Fed Preview: Done, Or More To Be Done?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe FOMC will make some close calls and tough decisions.

We’ve had a vigorous debate within the Economics Department over whether the Federal Reserve has reached the end of its tightening cycle. While there is consensus that interest rates will be left unchanged at the Federal Open Market Committee (FOMC) meeting next week, opinions diverge from there.

Debating points on each side of the areas critical to the Fed’s decision are enumerated below.

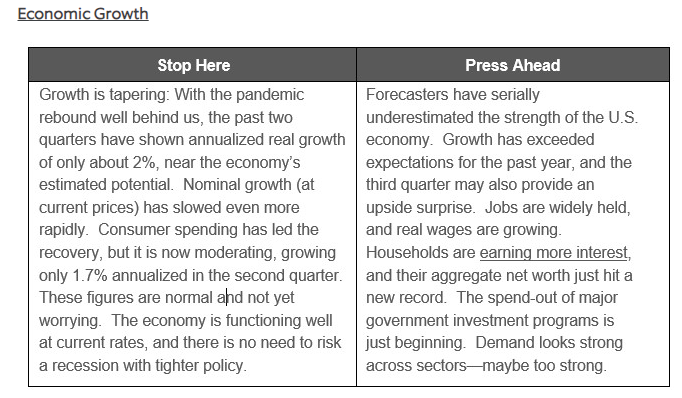

History is crucial to the study of economics, which has offered little reason for economists to be optimistic in this cycle. Corrections to high inflation have almost always been brought about by a recession.

It is dangerous to explain why today’s situation might be different, but so much about the pandemic and recovery cycles have been without historical parallels. We can’t yet say the soft landing has happened, but the longer it remains a possibility, the more plausible it becomes.

The Federal Reserve does not have a mandate to grow the economy in perpetuity. Cycles are natural, and Fed speakers have stated they would rather suffer the cost of a recession than leave inflation on an uncontrolled trajectory. Recent upside surprises to growth could cut both ways. Dovish governors may want to try to stick the soft landing, while more hawkish members may believe they have not gone far enough, and the economy can handle higher rates.

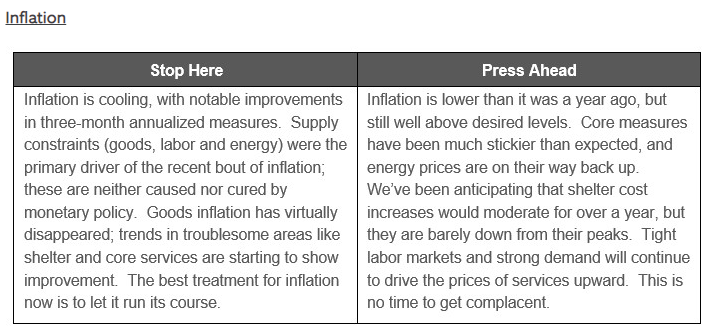

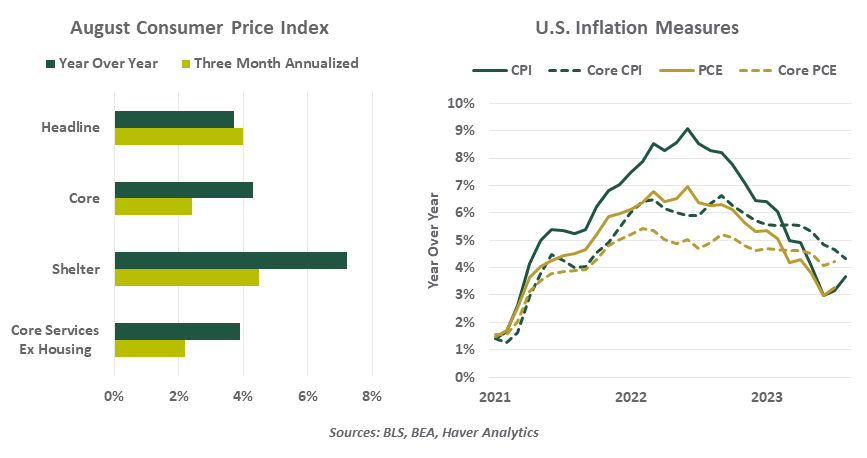

At the annual Jackson Hole Monetary Policy Symposium, Fed Chair Jerome Powell clearly reaffirmed that “Two percent is and will remain our inflation target.” Inflation’s downward trend over the past year is welcome progress, but today’s readings are unacceptably high. The question is whether more policy rate hikes are the appropriate remedy to push inflation down further.

In theory, higher interest rates increase the cost of borrowing, reducing demand as credit becomes more expensive and difficult to obtain. In practice, much demand has proven to be insensitive to interest rates, as consumers and corporations were cash-rich or locked in low interest rates while they were still available. A further hike would serve more as a signal of the Fed’s resolution to fight inflation, helping to tame expectations, than a concrete step to contain actual prices.

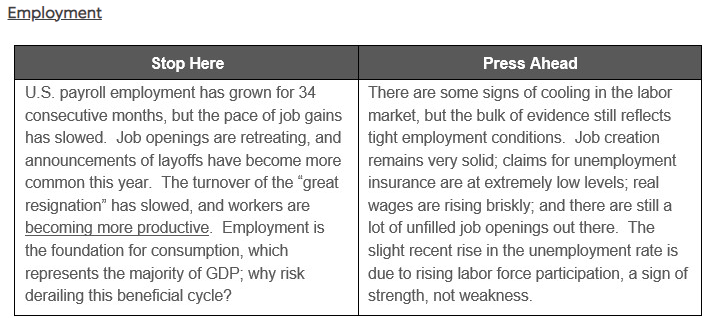

The Federal Open Market Committee has been able to focus singularly on inflation because the labor market has presented no cause for worry. Steady job creation and an unemployment rate hovering below 4% are optimal outcomes. Central bankers would not seek to achieve higher unemployment as a policy goal, but rather, accept it as a consequence of actions to keep the economy from overheating.

Wage gains are holding above the level that was formerly considered normal, which remains an inflationary risk (especially for prices of services). Workers welcome higher wages, but managers fret about the higher cost, which may flow through to final prices. Policy makers will want to prevent a wage-price spiral from taking root: thus far, one has not emerged, but the fear of this difficult scenario may push the FOMC toward higher rates as a precaution.

The long and variable lags of monetary policy remain a cloud on the horizon. Will the chill in bank lending spread to other sectors that remain active? Or will banks regain their footing without a broader market slowdown? Markets have endured several events that carried systemic risk over the past year, from the gilt crisis to a crypto collapse to Silicon Valley Bank. If one accepts the old maxim that “the Fed hikes until something breaks,” the breaks have thus far been manageable.

On balance, we anticipate no rate change next week, but one final hike before year-end. Once this Fed resolved to combat inflation, its decisions have been rapid, erring on the side of tightening. The end of the cycle is in sight, and we expect a hike to cement the tightening posture into 2024.

Our conversations are now turning to the timing and pace of eventual rate cuts. We anticipate slower inflation will allow the Fed to begin gradual rate reductions in mid-2024. Here again, there is no historical playbook for gradual cuts. The updated Summary of Economic Projections, released as part of the FOMC materials, will offer clues for how individual governors are contemplating the path to neutral.

Powell summarized his Jackson Hole speech by revisiting the theme of stars: “We are navigating by the stars under cloudy skies.” We are encouraged that the voyage has carried on so well, despite unclear conditions.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Equities are essential portfolio building blocks. Join VettaFi for the Equity symposium.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All