Higher yields on cash have allowed some de-risking.

Every accounting student starts by learning some simple rules: Assets equal liabilities plus equity, and every liability must have an offsetting asset. Before long, we start to see the tradeoffs everywhere, in our household finances and beyond. A new vehicle is an asset, but it’s offset with a new loan or a reduction in cash. A mortgage is a major liability, but the value of the underlying home is also significant.

The high interest rate environment has brought a lot of focus on liabilities. Borrowing costs are higher, which hinders economic activity. Major purchases like homes and vehicles become more expensive. Businesses seeking to expand will find debt financing to be more costly and difficult to procure. Indebted nations will find their fiscal balance even further strained by higher interest obligations.

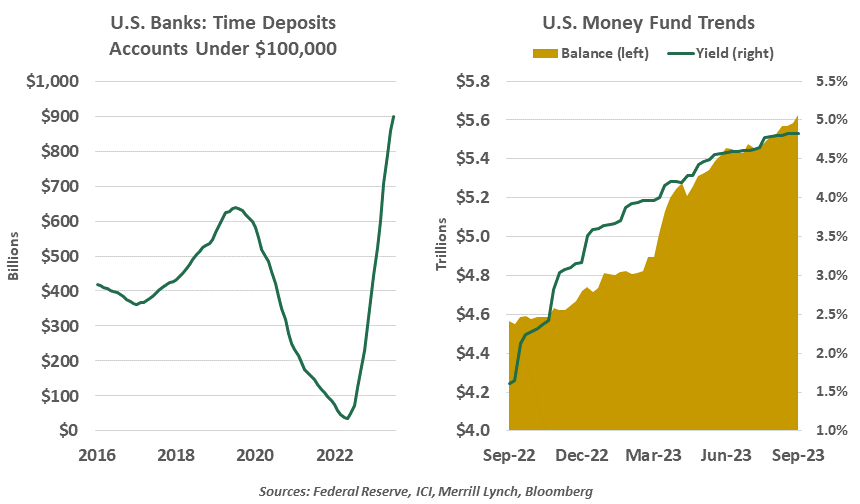

But the other side of the interest rate ledger has been somewhat overlooked. Households are earning significantly more on deposits; banks are raising their offered rates and are competing against each other for deposits in a way that had been unnecessary during a period of easy money.

Deposits are not savers’ only option, of course. Money market funds have seen balance inflows for more than a year now, with extra impetus in the wake of the failure of Silicon Valley Bank. With their access to the Federal Reserve’s overnight reverse repo facility, money market funds can comfortably offer annualized returns over 5%, in a safe and liquid vehicle.

Even on the liability side, consumers can find some good news. Many consumers are carrying debt at old rates that are no longer attainable. These consumers have lucked into a carry trade, keeping any extra cash in a high-yield bank account and paying only the minimum required on their old debt. The spread is small and won’t last forever, but it’s a welcome bonus for many households.

Individual and institutional bond buyers are also catching an upside and earning favorable income on their holdings. Newer market entrants are at the most advantage: bond holders endured a painful year in 2022 as higher yields pushed down the values of more seasoned bonds. With that repricing complete, investors have their pick of sovereign, investment grade and high-yield bonds, many of which offer interest well in excess of the rate of inflation.

A final benefit worth contemplating is greater investor discipline. The near-zero interest rates of the prior decade led many portfolio managers to reach for yield. In that search, they placed capital into sectors with which they may not have had deep experience. In the process, they ran up against the boundaries of their risk tolerance.

Higher yields on cash have allowed some de-risking. This has been especially helpful to the pension sector, which has taken the opportunity to lock in rates that will position them to meet future benefits more comfortably. Stronger positions in retirement accounts allow households to stay more comfortably within their appetites for risk.

What’s good for households, though, is not necessarily good for the Federal Reserve. As it meets to consider the future course of monetary policy later this month, it will have to consider the full balance sheet when assessing the impact of what has been done to date. It is safe to say that higher interest rates have been a net negative to the economy, but the boost to investment earnings has blunted the impact of higher borrowing costs.

Those who practice accounting are known for being impartial and dispirited mathematicians. Sources and uses, costs and revenues, assets and liabilities are just ledger entries to some. But for many households and investors, higher rates are a newfound form of goodwill.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust