The Northern Trust Economics team shares its outlook for U.S. growth, employment, interest rates and inflation.

The longer a soft landing remains possible, the more likely it starts to feel. Falling odds of a recession are an optimistic signal, but the celebration is premature. The battle against inflation is not yet won and will be complicated by continued wage gains and the recent rise in energy prices.

After a slow start, the Fed has erred on the side of acting to fight inflation in this cycle. We do not expect them to pull back anytime soon. History offers several examples of the Fed cutting rates too eagerly, prompting reflation. Whether or not the hikes have concluded, rates are likely to hold at elevated, restrictive levels well into 2024. Over that prolonged period, higher borrowing costs will be felt more clearly, constraining growth, but hopefully not tipping the economy into recession.

Amid so much uncertainty, layoffs have been subdued and consumer spending has durably grown. These factors will help the economy keep its buoyancy and grow through the year to come.

Influences on the Forecast

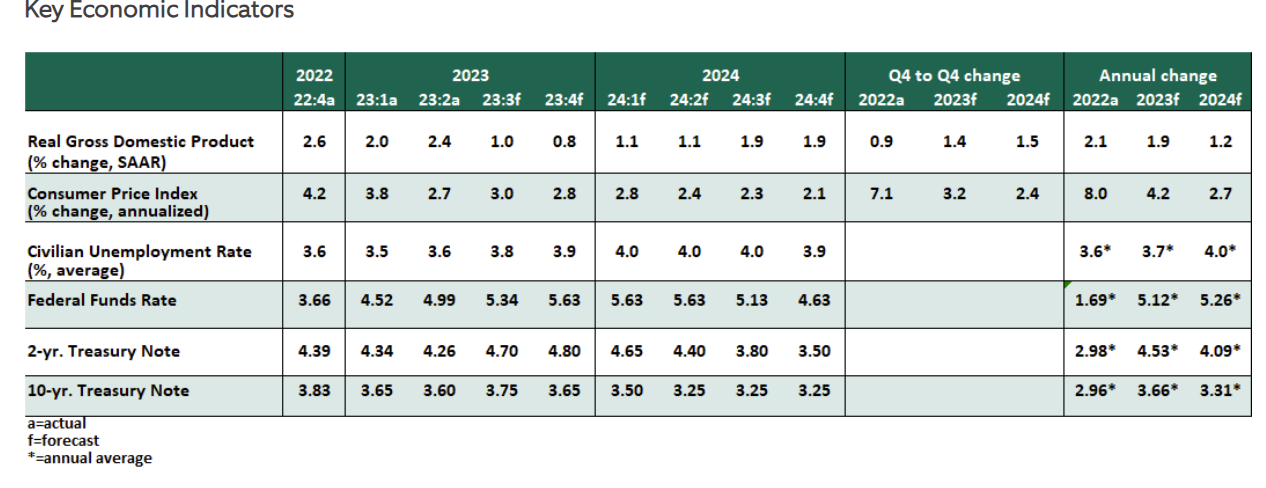

- All eyes remain on inflation. The headline consumer price index (CPI) grew 3.2% year over year in July. Excluding food and energy, core prices advanced at a rate of 4.7%, its slowest gain in 20 months. Growth in the deflator on core personal consumption expenditures improved to 4.1% in June, still well above the Fed’s 2% target. Measures of the costs of housing remain elevated despite expectations of a fall; gains from lower airfare and used car prices are unlikely to sustain. While these readings are much better than the frightening heights seen a year ago, they are not yet normal.

- Labor markets are showing signs of cooling. In July, 187,000 jobs were created. Over the past six months, job gains have averaged 222,500, compared to the average of nearly 400,000 in 2022. Monthly payroll increases are still elevated relative to pre-COVID norms; job creation from 2016-2019 averaged under 200,000 per month, and further cooling is likely. The unemployment rate improved slightly to 3.5%.

- Job openings have entered a declining trend, and the rate of voluntary quits is sliding, though both remain higher than their pre-pandemic trends. Layoff rates have not yet risen. A decline in demand for labor without job losses would be an optimal outcome.

- Average hourly earnings have settled into a growth rate of about 4.4% year over year. Wage gains outpacing inflation mean that workers are again seeing real wage increases, which brings a risk of spurring more spending and another inflationary cycle.

- In July, the Federal Open Market Committee (FOMC) raised the Fed Funds target rate to a range of 5.25-5.50%. The hike was well-signaled, and the accompanying statement and press release offered no insight as to the next steps for U.S. monetary policy. Every upcoming meeting should be considered “live” for a potential rate hike.

In the context of its dual mandate of stable prices and maximum employment, the FOMC has relatively little work left to do. We believe still-elevated core inflation will compel one more hike, followed by a prolonged hold through the first half of 2024.

The Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) showed continued tightening of bank lending standards across loan types in the third quarter. This measure received more attention in the wake of the failure of Silicon Valley Bank, though the tightening trend predates that disruption. More limited access to credit will impair economic growth and potential business expansion; this is an example of the long and variable lags of tighter economic policy.

- In the second quarter, U.S. gross domestic product (GDP) grew at an annualized pace of 2.4%. The upside surprise this quarter was strong business investment, an encouraging signal for demand and employment ahead. Rebuilding flat inventories and a return on residential investment are poised to contribute to GDP growth in the quarters to come.

- Amid a strong year for risk assets and a consensus shift away from imminent recession, volatility in fixed income markets has grown. We believe the primary driver has been a reassessment of how long monetary policy will remain restrictive. A higher-for-longer outlook for short-duration bonds is causing a repricing across the yield curve.

- The downgrade of U.S. sovereign debt by Fitch Ratings was well justified in principle but came at an odd time. Correcting the nation’s declining fiscal trajectory will not be quick or easy, but the cost of inaction is beginning to rise.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust