The Fed's asset portfolio is on an uncharted course.

Anyone who has been to Jackson Hole will agree that the view of the stars there is breathtaking. The absence of ambient light creates the perfect setting; it almost seems that the heavens are right on top of you.

At the recently concluded central banking summit in Jackson Hole, there was a lot of talk about stars…of the economic kind. Equilibrium levels of macroeconomic variables are often identified with a star; substantial efforts are made to define those levels and to use them strategically. Of particular interest at this year’s conference was the neutral level of monetary policy, which neither stimulates nor inhibits economic activity.

There are two aspects to this. The first is the natural long-run level of interest rates, or “r-star.” A confident estimate of r-star is critical to determining whether policy is tight or easy. It is also critical to helping markets center their expectations of where interest rates might be heading in the future, based on incoming economic information. Unfortunately, this year’s conference in Wyoming did not yield any additional clarity on where the nebulous R-star stands.

Getting relatively little attention in Jackson Hole was the star denoting the neutral level of central bank balance sheets. Quantitative easing programs have been employed to a substantial extent in the wake of the last two economic crises, and they have had a significant influence. With inflation running higher than desired, quantitative tightening (QT) is underway in a number of countries. Yet we don’t have a sense of where or when this process will end.

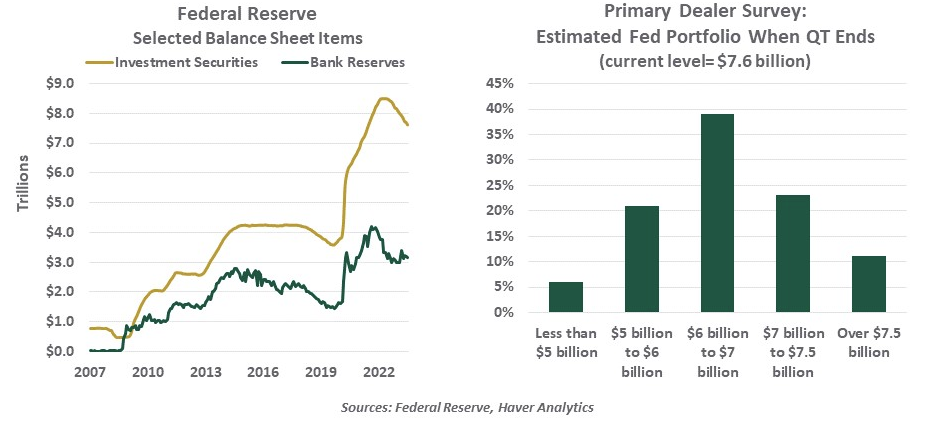

The Federal Reserve’s balance sheet has been declining for more than a year now, by a total of almost 8%. As a consequence, the U.S. money supply has fallen by 3.7% over the last twelve months. The withdrawal of excess liquidity from the financial system has impacted bank deposit levels and conditions in the fixed income markets. Wider mortgage spreads are one prominent byproduct.

The Fed is running its securities portfolio down at a targeted pace of $95 billion each month. It is difficult to discern how much further QT will go on, because we have little notion of what the equilibrium level of a central bank balance sheet should be. The Federal Reserve periodically asks primary dealers in Treasury securities to estimate how much further the Fed’s portfolio will decline; the most recent survey was conducted in July, and showed a wide dispersion of opinion.

Another angle on this question comes from the Federal Reserve’s survey of bank chief financial officers (CFOs). Banks hold reserves with the Fed for a variety of reasons: they help to satisfy liquidity and capital requirements, and they provide a source of cash that can be deployed when needed. Of late, they also provide very good risk-free rates of interest.

But QT essentially reduces the level of reserves available. The Fed’s latest CFO survey indicates a desire among banks to maintain or increase balances held at the Fed. The banking stress of the spring is a leading factor driving these intentions.

If the Federal Reserve reduces its portfolio too far, it creates a pinch point for financial markets and intermediaries. This was the case in 2019 when the Fed was forced to stop its QT effort many months before it intended amid increasing signals of liquidity stress. Post-mortem analysis suggested that the Fed had underestimated the core demand for reserve balances.

Another reason to better understand the equilibrium size of a central bank’s holdings is to keep interest rate and balance sheet policies consistent with one another. The two should not be working at cross purposes; knowing where each is relative to neutrality will be critical to this ideal.

Even on a clear night, some constellations are distinct while others are blurry. Central banks will need better telescopes to steer clearly in the months ahead.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust