The nation's complex and contentious fiscal processes are deemed a credit risk.

In 2011, I had just started a long-overdue vacation in Wisconsin when news broke that Standard and Poor’s (S&P) was downgrading U.S. government debt. On Tuesday this week, Fitch Ratings did the same thing…while I was enjoying time off in Wisconsin. My boss has already informed me that travel across the state line from Illinois will be strictly forbidden from now on.

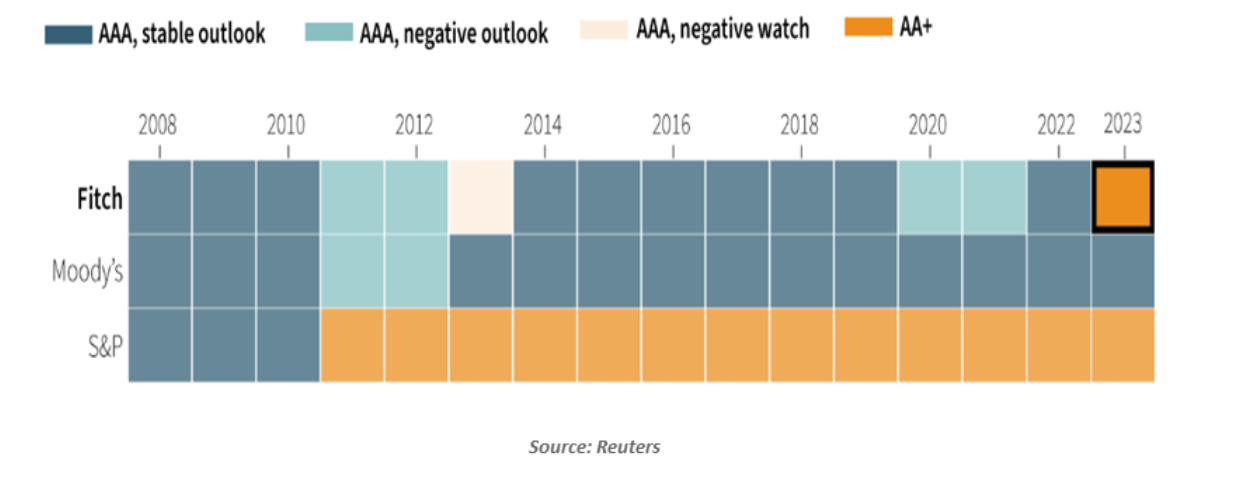

Issuance of bills, notes and bonds will now carry an AA+ rating from Fitch, down from AAA. The United States has a lot of companies at the new level; there are now only nine sovereigns in the world that still carry the top grade.

The timing of the Fitch action was interesting. The decision cited “a high and growing general government debt burden” and “a steady deterioration in standards of governance over the last 20 years, including on fiscal and debt matters.” While both issues are troubling, neither is novel. The debt ceiling debacle, which frustrated investors for weeks, was resolved two months ago with bipartisan support.

However, fiscal discussions since then have showcased the difficulty that America faces in dealing with its debt and deficit problems. The budgeting process itself is awkward; broad outlines can be approved, but battles over the details can still end in stalemates. Twelve major appropriation bills have to be adopted every year by September 30; that affords plenty of opportunity for friction.

As an example, approval of defense spending for the coming fiscal year became more challenging when the House added clauses dealing with unrelated social issues. A battle with the Senate is upcoming. Congress is currently in its summer recess; September 12 is the next date both chambers will be in session. A government shutdown at the beginning of October is looking more and more likely.

So far, trading in Treasury securities does not indicate undue stress. The U.S. government has been issuing heavily over the past two months to replenish accounts depleted by the failure to lift the debt ceiling; there have been no signs that the market is reluctant to absorb the supply.

Nonetheless, the Fitch report reinforces the notion that the finances of the United States are on a troubling trajectory. Interest rates have risen, and aging demographics are placing greater demands on the budget every week. Reform will require some combination of tax increases and cuts to major spending programs like Social Security, Medicare, or defense. The politics surrounding these areas makes reaching solutions nearly impossible.

Until Washington improves its fiscal policies, its grade from rating agencies will remain under pressure. And that could prove hazardous to my future vacation plans.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust