U.S. companies broadly notched better-than-expected results in the second quarter, even as overall earnings growth for the S&P 500 saw a decline. Equity investor Carrie King sees more interesting developments beyond the numbers and posits one area that may be getting tired as another readies for a reawakening.

By the numbers

Earnings for S&P 500 companies largely came in better than expected for the second quarter, even as analyst expectations had been rising throughout the reporting season. The number of companies beating estimates on both sales and earnings was slightly better than the historical average, yet stock prices were not well rewarded for their relatively strong showing. It may be that much of the good news is already baked into prices.

Overall, the S&P 500 is tracking for a year-over-year earnings decline, dragged down primarily by energy and materials. Many analysts have suggested that Q2 could represent the trough, with an earnings upturn kicking off in Q3.

Consumer discretionary led among S&P 500 sectors, with the hotels, restaurants and leisure segment more than doubling its prior year’s earnings growth. The average market reaction to beats in the sector: a disappointing -2.3% return the day after reporting.

Beyond the numbers

Much of our analysis as forward-looking fundamental investors center on what companies are saying and parsing that alongside the data.

The numbers suggest consumers are still making up for lost fun since the pandemic. And the rhetoric from travel and restaurant company managements has been equally buoyant, with notes of “further acceleration,” “improving trends,” “good momentum” and even some “surprised by consumers’ resilience.”

But the market reaction seemed skeptical and, to be sure, consumers’ pockets are only so deep. Retailers of hardlines have suggested “see-through is not good,” the “online marketplace is more competitive” and “promos are ramping up.”

Consumers, it seems, are having to make choices. They are prioritizing experiences over goods, managing their pantries, exercising caution and value searching even in packaged foods. Staples companies are seeing consumers buying bulk for value, going to smaller packages to manage their budgets, or not replenishing.

Consumers growing tired

Despite a strong earnings season, the fact that consumers are making trade-offs to reprioritize their spending suggests some prudence may be warranted going forward.

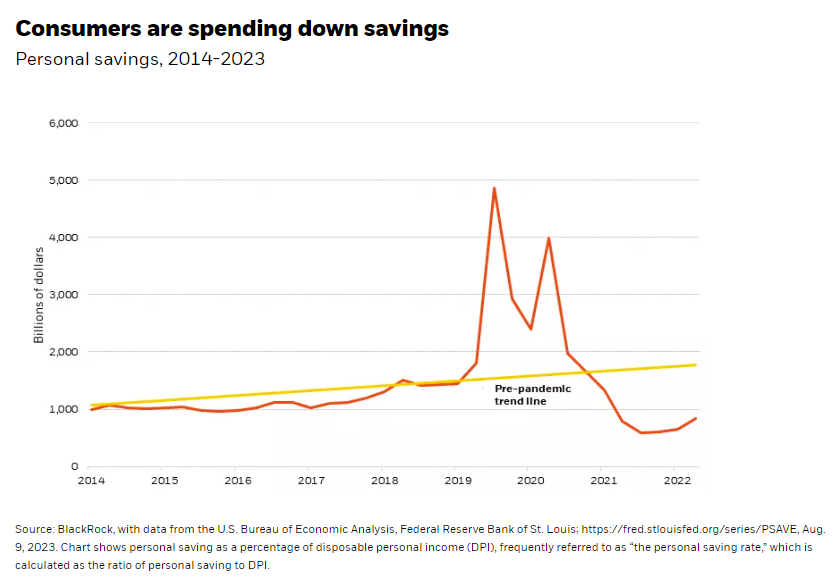

U.S. households still have roughly $500 billion in aggregate excess savings accrued either through reduced spending or relief payments received during the Covid pandemic.1 But as shown below, those savings are on a rapid drawdown.

Wages have been growing and unemployment is near a 50-year low of 3.5%.2 Yet inflation remains elevated, interest rates on mortgages and consumer credit are higher, and the government is ending its three-year pause on student loan payments this year. Household debt rose to $17 trillion in the second quarter, according to the Federal Reserve Bank of New York, with credit card balances touching a new high.

All told, we may be nearing the end of the consumer boom ― and this clouds the picture going forward. We remain selective in consumer companies and generally see greater potential in experiences over goods, as spending on services is still shy of pre-pandemic levels.

Industrials due for an awakening

On the opposite side of the ledger is industrials, where Q2 earnings came in mixed but we see the seeds of opportunity being sown. One signpost is the world’s largest maker of construction equipment. The company posted stellar results amid healthy demand, an outcome we believe could repeat across the sector as long-awaited spending and investment finally begins to materialize.

What might prompt the spend? Catch-up from years of deferred infrastructure upgrades; a deglobalization trend that could see companies relocating their operations closer to home; global decarbonization efforts that will require the build-out of new eco-friendly systems, along with government programs that earmark funding to advance those efforts; and increased interest in automation as a shrinking working age population makes the case for industrial and technological automation of processes.

After a long period of underinvestment, we believe these secular drivers could power an acceleration in industrial spending and underpin future growth. While consumers have been “pedal to the metal” for some time, we expect that momentum could wane just as the building blocks of an industrial resurgence could be in formation.

1 Source: Federal Reserve Bank of San Francisco, May 2023.

2 Source: Bureau of Labor Statistics, July 2023.

Earnings figures cited herein are from BlackRock Fundamental Equities, with data from Refinitiv and FactSet. Figures are as of Aug. 9, 2023, with 82% of S&P 500 companies reporting.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of August 2023 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

Prepared by BlackRock Investments, LLC, member FINRA.

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

© BlackRock

Read more commentaries by BlackRock