- Entering 2H23, our Key Themes are unchanged, and we highlight Theme #2 Expect the Unexpected.

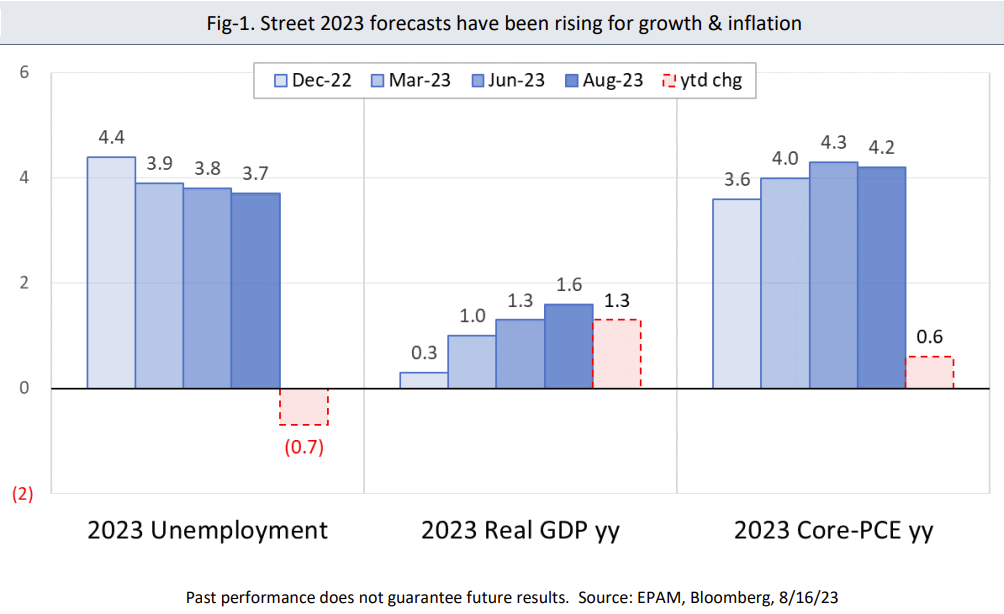

- In January, markets expected 100bps of Fed cuts in 2H23 and Wall Street forecasters expected a recession to start by year-end. We disagreed and, in our “2023 Outlook” (1/19/23), outlined two non-consensus calls; 1) Rates would be higher-for-longer (Powell wants to be Volker, not Burns), and 2) US growth & inflation would be resilient (“Reflexive Policy Cycle”). Just six months later, and despite 3 of the 4 largest bank failures in US history, Powell has hiked 100bps and, for 2023, markets no longer expect Fed cuts and forecasters no longer expect a recession.

I found a flaw in the model that I perceived as the critical functioning structure that defines how the world works. – Greenspan

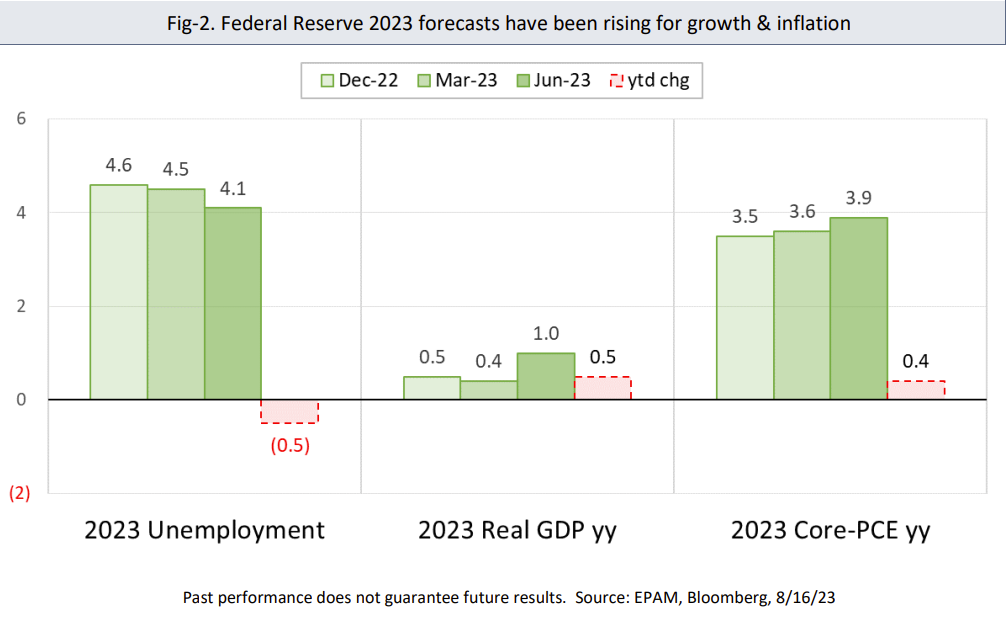

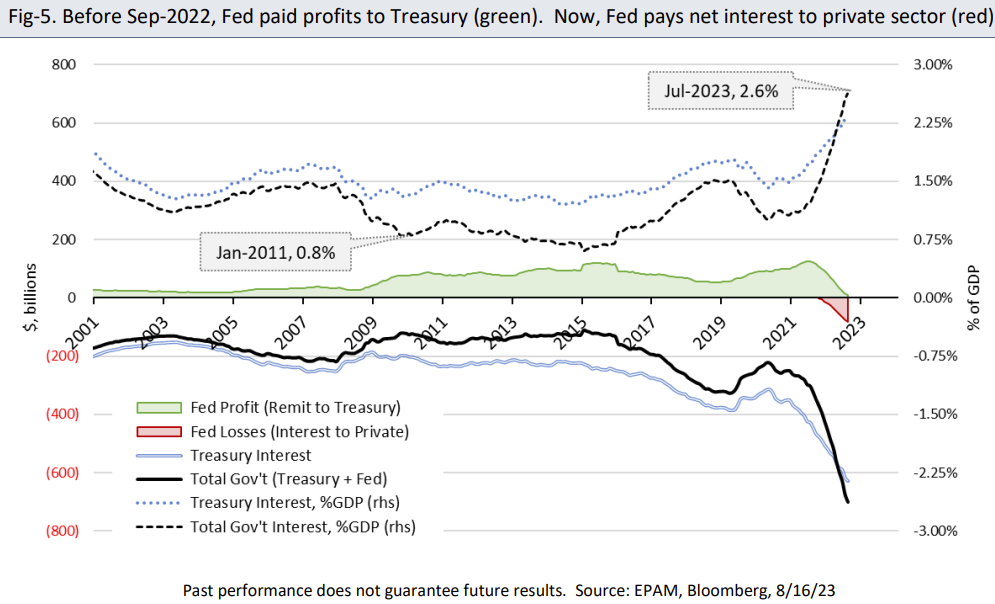

- Rates are at 20-yr highs, yet unemployment remains at 50-yr lows, core-PCE is near 30-yr highs, and Wall Street (and Fed) economic forecasts continue improving. Pg-2. What explains the disconnect between these unexpected outcomes and those expected by mainstream economic textbooks? Consensus says: monetary policy works with long & variable lags. We say: it’s the Fiscal, Stupid!

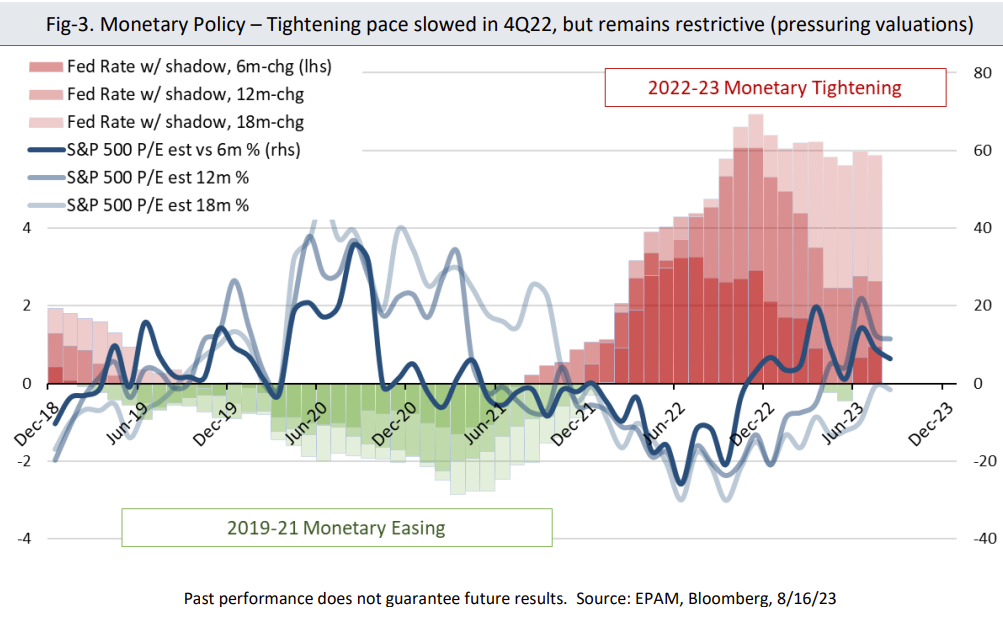

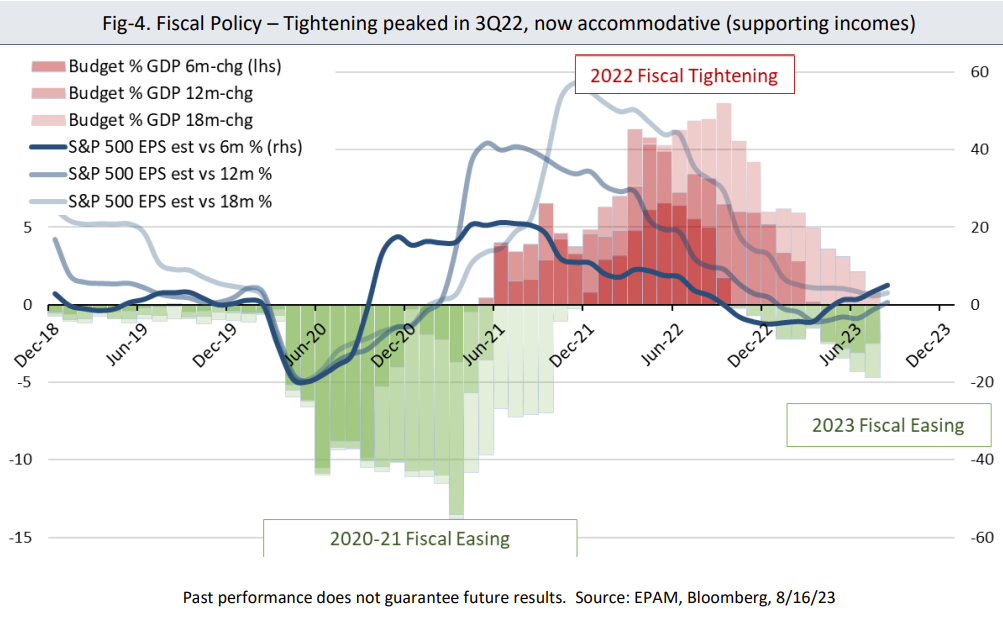

- Our summarized policy framework: Monetary affects valuations and Fiscal affects incomes, but Monetary actions have Fiscal implications. In 2020-21, monetary and fiscal easing boosted valuations and incomes. In 2022, monetary and fiscal tightening pressured valuations and incomes. Entering 2023, we expected monetary to remain restrictive (suppressing valuations) while fiscal turned accommodative (supporting incomes). Pg-3. Importantly, we expected monetary tightening (higher rates) to accelerate fiscal easing (higher interest), reinforcing a procyclical “Reflexive Policy Cycle”.

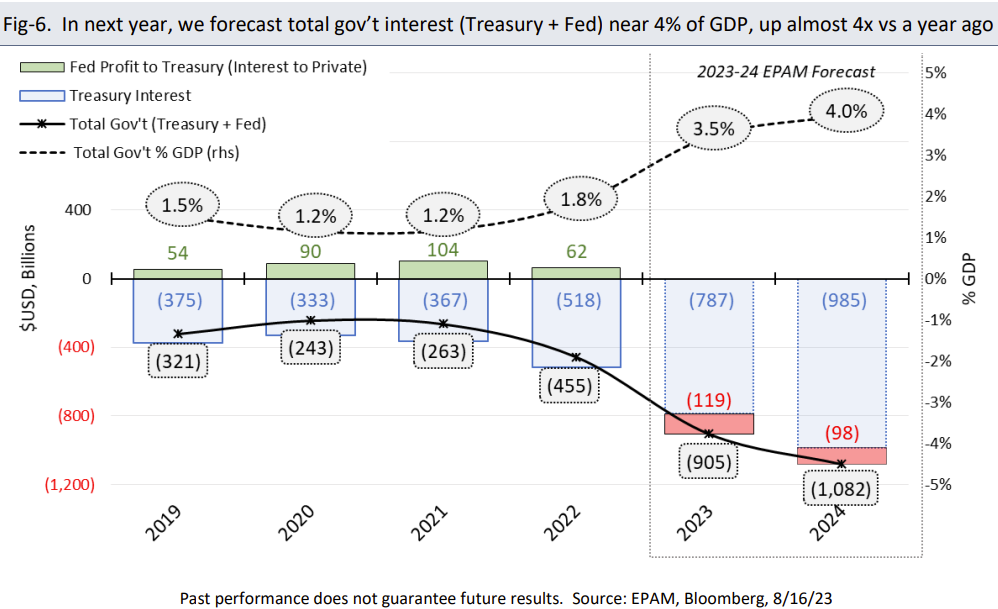

- Thus far, our 2023 policy forecasts are proving correct. The Fed has hiked 100bps YTD (to 5.5%) and, per its latest projections, may hike again by year-end. The budget deficit/GDP has widened 300bps YTD (to 8.4%) and, due to Fed rate hikes, is set to widen further as interest expense explodes higher. Importantly, the Fed now pays net interest to the private sector (rather than profits to Treasury), so total government interest (Treasury + Fed) is rising even faster. Over the next year, we forecast total interest will reach 4% of GDP (Total $1,000B = Treasury $850B plus Fed to private sector $150B), up almost 4x from a year ago (Total $250B = Treasury $350B less Fed to Treasury $100B). Pg-4.