The common currency has not led to common outcomes.

After almost a decade of preparations starting in the early 1990s, the euro saw the light of day in January 1999. The idea was that a common currency union would increase economic convergence among member states. Twenty-five years later, these expectations have not been met. Europe’s economic performance has been anything but homogenous.

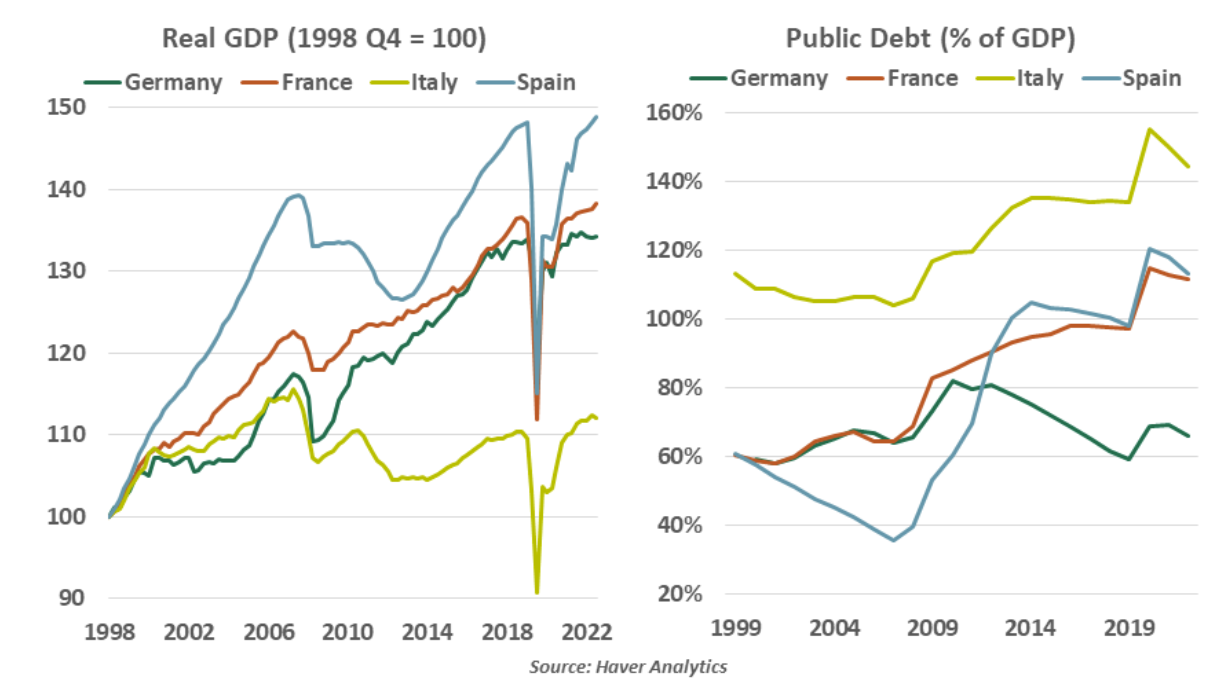

Countries like Spain and Austria have expanded at a rapid rate, benefitting from a common market and currency. Others, like Italy, didn’t gain much from joining the bloc. The Italian economy has expanded by a little over ten percent in 24 years, showcasing the stark divergence among the member states.

Over the years, economic differences have persisted due to differing models of growth embraced by individual governments. Nations like Germany, the Netherlands and Austria have pursued an export-oriented growth model. They are also among the frugal states with low public debt and deficit levels. On the other hand, southern states have had a history of spending beyond their means, leaving them on a shaky pile of debt. Periodic devaluation of domestic currencies was the main instrument for countries like Italy, Portugal and Greece to maintain their competitiveness prior to 1999. Joining the monetary union meant giving up an important economic policy tool.

The economic gap between countries has become more apparent in the post-COVID era. While output declines were uniformly large across the currency union in the initial phase of the pandemic, the recovery has been uneven. The largest eurozone economy, Germany, is fighting to avoid a recession. Italy is barely growing. Spain and France have performed well in the first two quarters of 2023. Purchasing Managers’ Indexes are pointing to continued divergence into the third quarter.

After COVID put all economies on shaky ground, the energy shock related to the Ukraine War contributed to the current uneven recovery. Germany, being an industrialized economy, was the most impacted by the energy crunch. The crises forced the otherwise frugal northern state to spend large sums of money to shield households and firms. Berlin’s fiscal support to combat the energy shock was among the largest in Europe, amounting to 7.5% of gross domestic product.

The French and Italian economies have somewhat improved their competitiveness in the past few years. However, “Germany has gained by far the most from the introduction of the euro”, according to a report by the Centre for European Policy. Politics and institutional strength have also played their part. Frequent changes in leadership in Italy have been major a hindrance to coherent economic policies. The French government has been more stable than in Italy, but domestic conflicts have often blocked the path of unpopular reforms. In contrast, Germany is known for its strong institutional framework, thus enjoying greater investor confidence.

This has made policymaking a challenging task, especially during episodes of stress. Between 2010 and 2015, heads of European governments met on more than 50 occasions before agreeing to painful rescue packages for struggling member states like Greece, Ireland and Portugal. Reforming the bloc’s fiscal rules remains contentious.

The structural differences between the economic models of the member states are unlikely to close meaningfully anytime soon. A significant problem arising from this lasting divergence is that it would feed discontent and hurt prospects of further economic integration. The expansion of the euro area, most recently adding the relatively poor nation of Croatia, will only add to the risk of the union becoming too heterogeneous.

The Euro project was already under persistent pressure before the pandemic with forces like the sovereign debt crisis, the rise of populism, managing immigration and Brexit, all testing the unity of the monetary union. Yet, the euro has survived and grown, with eight additional nations adopting the currency since its inception in 1999.

However, surviving is not the same as thriving. Without closer alignment across political and fiscal policies, the monetary union will simply continue to stumble forward, but not prosper.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust