure. As we stated then, “the reflexive trade will be rapid when the shift in sentiment occurs.”

Looking back, it is pretty evident such was the case, particularly with the Nasdaq believed to be dead.

Bullish Measures Are Getting Bearish

Of course, hindsight is always 20/20. Last year there were many reasons to be bearish. Things were seemingly so bad, with everyone expecting a recession, that there was nowhere to go but up. Since October, market participants have been betting on avoiding a recession. Such has led to a sharp reversal in bearish sentiment as the “Fear Of Missing Out,” or FOMO, kicked in.

Since the end of January, despite the Fed hiking rates, a bank solvency crisis, and weakening economic data, the market has continued to “climb a wall of worry.” In fact, not only did it climb a wall of worry.

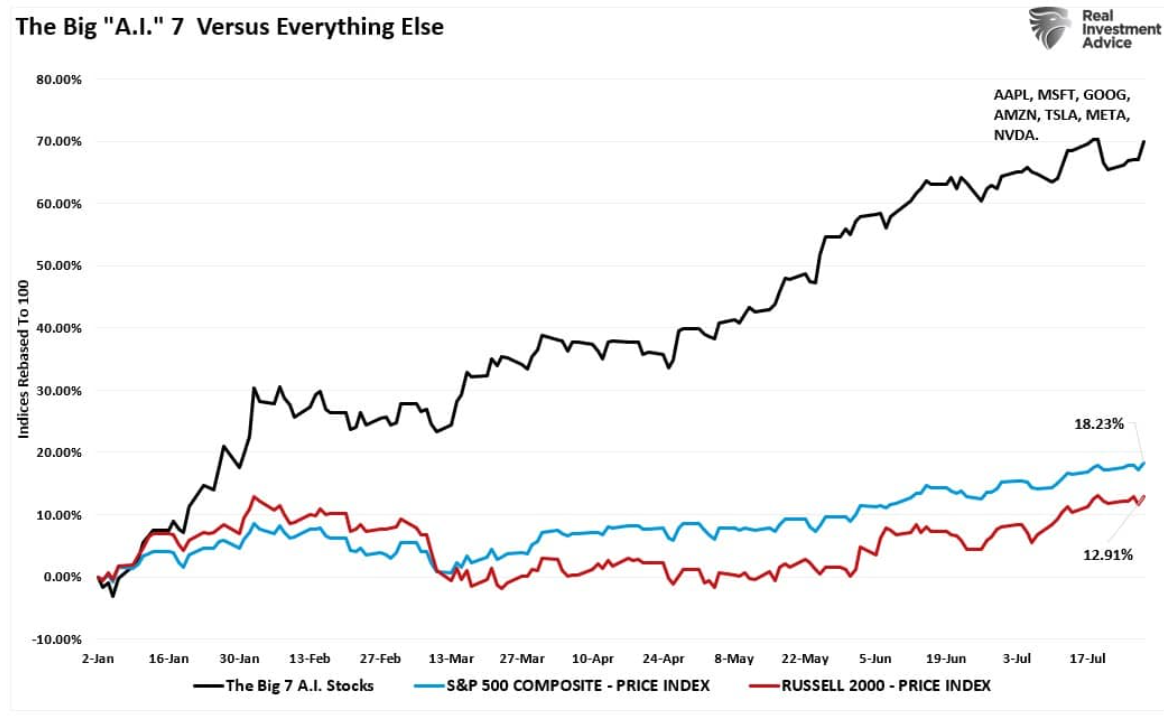

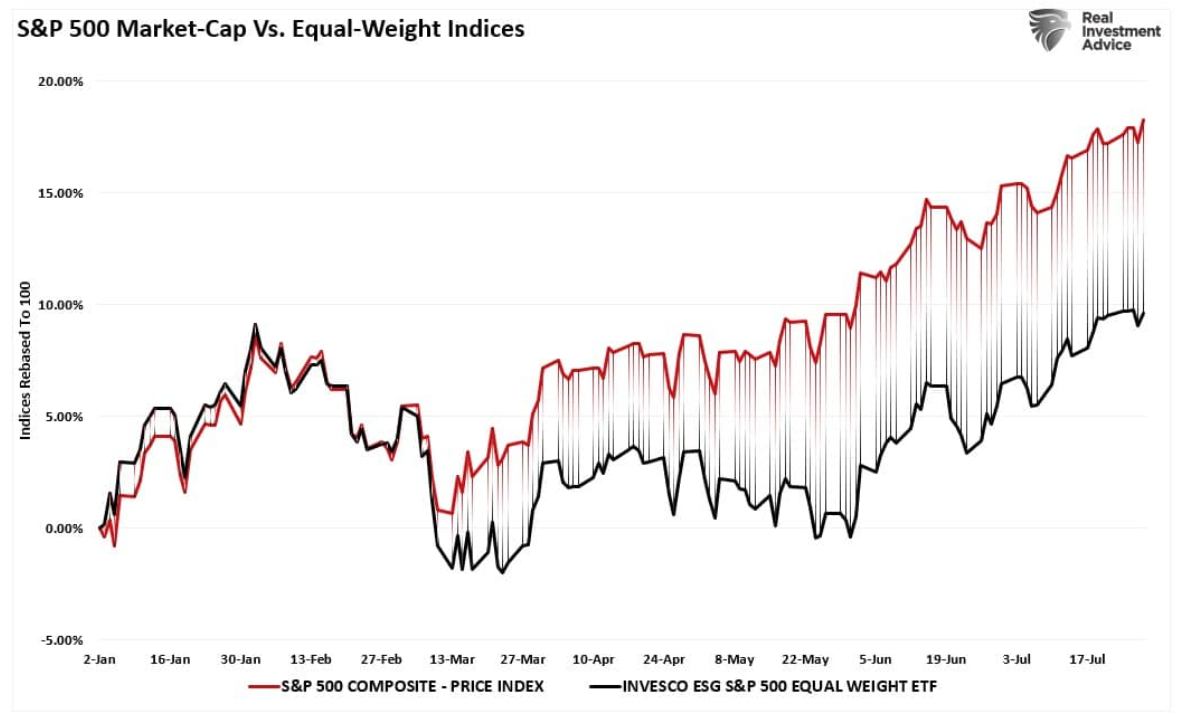

As discussed in “Breadth Not As Strong As A/D Suggests,” if it weren’t for the 7-largest market capitalization-weighted stocks in the S&P 500, market returns this year would be substantially lower.

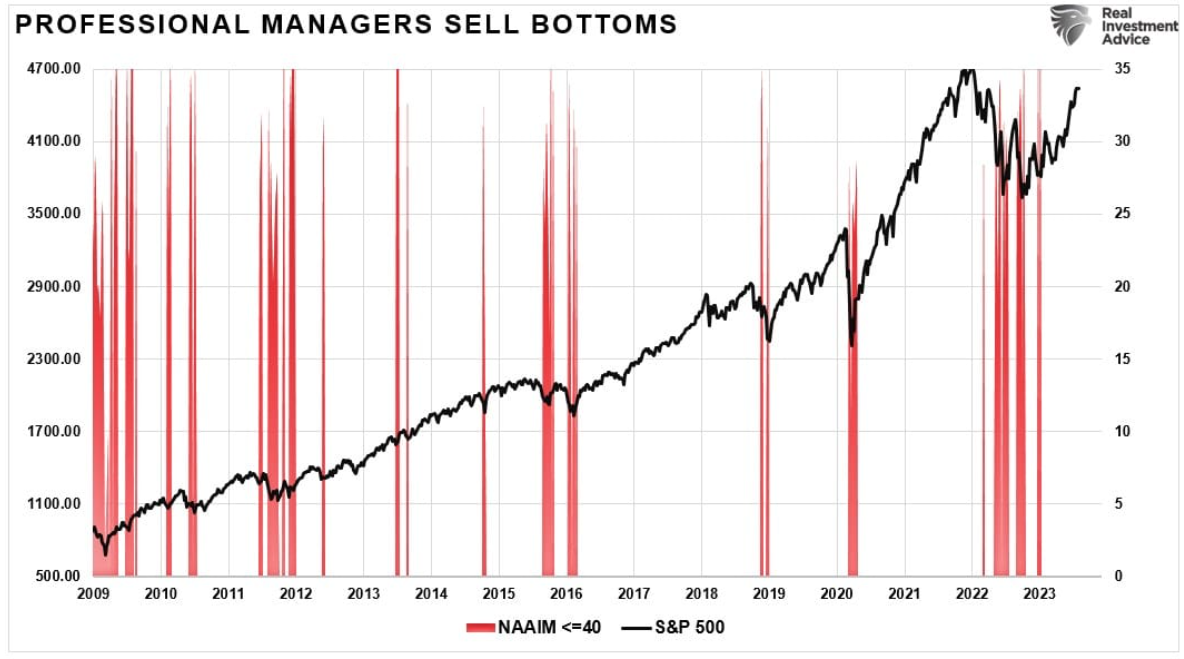

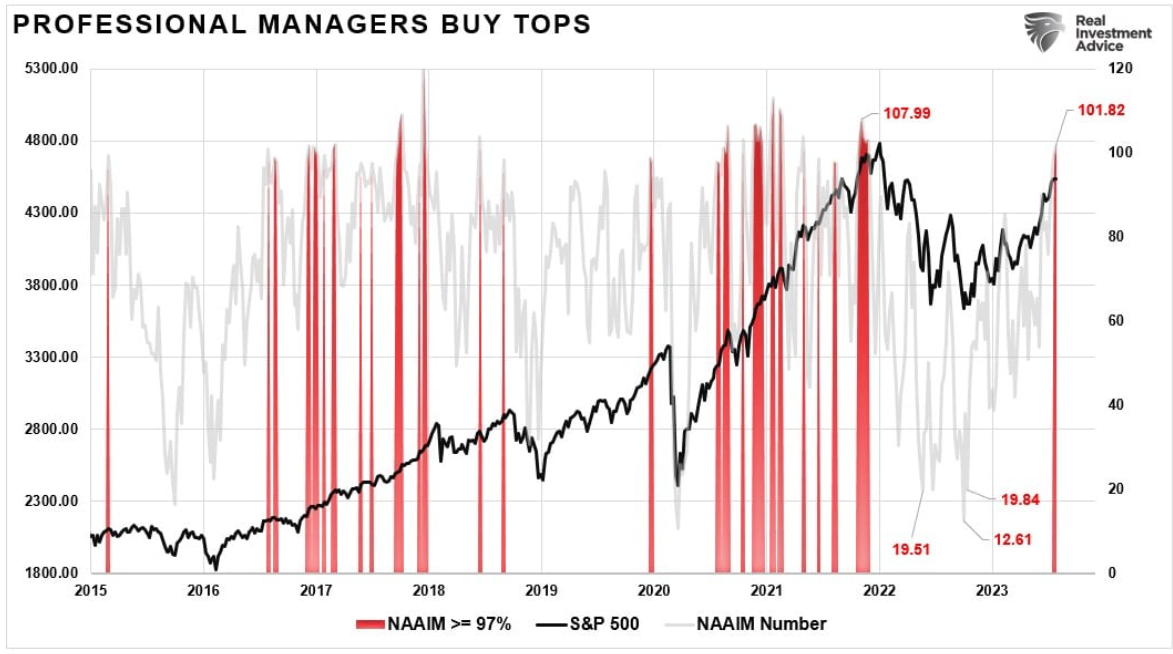

Nonetheless, the surge in the markets reversed that extremely negative bearish sentiment. One measure we look at is the NAAIM sentiment survey of professional investors. This index measures the level of equity exposure of institutional managers every week. Last year, equity exposures were cut near the market lows as managers sold.

Today, those exposure levels are increasing rapidly. From a contrarian perspective, professional investors have a long history of selling bottoms and buying tops.

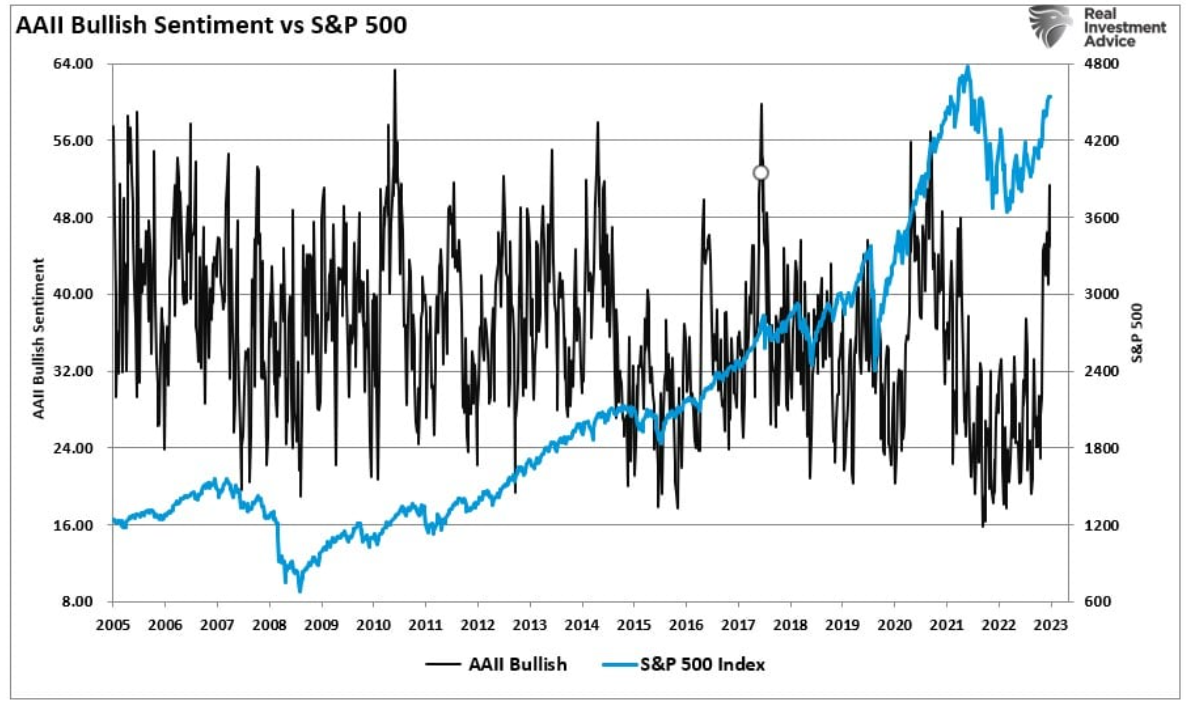

However, it isn’t just professional managers piling into the equity market but retail investors also. In 2022, retail investor sentiment also hit extremely bearish levels. As retail investors capitulated and repurchased equities, the market surged higher, rapidly increasing their bullish sentiment.

Unfortunately, these more exuberant bullish readings are the antithesis of the bearish readings. While extremely bearish readings tend to denote short-term market bottoms, extremely bullish readings historically suggest short-term peaks.

A Correction Is Likely

The shift from bearish to bullish sentiment has been steady since the beginning of March. The capitulation of bearish investors continues to push markets higher. Retail and professional investors’ “Net Bullish Ratio” tells the tale.

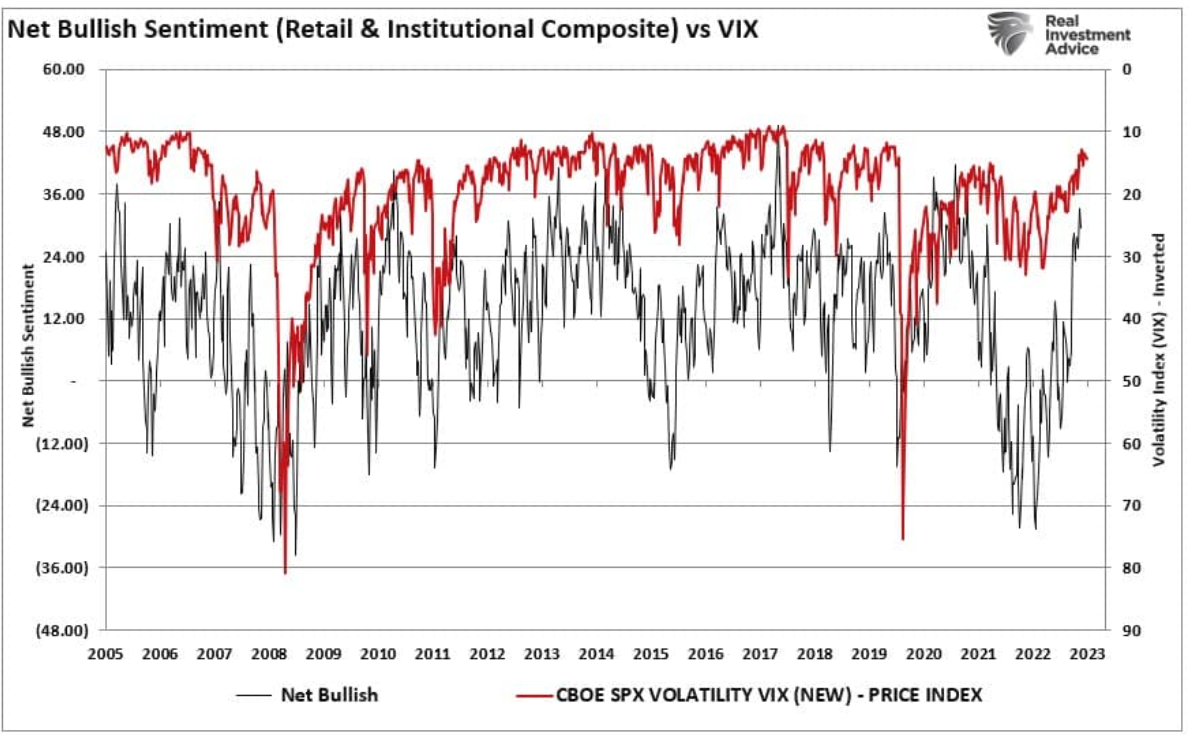

The surge in optimism unsurprisingly resulted in a collapse of market volatility which is also reaching more extreme levels.

The turn in sentiment resulted from the “pain” felt by investors on the sidelines. While that turn in bullish sentiment is not yet to more extreme levels, it is often the sign of the end of a rally rather than the beginning of one.

As a contrarian investor, excesses get built by everyone on the same side of the trade. Previously, everyone was so bearish that the bullish trade higher was inevitable. Today, it is the opposite.

Regardless of your personal views, the bull market that started in October remains intact. However, given the more extreme levels of optimism in the short-term, plenty of evidence suggests a near-term correction is likely. The technically overbought conditions of the market confirm the same.

However, such does not mean selling everything and going to cash.

What I am suggesting is that when “sell signals” are given, individuals should perform some essential portfolio risk management such as:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that are not working (Positions not working in a rising market won’t work in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

There is minimal risk in “risk management.” In the long term, the results of avoiding periods of severe capital loss will outweigh missed short-term gains. While I agree you cannot “time the markets,” you can “manage risk” to improve long-term outcomes.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors.

He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Disclosure & Privacy Policy

Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with over $1 billion in assets under management. As a team of certified and experienced professionals, we seek to provide our clients with educational services and the necessary information and tools to educate you in the field of finance, investing and economics. To this end, you can use the Real Investment Advice Platform to avail yourself of various video, audio and proprietary collections of information at your leisure to learn and gather the necessary information that you may need in the fields of investment news, investment opinion, financial news, financial opinion, economic news and economic opinion, finance, investing and economics. Utilizing the functionality and tools provided by Real Investment Advice, you can access this information in a variety of ways, including via video and audio programming, audio and visual media content streaming services, downloadable audio-visual media, uploaded, posted or tagged third-party videos, receiving or viewing audio and video clips, blogs, podcasts, and YouTube videos, all of which are accessible on the Real Investment Advice media platform and/or various Internet and communications links that are accessible via the Real Investment Advice Platform and allow for the broadcasting, transmission and streaming of the information and audio-visual content to your media devices and other communications platforms for your viewing and listening pleasure. All of these tools and sources of information are made available to you so that you can utilize the same to make the right financial, economic and investment decisions.

RIA Advisors offers multiple custodial arrangements, either directly of through wholly owned subsidiaries, with Fidelity, TD Ameritrade, Charles Schwab and Interactive Brokers.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice