Evidence of China's slowdown is appearing in unexpected places.

I recall a long-ago discussion with an older man who grew up in Germany during the nation’s postwar reconstruction. He recalled fond feelings among his generation for the United States: “Everything good was made in America! The music, the cars, the movies, the moon landing!” While our nation faces more competition for our tangible and cultural exports, one export has remained in high demand: U.S. Treasury instruments.

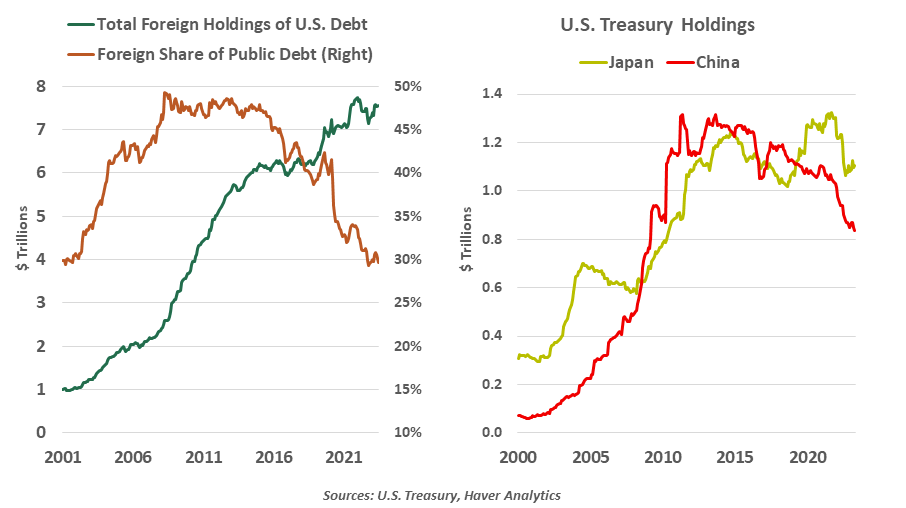

Each month, the U.S. Treasury updates its International Capital (TIC) reports of cross-border financial flows, including a report of foreign holdings of U.S. debt. Through June, TIC shows an overall steady demand for sovereign debt, but with a shifting composition.

The role of foreign holdings can be a subject of hyperbole, suggesting that the U.S. has compromised its autonomy by being in debt to other nations. That is an overstatement and an oversimplification. Nations hold foreign-denominated assets as buffers against currency fluctuations and to support international trade. The U.S runs a trade deficit; dollars are exported in exchange for imported goods. The nation’s debt instruments are the standard for risk-free assets, and the U.S. dollar is the world’s reserve currency, creating more incentive to amass dollar assets. And the TIC summaries list only the location of the holder of the debt. Asset owners are split roughly 50-50 between official and private sector investments. The potential that these holdings might be used for political purposes is very low.

The tactical purpose of foreign holdings explains why they have held fairly steady through an interval of active fiscal policy. COVID interventions ballooned total U.S. publicly-held debt by nearly 50%, from $17.2 trillion in January 2020 to $25.5 trillion in June of this year. Over that same interval, total foreign holdings did not increase proportionately, growing by only $536 billion (+7.6%). This new tranche of debt was largely absorbed by the Federal Reserve and other domestic buyers.

Foreign holdings peaked at 49% of debt held by the public in April 2008, as demand for safe U.S. Treasuries increased amid global credit stress. That share fell as U.S. debt issuance grew. Top holders of U.S. government debt include Japan, China and financial centers like the United Kingdom, Luxembourg, Switzerland and the Cayman Islands.

China supplanted Japan as the largest foreign holder of U.S. debt in 2008, reaching a peak of $1.3 trillion in 2013. At the time, this represented over 10% of U.S. debt held by the public. China has gradually reduced its ownership of U.S. Treasuries, ceding the title of top sovereign holder to Japan in 2019.

Of late, China’s holdings of Treasury debt have declined more rapidly. As of June, they hold $835 billion, an 11% decline from a year before. This is a rapid turnabout. Through much of China’s ascendancy, its government purchased foreign assets to support its growth and weaken its currency, supporting exports. Now, in a push against dollar dominance and in light of its more recent myriad stresses, the nation has shifted to a posture of selling dollars to buy yuan, to keep the currency from devaluing further.

Japan has also decreased its holdings by 10% in the past year. In Japan’s case, the story is more hopeful. The gradual, long-awaited normalization of monetary policy, combined with favorable growth prospects, is increasing domestic demand for yen. An important common thread with China, though, is that each nation’s lower appetite for dollars is driven more by their own circumstances than a perceived counterparty risk with the United States.

Despite these two notable declines, external demand for Treasuries overall is steady. Total balances increased 2% over the past year; two-thirds of the nations reported in TIC data increased their holdings. Rising yields will add to the attractiveness of Treasuries as an asset class, helping to allay any nascent competition for reserve currency status. America’s era of export dominance in goods may be in the past, but we expect the nation’s debt to remain a popular item overseas.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust