Better productivity is easing employers' burden of higher wages.

In our writing and speaking, we try to strike a balance that shows we understand a variety of perspectives. This is easier for some topics than others.

Wages can be a particularly difficult subject on which to strike a balance. From the worker’s perspective, who wouldn’t want to get a raise? It’s a reward for good work and enables a better quality of life. But from the employer’s side, higher wages are a greater cost that can impact profit margins. Economically, higher incomes bode well for consumption. However, when workers see rapid wage gains, the risk of a wage-price spiral emerges: better pay fuels more consumption, driving up prices, and leading workers to demand further raises.

We have thus watched trends in hourly earnings closely through this inflationary cycle. They followed a similar path as most measures of inflation: from a peak of a 5.9% annual gain in March 2022, they have cooled, most recently to 4.4%. The current rate is higher than the former norm, and the normalization has stalled; in the pre-pandemic cycle, wage gains peaked at 3.6%.

Fortunately, higher compensation is not always inflationary. Workers’ pay should reflect their output. More productive workers are more valuable. In a well-functioning labor market, they will receive higher pay. The latest measures of productivity suggest this stage of the cycle has commenced, calming some of our worst fears of the inflationary effects of higher wages.

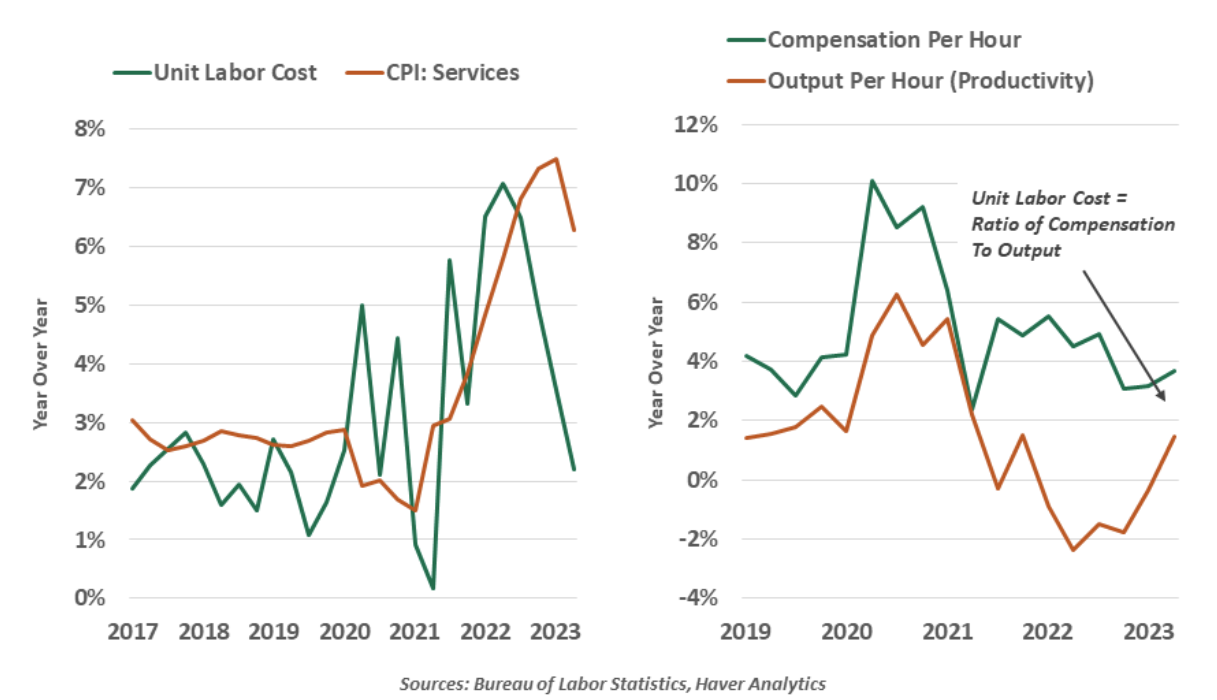

Second quarter U.S. productivity data showed an encouraging slowdown in unit labor costs (ULC): the measure of what employers pay for the output they receive from their employees. Compensation is still growing at a steady rate, but output increased. In effect, employers are getting more bang for their payroll buck.

Productivity tends to follow a pattern in economic cycles. As a recession begins and workers are laid off, the remaining workers maintain output, boosting productivity. Then, lower demand leads to lower output, and productivity declines with it. In this cycle, the pattern played out swiftly. Productivity was also challenged by the “great resignation:” Experienced workers changed jobs or retired, and new hires needed time to reach their potential. Now, as the labor market settles into a state of lower turnover, employers are seeing some upside in better productivity.

Employers are also limiting their wage bill by keeping a lid on hours worked. The average hourly workweek has declined from a peak of 35.0 hours in January 2021 to 34.3 in July. The curtailment has been in the service sector; while goods-producing occupations like construction and manufacturing are holding steady, services like hospitality and retail trade drove the overall decline. Employers appear to be managing their wage costs by containing hours rather than reducing headcount, a symptom of labor hoarding.

These trends are important in the context of concerns about ongoing services inflation. The pandemic disruptions included a stay-at-home bubble that raised demand for goods. Prices of goods increased amid shortages and then deflated as the economy reopened and spending shifted back toward services. Prices of services then entered an interval of higher inflation…and they have been slow to cool. Services inflation in the consumer price index peaked at 7.6% year over year at the start of this year. The most recent measure of 5.7% shows progress toward normal, and higher productivity is helping to make that high rate tolerable.

All of this adds up to a less concerning picture for a service-led inflationary cycle. The rise in prices is tapering. Wages are growing, but higher productivity is easing the burden on employers. As services are more labor-dependent, this bodes well for a more normal trend of services inflation to come. Finding balance in the labor market has been difficult, but if these trends persist, there will be good news for everyone.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

© Northern Trust

Read more commentaries by Northern Trust