Why Mexico’s Category 1 Air Safety Status Spells Good News For Investors

Florence, Italy, is one of the most historically consequential cities in history. Known as the birthplace of the Renaissance, Florence is home to some of the most remarkable examples of medieval and Renaissance architecture and art, including the Cathedral of Santa Maria del Fiore and Michaelangelo’s David.

If culture isn’t your thing, you may be interested to learn that the city was instrumental in shaping modern day banking and accounting. The gold florin—first minted in the 13th century in what was then the Republic of Florence, the coin’s namesake—soon became the de facto currency not just in Italy but in all of Europe, establishing the city-state as a major financial hub.

Although not invented in Florence, double-entry bookkeeping was first popularized in the city, most notably by the legendary Medici family. Still in use today, this system, which involves recording both credits and debits for each transaction, allowed for more accurate and transparent accounting. (Triple-entry bookkeeping, which adds cryptography to the mix, wouldn’t arrive until the end of the 20th century.)

The reason I’m sharing this with you is because I visited Florence this week to meet with fellow CEOs, and I was struck by the sheer number of American tourists, many of them with very young children. Even late in the evening on a school night, throngs of American families stood in long lines to enter the Galleria dell’Accademia and Uffizi Gallery.

It’s anecdotal, boots-on-the-ground proof that leisure travel has truly recovered, and I believe air passenger volumes will only continue to climb.

There’s talk that another strong Covid wave will disrupt commercial aviation later this year, but from what I’ve heard, people in general are much more fearful of not being able to travel freely than they are boarding a plane. Most people lost two to three years of travel time; they’re not about to give up on additional opportunities.

Mexico Upgraded To Category 1, Opening Doors For New Routes And Partnerships

In a significant turnaround for its aviation sector, Mexico’s air safety rating was upgraded from Category 2 back to Category 1 by the Federal Aviation Administration (FAA), the agency announced this week.

The reinstatement comes after a costly two-year downgrade that restricted Mexico’s airline growth and led to losses exceeding $1 billion for the industry.

For investors watching the aviation space, this upgrade could be a game-changer, offering opportunities for both Mexican airlines and their U.S. joint venture partners. I believe the recent rise in oil prices, which has put pressure on airline stocks, has also created an attractive buying opportunity.

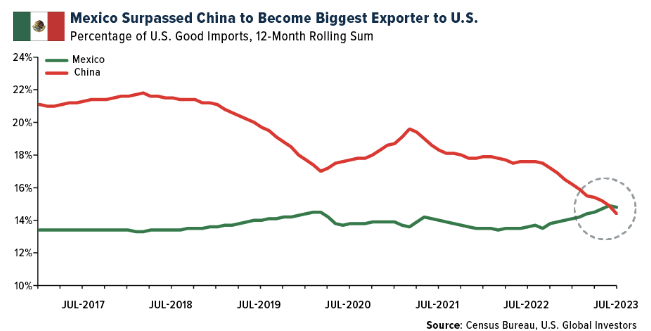

The upgrade to Category 1 is a watershed moment for the Mexican airline industry. This status allows Mexican carriers to add new routes to the U.S., a significant benefit given the Central American country’s status as the leading exporter to the U.S., displacing China.

Beyond opening up new routes, the upgrade is a green light for American airlines engaged in joint ventures with Mexican carriers. Volaris, which had been constrained by the Category 2 rating, can now expand its U.S. network, a development that should also make it more attractive to investors.

Delta Air Lines, with its joint venture with Mexican flagship carrier Aeroméxico, is another beneficiary, especially as Aeroméxico plans to go public in the U.S. after delisting from the Mexican stock exchange late last year. Ultra-low-cost carrier (ULCC) Allegiant Air also stands to gain, thanks to its proposed partnership with Viva Aerobus, currently being reviewed by the Department of Transportation (DOT).

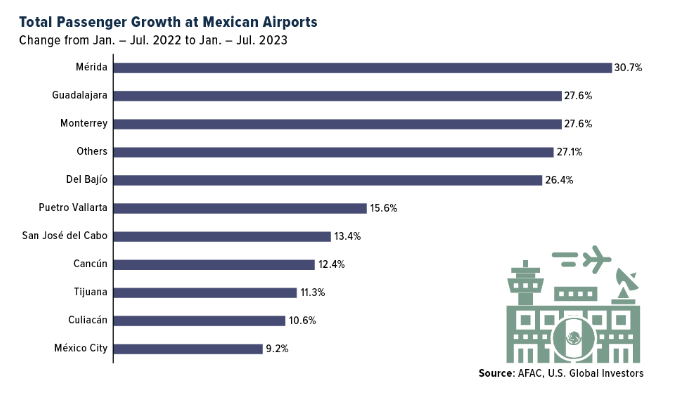

Despite an array of challenges ranging from safety issues to infrastructural vulnerabilities, Mexico’s top three airlines—Aeroméxico, Viva Aerobus and Volaris—registered a collective 16.5% increase in passenger numbers in the first half of 2023 compared to the same period last year.

This growth isn’t that surprising, considering that air travel is increasingly replacing long-distance bus, car and train journeys in Mexico, the number one overseas destination for Americans. Each airline has found its niche—Volaris caters to leisure routes, Aeroméxico targets business travelers and Viva focuses on converting bus passengers to airline customers.

Investment Opportunities In The Airline Sector

Investors have several compelling reasons to look closely at Mexican airlines.

First, the reinstatement to Category 1 status makes these stocks an attractive proposition for market growth and increased revenue. The designation has already had an impact, with U.S.-traded shares of Volaris closing last Friday’s session up more than 12%, its best day since January.

Even before the status upgrade, Aeroméxico was experiencing strong demand in European markets, capitalizing on its unique position as Mexico’s only long-haul operator. According to data from the Centre for Aviation (CAPA) and the Official Airline Guide (OAG), 65% of the airline’s available seat kilometers (ASKs) are from international operations.

Speaking of Europe, passenger volumes at airports were 97% of pre-pandemic levels in July, according to the latest report by Airports Council International (ACI). London Heathrow was the month’s busiest airport, serving over 7.7 million passengers, followed by Istanbul Airport (7.4 million passengers) and Paris Charles de Gaulle Airport (6.6 million).

For those considering diversified options, American partners of Mexican carriers also present investment opportunities. With global air traffic nearly returning to pre-pandemic levels and Latin American airlines experiencing a more than 25% increase in traffic between July 2022 and July 2023, the industry looks set for an upswing.

The Double-Edged Sword Of Rising Oil Prices

I would be remiss if I didn’t address rising oil prices in the context of airline stocks. Brent oil has climbed to over $93 per barrel since June, with the rise attributed to supply cuts and rebounding demand.

In the past, the immediate market reaction to rising oil prices has included a selloff of aviation names. This could lead to overselling, providing an opportunity for investors to buy shares at a lower cost with the expectation that they will rebound—just as they did during the pandemic.

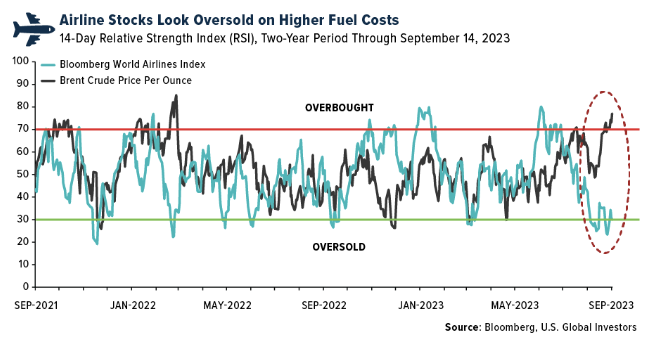

Indeed, global airline stocks look oversold right now, with the Bloomberg World Airlines Index below 30 on the 14-day relative strength index (RSI), compared to oil prices, which are safely in overbought territory. Now could be an attractive entry point for airlines as we await mean reversion to take place.

However, both the Organization of Petroleum Exporting Countries (OPEC), which turned 63 years old this week, and the International Energy Agency (IEA) predict continued supply shortages. Starting this month, “the loss of OPEC+ production, led by Saudi Arabia, will drive a significant supply shortfall through the fourth quarter,” the IEA writes, adding that a rollback to the cuts at the beginning of next year “would shift the balance to a surplus,” which would be good news for airlines.

Discover the top performing airline stocks in 2023 so far! Watch the YouTube video here.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.12%. The S&P 500 Stock Index fell 0.20%, while the Nasdaq Composite fell 0.39%. The Russell 2000 small capitalization index lost 0.41% this week.

- The Hang Seng Composite gained 0.73% this week; while Taiwan was up 2.08% and the KOSPI rose 2.10%.

- The 10-year Treasury bond yield rose 6 basis points to 4.329%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Hawaiian Air, up 4.70%. Shares of Spirit Airlines climbed after JetBlue, which has agreed to buy the company, said it plans to divest some assets in a bid to overcome antitrust scrutiny of the budget airline combination. Spirit stock rose almost 13% to $17.57, but shares are down 10% so far this year.

- According to Morgan Stanley, shipping activity bottomed out in January–March, and volume is currently recovering, especially for European and U.S. routes. Freight rates are rebounding for North American routes but are holding flat for other routes (rates are down about 80% from peak levels and up about 20% compared with pre-Covid levels).

- JetBlue Airways Corp. agreed to transfer some Spirit Airlines Inc. gates and flight slots at three airports to help lessen antitrust concerns over its pending acquisition of the low-cost carrier. JetBlue will shift all of Spirit’s holdings at Boston Logan International and Newark Liberty International and part of its assets at Fort Lauderdale-Hollywood International in Florida to Allegiant Travel Co., according to a statement Monday.

Weaknesses

- The worst performing airline stock for the week was Frontier, down 7.80%. According to Bank of America, following the first negative weekly datapoint since mid-2021 for international leisure sales, the channel’s data further decelerated this week, with net sales down 5.3% versus down 1.8% last week. International volumes fell 2.5% compared to down 1.5% last week and only the fourth negative week all year. Domestic leisure sales also decelerated, albeit far more modestly, down 6.9% compared to down 6.6% last week.

- According to Alphaliner, the six European and American ports featured in the Top 30 ranking of major container ports showed across-the-board declines in throughput in the first half of the year, as the impact of economic contraction in the west took effect. Despite recent export softness, China reported a very strong half year: total volumes processed across the country’s ports reached 149.2 million tons, a rise of 4.8%.

- American Airlines published an investor update lowering its September-quarter EPS outlook to $0.20 to $0.30 from $0.85 to $0.95 due to higher fuel, labor costs (previously announced), and unit revenue coming in at the lower end of prior expectations. The midpoint of its new EPS guidance is beneath the FactSet consensus heading into the print of $0.69.

Opportunities

- According to ISI, based on current airline scheduling data, third quarter 2023 capacity is scheduled up 12% year-over-year. Fourth quarter planned capacity is up 13% year-over-year. Compared to 2019, third and fourth quarter capacity is up 4% and up 8%, respectively.

- DSV announced a strategic partnership with Qatar Airways Cargo, enhancing North America’s connectivity to the Middle East while strengthening service offerings to the oil and gas industry. Through this collaboration, DSV introduces a new route to its air freight charter network that significantly bolsters access to the Middle East and beyond.

- According to Bank of America, the Qantas buyback provides some near-term support, but the road to re-rating depends on Qantas showing stronger-for-longer demand at its trading update later this year, and a gradual de-escalation of regulatory issues ahead.

Threats

- Three top American Airlines Group Inc. global corporate sales executives are leaving the carrier after it finished a dismantling of the team that began earlier this year, shifting its remaining functions and workers to other departments. The moves are linked to American’s shift to direct dealings with corporate business customers instead of going through travel agencies or travel management companies.

- According to the UPS CFO, current third quarter 2023 expectations are far too high owing to the volume challenges leading up to the labor deal and a first-year cost impact that is approximately $500 million above management projections.

- According to Bank of America, Hawaiian Air lowered capacity by 450 basis points each month from November to February. Cuts primarily impacted Japanese flying while there were also modest reductions to interisland and west coast flying. The reductions do not seem to be directly related to the Maui wildfires; however, west coast reductions could be related to the GTF engine recall.

Luxury Goods And International Markets

Strengths

- Lamborghini, a unit of Volkswagen AG, is heading for record sales in South Korea. The company sold 403 cars last year in the country, making it the brand’s eighth-largest market, according to new registration data from the Korea Automobile Importers & Distribution Association. Through the end of August, Lamborghini sold 267 cars, a 19% increase from a year earlier.

- China published better-than-forecasted economic data. Industrial production increased 4.5% on a year-over-year basis versus consensus which was calling for an increase of 3.9%. Retail sales are up 4.6% year-over-year versus consensus of positive 3.0%. The unemployment rate declined to 5.2% in August from 5.3% in the prior month.

- Faraday Future Intelligence, an EV maker, was the best performing S&P Global Luxury stock this week, gaining 35.9% in the past five days. The company has been the weakest performer over the past few consecutive weeks, but shares bounced this week after the company announced the delivery of another long-awaited FF91 2.0 car.

Weaknesses

- Eurozone industrial production missed expectations. Month-over-month industrial production declined 1.1% versus the expected correction of 0.7%. On a year-over-year basis, production was down 2.2% versus consensus of a 0.3% drop. Most of the decline in production was attributed to a larger fall in Germany and Ireland.

- On a year-over-year basis, inflation in the United States increased to 3.7% in August from 3.2% in July. Bloomberg economists were expecting a slightly lower reading at 3.6%. On a month-over-month basis, inflation spiked to 0.6% from 0.2% (in line with consensus).

- Farfetch Ltd., a specialty online retailer, was the worst performing S&P Global Luxury stock, losing 12.5% in the past five days. Wells Fargo analyst Ike Boruchow lowered the firm’s price target to $13 from $18 to account for a greater near-term execution risk and weaker fundamentals, according to Bloomberg. However, the firm kept an “overweight” rating on the stock and shares closed at $2.31 on Friday.

Opportunities

- Another luxury ETF started trading in the United States, making a total of three exchange-traded funds available to investors. KraneShares launched the KraneShares Global Luxury Index ETF (KLXY) last Thursday, aiming to cash in on the rising sales of luxury goods. The fund idea came from KraneShares’ founder Jonathan Krane who spotted the pickup in global travel and a new wave of luxury consumption post-Covid.

- Apple announced a new smartwatch that is described as a major environmental milestone for the company. The new Apple Watch Series 9 and a second-generation version of the high-end Ultra model are manufactured with clean energy and use an eco-friendly band. The new watches will use a faster S9 chip, and it comes in three colors (pink, gold, and black). Series 9 will start at $399, and the Ultra version has a price tag of $799.

- China provided more stimulus to support economic growth and remains committed to better supporting key areas and weak links. The PBOC announced a 25-basis points reserve rate requirement (RRR) for banks, effective Friday, except those that have implemented a 5% reserve ratio. The bank injected more cash into the interbank market while keeping the 1-year medium lending facility rate unchanged at 2.5%.

Threats

- The European Central Bank (ECB) hiked rates by 25 basis points, raising the main refinancing rate to 4.50%, the lending facility rate to 4.75%, and the deposit facility rate to 4.00%. The Eurozone’s inflation slowed to 5.3% on a year-over-year basis in August, but that’s still way above the ECB’s 2% target. With energy prices now rising again, the bank’s latest projections show headline inflation slowing to 3.2% in 2024, versus its prior 3.0% forecast. This week’s hike in Europe threatens to deepen and lengthen recession in the region and worsen the hit to euro bloc company earnings, Piper Sandler commented.

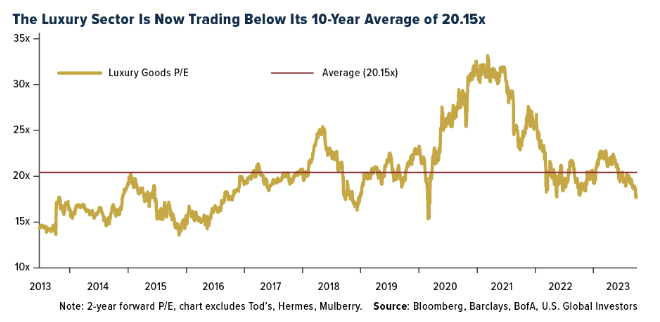

- Barclays’ luxury research team turned more cautious on luxury goods due to expectations that China will further disappoint. The company downgraded the luxury sector to neutral from positive and cut Louis Vuitton’s (LVMH) rating to equal weight from overweight while maintaining overweight ratings on Hermes, Moncler, Prada, and Richemont. According to the group’s research, the luxury sector is now trading below its 10-year average of 20.15 times price-to-earnings.

- Deutsche Bank’s European equity strategists downgraded consumer products to underweight because of the luxury companies’ exposure to China, where growth is slowing down, and corporate defaults are on the rise. The luxury goods sector has been going through a severe de-rating over the past month, the broker said, and the third quarter reporting season may be disappointing.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was uranium, rising 10.28%, as demand for nuclear fuel is rebounding. Copper steadied as a stronger dollar countered a move by China’s central bank to bolster stimulus efforts. The greenback rose after a slew of U.S. data, including producer prices and retail sales, pointed to persistent inflationary pressures in the economy.

- European natural gas prices rose for a third straight session as strikes continue at key export sites in Australia and Norway struggles to exit lengthy maintenance

measures. Benchmark futures gained as much as 9.8% on Monday after workers began partial strikes late last week, threatening operations that supplied about 7% of the world’s liquefied natural gas in 2022. - According to RBC, uranium prices rose for a ninth consecutive week, as recent supply challenges remain top-of-mind along with steady demand interest from investors and utilities. Last week, the annual World Nuclear Symposium in London was held, where nuclear’ s role in the transition to clean energy was highlighted by a positive and constructive tone, while acknowledging there remain hurdles including regulatory and financial limitations. On the geopolitical front, the Niger coup has resulted in sanctions which have created logistical bottlenecks, and stalled uranium processing operations at Orano, a French supplier, although the mine remains operational.

Weaknesses

- The worst performing commodity for the week was soybeans, dropping 1.80%, as U.S. inventories increased. According to Bank of America, cobalt prices have gone full circle twice in the past six years, finding a bottom again this summer, after dropping by 66%. A closer look at supply and demand growth highlights a gap between the two metrics: an acceleration in production has pushed the market into surplus and it looks to remain oversupplied in 2024 too. Almost all the supply additions are coming through in the Democratic Republic of Congo, the mainstay of the cobalt market, and in Indonesia, which has been put on the cobalt map by China’s miners.

- According to JPMorgan, gasoline built for the second time in six weeks (5.6 mm bbls below 2015-19 average inventory levels), and diesel built for the fifth straight week (24.9mm bbls below 2015-19 average inventory levels). On a four-week moving average basis compared with 2015-19, gasoline demand was -6.3% (last week -5.6%) and diesel demand was -2.8% (last week -4.0%).

- The U.S. steel price correction that began in mid-April, continued through the third quarter of 2023. Spot steel prices currently range between $650-$730 per ton. Spot buying activity decreased as buyers continued to focus on managing inventories. Though domestic production declined for three consecutive weeks and lead times rebounded modestly from lows in late-August, spot remained under pressure given the threat of an automotive strike.

Opportunities

- Lithium Americas shares rose, after research and media reports suggest that the company’s Thacker Pass project is located on a U.S. lithium deposit that could be

among the largest in the world. - According to Morgan Stanley, for energy stocks, over the past six months, 2024 EBITDA estimates for the sector have declined by 10%, bottoming in early August before starting to recover modestly in recent weeks. With the 2024 strip rallying sharply since mid-summer, the group now sees 6% upside to next year’s consensus estimates for the oil-weighted coverage at ~$80/bbl WTI. For gas, at $3.50 Henry Hub, Morgan Stanley sees 5% upside to consensus estimates.

- According to ISI, the DOE recently released its 2023 reports on the land-based wind market, offshore wind energy, and distributed wind energy, confirming not only a great 2022 in the U.S. wind power sector (both in terms of new capacity installed and capital investments), but also reaffirmed its expectations that the sector will continue strengthening in the upcoming years.

Threats

- Chevron was unable to reach an agreement with unions after several meetings with the Fair Work Commission, as the unions’ terms were significantly above the market, Reuters reported. Workers began short strikes at Chevron’s Gorgon and Wheatstone LNG facilities and will begin two weeks of 24-hour strikes.

- According to Global Markets Weekly, the historically close correlation between copper and macro indicators like PMIs or CNY has broken down. Indeed, these two metrics suggest the red metal should be trading around 30% below current levels. Green demand in China, (i.e., investment in renewables and electric vehicle production), has been strong. Beyond that, supply growth has been constrained: only 1 of the 10 largest copper producers have raised 2023 production guidance.

- According to Goldman, the risk that strikes at Australian LNG export facilities impact LNG supply, (which has lent significant support to global gas market volatility), has also lent support to coal prices. Goldman believes Newcastle coal prices – and the resulting wider Newc-API2 spread – have overshot fundamentals and have downside from current levels.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was TOMI, rising 30.13%.

- Brevan Howard Asset Management is predicting a potential boom in digital assets similar to what the internet has seen in the past couple of decades and is looking to make “disproportionate returns,” according to an article published by Bloomberg.

- What’s good for equity investors appears to be beneficial again for cryptocurrency enthusiasts, with Bitcoin rebuilding its correlation with technology stocks. After a breakdown in the directional relationship between the two asset classes in June, Bitcoin is back to mirroring the price moves of the surging Nasdaq 100 Index, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was APE, down 16.64%.

- Binance.US CEO Brian Shroder has left the crypto trading platform and has been replaced on an interim basis by the company’s Chief Legal Officer. The company is eliminating about one third of its workforce, writes Bloomberg.

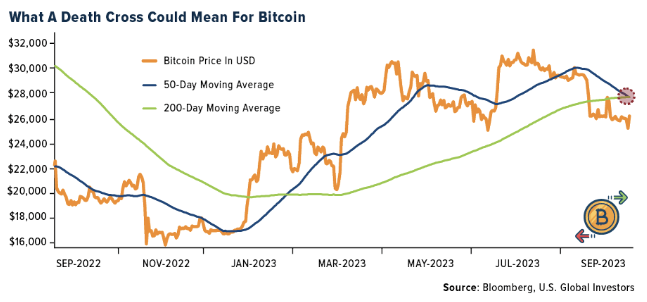

- Bitcoin’s 50-day moving average crossed below its 200-day moving average this week, forming what is known as a “death cross” in the technical world. This is a bearish technical indicator and points to Bitcoin prices potentially heading lower.

Opportunities

- Former Goldman Sachs Group managing director Javier Rodriguez is joining XBTO, the crypto investment firm that’s the jersey sponsor for football superstar Lionel Messi’s new team Inter Miami. His role will include overseeing XBTO’s expansion into new products and asset management strategies, writes Bloomberg.

- Kasikorn Bank, Thailand’s second-largest bank by assets, has launched a $100 million fund to invest in Web3 and artificial intelligence startups. The fund has been set up by KBank’s tech arm, according to Bloomberg.

- Deutsche Bank AG is one step closer to launching a digital assets custody service after finalizing a deal with Swiss crypto technology firm Taurus SA. The bank will use the startup’s technology for providing custody and tokenization services, the two firms said as reported by Bloomberg.

Threats

- Singapore’s central bank imposed nine-year prohibition orders on Su Zhu and Kyle Davies for transgressions at their collapsed crypto hedge fund Three Arrows. The orders from the city’s financial watchdog took effect Wednesday and ban both men from any regulated activity, according to Bloomberg.

- The CFTC’s enforcement director called unregulated decentralized finance exchanges an “obvious threat” in recent remarks following the agency’s charges against a trio of Defi protocols last week, writes Bloomberg.

- Coinbase Global’s volumes and the price of Bitcoin could be decoupling, according to Mizuho’s Dan Doley, pushing the underperform-rated analyst to question if the stock’s 128% rally this year is sustainable, reports Bloomberg.

Gold Market

This week gold futures closed at $1,944.50, up $16.20 per ounce, or 0.84%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.31%. The S&P/TSX Venture Index came in up 1.24%. The U.S. Trade-Weighted Dollar rose 0.22%.

Strengths

- The best performing precious metal for the week was palladium, up 4.88%, due to some short covering that occurred by hedge funds. Gold in China is trading at a record premium to international prices, a sign of Beijing’s escalating battle to defend its currency. Bullion on the Shanghai Gold Exchange traded at a premium of more than $90 an ounce on Wednesday, according to calculations by Bloomberg. That’s the highest since the exchange was founded over two decades ago, as a weak yuan drove up prices in recent weeks.

- According to BMO, Pan African reported its fiscal year 2023 financial results with costs in line and a slight beat on earnings driven by higher revenue. While the 2024 production guidance was announced earlier, the company provided costs and capital outlook with slightly higher AISC, but overall lower total capital spend.

- According to Morgan Stanley, the value of rough lab grown diamond imports increased by 16%-20% month-over-month (MoM) and year-over-year (YoY) and came in above the three-year high. At the same time, polished exports came in above three-year average and increased MoM (but down YoY). This suggests that lab-grown diamonds are gaining market share both at mid-stream and end markets.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 0.16%, as the precious metal suffered a technical breakdown and selling occurred. Exchange-traded funds cut 64,945 troy ounces of gold from their holdings, bringing this year’s net sales to 4.58 million ounces, according to data compiled by Bloomberg. This was the longest losing streak since August 9.

- Azerbaijan produced 1,376 kg of gold in the first eight months of 2023, down 30% from a year earlier, according to data published on State Statistics Committee website. Silver production in January to August declined 41% year-over-year to 2,717 kg.

- Gold retreated to the lowest level in more than two weeks after a breach of key technical support sparked selling. The metal’s slide extended after the spot price broke below its 200-day moving average of about $1,920 an ounce amid high volume in Comex futures.

Opportunities

- According to UBS, SSR Mining remains one of the group’s preferred gold picks for its free cash flow generation driven by modest growth capex and attractive margins versus peers. A strong second-half CY23 of 400,000 ounces gold should get it to the bottom end of guidance of 700,000-780,000 ounces gold at $1,365-$1,425 per ounce, which remains on track. In a sign of its strength, it recently announced a new buy-back of up to 10.2 million shares (5% of outstanding).

- According to RBC, gold producers have been challenged by considerable cost inflation and margin pressures, with senior producer costs rising 10% in 2022 and a further 8% estimated in 2023. However, RBC forecasts declining headwinds into 2024, with senior producer costs forecast to decline 2% year-over-year, but the group does note these estimates are currently 5% above consensus.

- Gold imports by India, the world’s second-biggest consumer of the yellow metal, surged about 40% in August on strong festival buying, a person familiar with the matter said, threatening to blow out the trade deficit that has already been high due to rising oil prices.

Threats

- RBC Global Mining Equities now incorporates gold price assumptions of $1,960 per ounce in 2024 and $1,975 per ounce in 2025. The group updated its long-term gold price forecast to $1,700 per ounce and has increased the base discount rate assumptions for producers to 8% from the conventional 5%. The net impact of these changes has resulted in a median NAV changing by -2% and median EBITDA over 2023-2025 changing by positive 23%.

- The Biden administration is recommending changes to a 151-year-old law that governs mining for copper, gold, and other hard rock minerals on U.S.-owned lands, including making companies for the first time pay royalties on what they extract. A plan led by the Interior Department also calls for the creation of a mine

leasing system and coordination of permitting efforts among a range of federal

agencies. This comes as the White House has been pushing to boost domestic

mining for minerals needed for electric vehicles, solar panels and other clean

energy. - According to Morgan Stanley, India August trade data suggests that mid-stream diamond inventories continue to build while market share loss to lab-grown stones persists. Declines in polished prices intensified in August with Rapaport pointing to cuts of 2%-9% for 0.3-3 carat stones.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2023):

JetBlue

Allegiant Travel Co.

American Airlines

Qantas Airways

Boeing Co/The

Hawaiian Air

Volkswagen

LVMH Moet Hennesy

Hermes

Moncler

Prada

Richemont

Delta Air Lines Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Nasdaq-100 is a stock market index made up of 101 equity securities issued by 100 of the largest non-financial companies listed on the Nasdaq stock exchange.

The Bloomberg World Airlines Index is a capitalization-weighted index of the leading airlines stocks in the World.

The Relative Strength Index (RSI) is a momentum indicator that measures the magnitude of recent price changes to analyze overbought or oversold conditions.

Mean reversion is a financial term for the assumption that an asset’s price will tend to converge to the average price over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.