Volatile rates are adding to the cost of residential debt.

Purchasing a home will stretch most budgets. For recent home buyers, the cost of debt has been the biggest burden. This week, 30-year fixed mortgage rates quoted in the Wall Street Journal exceeded 7.7%, a level not seen since the year 2000. While the rising rate environment is a central feature of this economic cycle, most other long-dated debt has not seen such a sharp increase in cost. Why are mortgage rates so stretched?

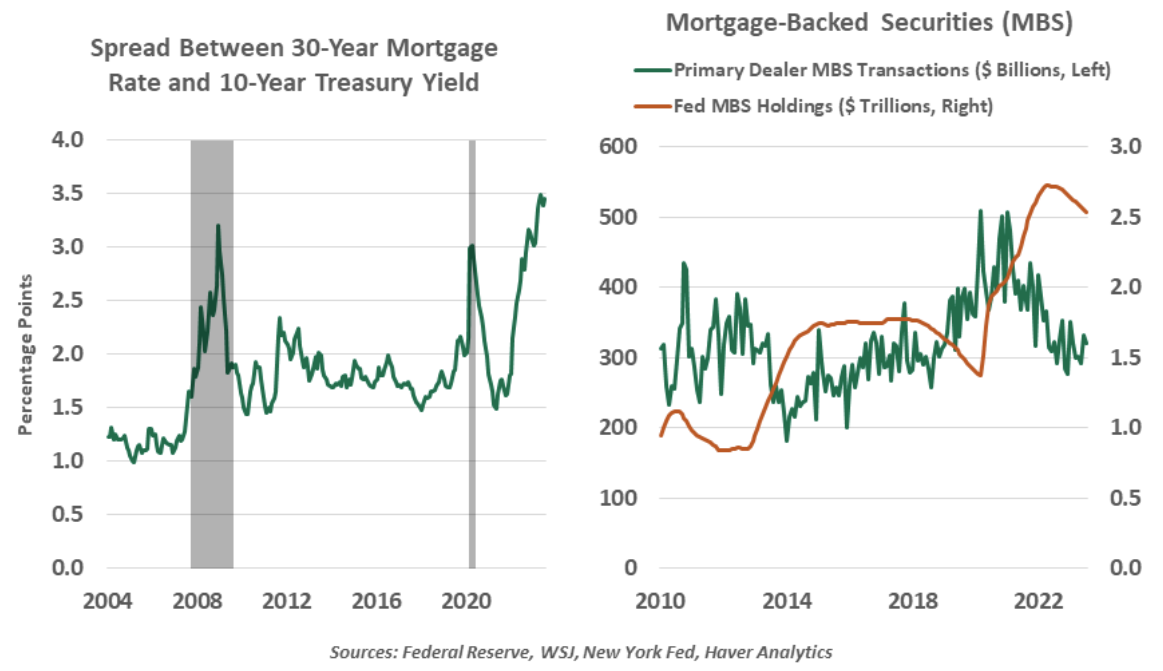

Mortgage rates closely track the yield on 10-year U.S. Treasury notes. Mortgage originators charge a premium over this base rate to compensate for credit risk and the costs of origination and servicing. This spread has reached new highs over the past two months, now holding at a level that exceeds even the spreads seen during the housing-led financial crisis of 2008.

Part of the elevated spread is due to the decline of the mortgage-backed security (MBS) market. Most mortgages are repackaged into MBS, and sold to fixed income investors. However, the Federal Reserve ceased net purchases of MBS when it ended quantitative easing in early 2022, removing an important buyer from the MBS market. Banks are also hesitant to invest in long-term assets like MBS when they are fearful of short-term liquidity constraints. MBS deals must offer a premium to attract a more limited set of buyers.

Interest rate volatility is also a driver. Mortgage lenders face rate optionality, first from the rate lock available during the origination process, and then the risk of prepayment over the life of the loan. Instruments to hedge these risks are more expensive in volatile rate environments. Also, securitizing is not instantaneous. Originators hold onto mortgages while packaging them into MBS deals, and their cost of warehousing loans grows with higher, unpredictable rates.