Higher long-term bond yields will allow the Fed to do less on short rates.

Conversations about the Federal Reserve can be challenging. Those who don't pay close attention to financial markets often ascribe much more power to the central bank than it really has. The only rate the Fed controls is the Fed Funds Rate (FFR), at which banks lend to each other overnight. Shorter-term rates are well correlated with the FFR, but the farther out one goes on the yield curve, the less power the Fed has to steer.

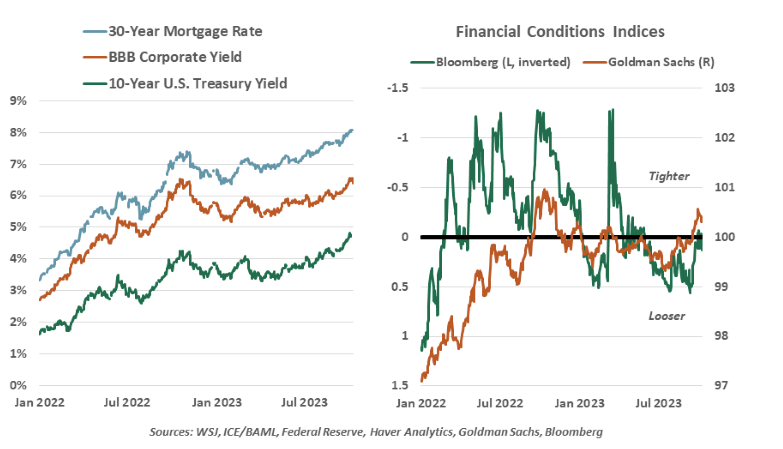

This week brought signs that the recent runup in longer-dated Treasury yields has captured Fed leaders' attention, likely bringing an end to the rate hiking cycle. The yield on the ten-year U.S. Treasury rose from 4.1% at the end of August to a recent high of 4.8%. The salient question has been, what changed?

A higher-for-longer rate outlook has been the conventional wisdom for quite some time. Guidance from the Fed throughout the summer poured cold water on expectations of a rapid monetary policy retreat next year. Treasury issuance has been elevated since the debt ceiling was resolved, but the auctions of new debt have been orderly.

Long term rates are the sum of the yields earned by short term bonds, plus a term premium, the additional compensation to an investor for locking up capital for a longer period. The term premium is not an explicit spread or fee, but rather, an implicit cost set in market transactions. It appears the recent runup has been a function of higher term premia for U.S. Treasury debt.

We need not look far for reasons to understand investor skepticism of U.S. sovereign debt. The nation nearly entered a technical default due to the debt ceiling, prompting a downgrade by Fitch Ratings. A shutdown seemed certain as the fiscal year ended; a last-minute compromise granted a temporary reprieve and has left the lower chamber of Congress leaderless. The nation's long-run fiscal trajectory is on a course for perpetually growing debt and deficits, without easy remedies. Characterizing U.S. Treasuries as a risk-free benchmark is starting to sound a bit optimistic.

Higher policy rates are pushing up the cost of debt for new and variable-rate loans. This debt is usually priced as a spread to a benchmark rate like the Secured Overnight Funding Rate (SOFR, a replacement for LIBOR) or Bank Prime, all of which have climbed since 2022. Though spreads are stable, the absolute rise in rates is a burden for borrowers. The higher rates are serving to meet the Fed's objective of slowing the economy by tightening financial conditions. More hikes to short rates may no longer be needed.

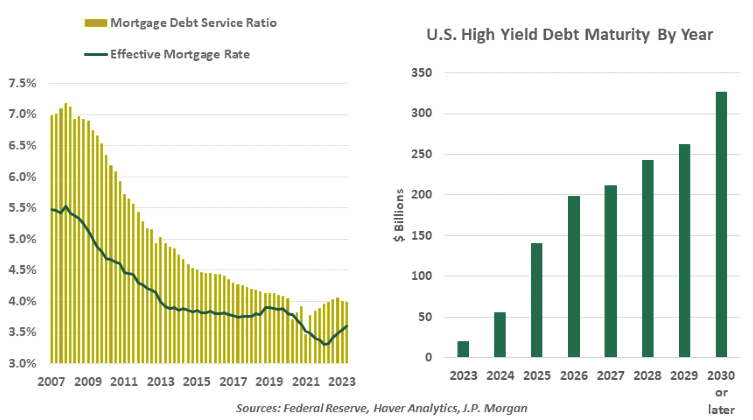

The specific timing of the move in yields is difficult to explain with precision, but it is consistent with the lagged effects of monetary policy. The immediate impact of FFR increases has not been felt by many borrowers. Most homeowners locked in low rates and have avoided the higher cost of mortgage debt; most corporate debt will not come due for several years; owners of older vehicles are avoiding the newly higher cost of auto financing. But rapid policy rate changes and greater uncertainty are becoming clearer in the U.S. Treasury’s cost of borrowing.

This week, Fed leaders offered comments suggesting that higher rates are shifting their outlook. Dallas Federal Reserve Bank President Lorie Logan gave a speech that went into detail about the forces that can move rates, including surveys, term structure models and event studies, concluding that term premiums explain the majority of the rise in yields. Fed Vice Chair Phillip Jefferson said he would “remain cognizant of the tightening in financial conditions through higher bond yields.” Neither speaker indicated a need for more FFR hikes.

Materials from the September meeting of the Federal Open Market Committee reflected a committee split between zero and one more rate hike in the remainder of 2023, before cuts to follow next year. Moves in the market, and recent signals from the Fed, suggest that the cycle has concluded.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust