Measuring, anticipating and controlling the cost of healthcare are all difficult.

I have become more acutely aware of health care costs as the frequency of my visits to clinicians and laboratories has increased. A basic blood workup takes the technician five minutes to initiate and is analyzed by machines. The overall bill: $1,200.

Fortunately for us, insurance covers a significant fraction of this total. But I have periodically wondered how statisticians measure inflation for medical services. Health care is big business in the United States, accounting for 15.7% of personal consumption expenditures (PCE). This is the weight assigned to the sector in the PCE deflator, the Federal Reserve’s favored inflation gauge.

Health care is a much smaller component of the consumer price index (CPI), accounting for just 7.8% of the total. The difference in weights between the two inflation gauges exists because the CPI measures only the costs paid by households (inclusive of insurance premiums), while the PCE deflator includes costs paid on behalf of households by insurers.

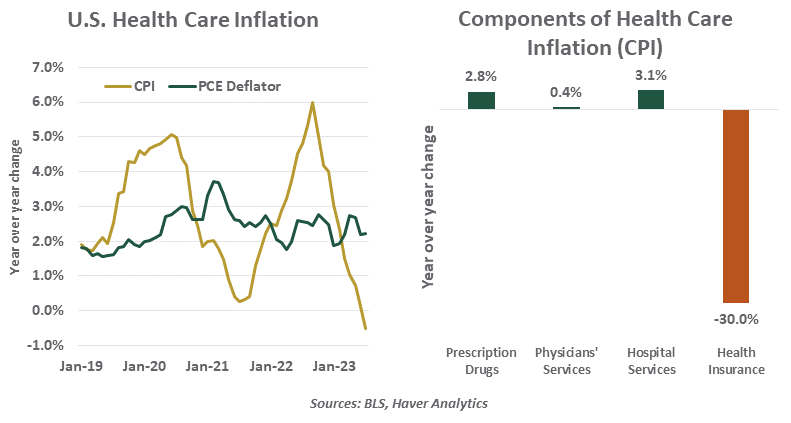

The two approaches produce significantly different paths of health care inflation. The CPI for health care shows considerable amplitude, while the PCE component is steadier. This is due to changing insurance coverage from providers and the selection of different coverage by consumers.

On a year-over-year basis, medical costs in the CPI have declined, contributing to the moderation seen in the overall index. The main contributor is a 30% drop in the CPI’s gauge of health insurance premiums. This is highly counterintuitive, and raises questions about the calculations.

In response, measurement changes to be implemented in October will use a longer averaging period that will change the negative to a positive. The monthly and year over year increases in the CPI will rise as a result.

The situation surrounding medical costs illustrates the difficulty of estimating inflation in health care. Aside from the question at what level measurement should occur, and over what time period, prices have to be adjusted for the quality of the service provided. Changes in therapies, virology, medication, legislation and insurance practices can all have a significant influence. These factors make it very difficult to anticipate and control inflation that emerges from this source.

With health care expected to account for almost 25% of U.S. GDP by midcentury, the influence of this sector on inflation is only going to increase. The quality of our measurement surrounding it needs to keep pace.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust