When younger folks at the bank (which means almost everyone that I work with) complain about inflation and interest rates, I become a curmudgeon. When I was starting out, I tell them, both quantities were well into the double digits and the phrase “soft landing” hadn’t entered our vocabulary. I close my diatribe by suggesting that their present discomfort is nothing compared to what we old-timers endured way back when.

In recent weeks, I have also overheard partners worrying about the rising cost of energy. I am tempted to cut them off with tales of oil prices rising by ten times during the 1970s, hollowing out American heavy industry and producing a series of painful recessions. But I do have to acknowledge that the recent reversal in energy markets comes at an uncomfortable time. Then, as now, we are struggling with the question of how best to power the economy and how monetary policy should react to supply shocks.

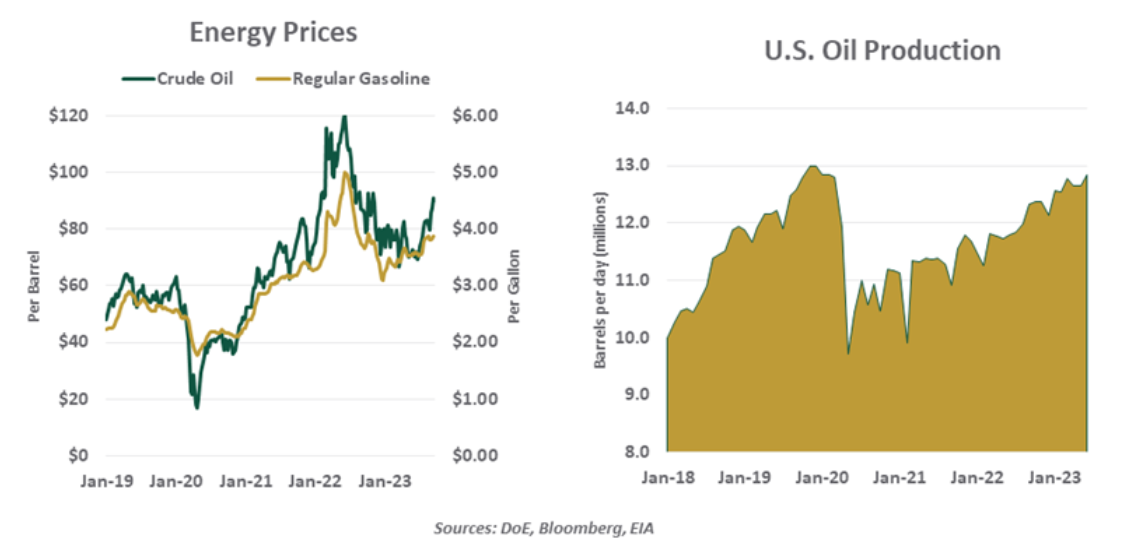

Inflation in the United States, as measured by the year over year change in the consumer price index (CPI), fell by two-thirds between June 2022 and June 2023. The main driver of the decline was energy prices; a barrel of crude oil cost $120 in the summer of last year; twelve months later, it cost $70. Broad measures of energy costs, which include electricity and natural gas, were down by 17% during that interval.

Weakness in global manufacturing was the main driver behind the decline in oil prices. Across countries, purchasing manager’s indexes covering heavy industry are in recessionary territory. China was an exception for a time, as the country emerged from the pandemic. But China’s darkening economic outlook will limit its appetite for oil as we move into 2024.

Witnessing this, oil exporting nations have reduced supply. Worldwide production is more than three million barrels per day lower than it was early this year; Saudi Arabia alone has cut its output by one million barrels per day, a 10% drop. It is estimated that the Saudis need crude to sell for at least $85 per barrel to meet their fiscal targets; prices have soared through that milepost. Some analysts think that $100 per barrel is likely in the near term.

Prior to the pandemic, American oil production stood ready to offset supply cuts elsewhere in the world. But the industry has changed a lot since 2019. The price collapse of three years ago strained the finances of some exploration companies and created losses for those who had extended credit to them. The consequent tightening of financial conditions surrounding the sector made the development of new supplies much more challenging.

Further, the lull in production during 2020-21 encouraged laborers in the oil patch to seek other opportunities. The number of persons employed in oil extraction is still below 2019 levels. And the United States still experiences periodic bottlenecks in refining, the result of capacity constraints.

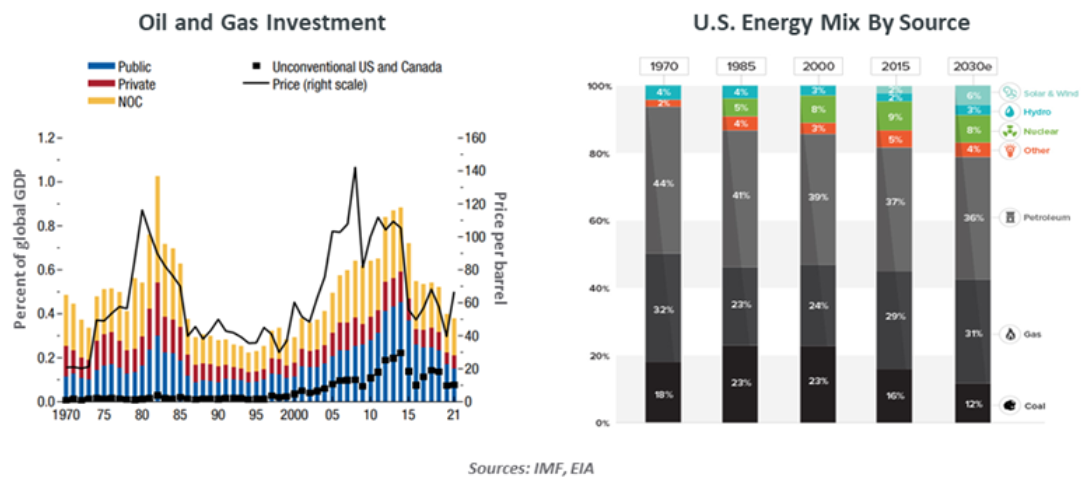

Finally, global investment in oil and gas exploration and production has been declining, limiting the discovery and development of reserves. Volatile demand and prices have certainly contributed to this trend, but the focus on developing alternative energy sources has absorbed a lot of the capital flowing into the sector. Climate change and its influence on governments and investors have been among the drivers of this change of emphasis.

As a result of these factors, American oil production only recently returned to its pre-pandemic levels. The number of active rigs is still 25% below levels seen prior to COVID-19, leaving some reserves untapped. The industry does not have the same flexibility to respond to higher prices as it did four years ago.

To compensate, the White House has authorized substantial releases from its Strategic Petroleum Reserve (SPR). The SPR is 45% smaller than it was at the beginning of 2021; the administration declined to replenish it as oil prices fell, which now appears to be a missed opportunity.

It bears noting that the world will still need significant supplies of traditional fuels even as new sources are developed. Securing those supplies will require investment into the sector. As well, major energy companies are performing research aimed at using traditional fuels more cleanly and efficiently. We’ll need some new discoveries in this arena if we have any hope of bending the carbon curve.

Policy makers and portfolio managers are gaining appreciation of these nuances. We will need an “all of the above” energy strategy in the years ahead.

The descent of inflation this year has given central banks a renewed sense of control and brought interest rate increases close to an end. But the resurgence of oil prices has prompted a rise in overall inflation. Higher petroleum prices will also affect core inflation through their influence on transportation costs and the prices of raw materials like plastics.

Monetary policy is not the best tool for dealing with supply shocks, especially in energy markets. Raising interest rates in the current circumstance may actually be counterproductive, as it would tend to discourage increases in U.S. production that could offset OPEC restrictions. But the price of gasoline is persistently correlated with inflation expectations, which have generally been well-behaved during the current cycle. Central banks would like to keep them that way.

For now, resurgent energy prices may not be enough to prompt more rate increases, but they may contribute to higher for longer monetary policy. Sensing this, bond markets have been correcting; the yield on a 10-year Treasury note has risen by 70 basis points in the past two months.

Today’s energy price surge may not produce the upheaval that we experienced half a century ago. But it raises questions that we first asked back then…and which we have yet to answer satisfactorily. If we are to keep our economy and our environment in reasonable balance, we’ll need to respond well.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust