Targeting Resilient Portfolio Construction With Alternatives

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey points

- As investors face continued macroeconomic and market uncertainty, evolving the 60/40 portfolio of stocks and bonds to include alternative investments may help build portfolio resiliency.

- When selecting alternative investments, investors may want to consider strategies that seek to deliver differentiated portfolio outcomes—like amplifying returns or diversifying risk exposures.

- The complementary risk and liquidity characteristics of liquid alternatives and private assets may make for a balanced and outcome-oriented alternatives allocation.1

The expected comeback of the 60/40 portfolio in the first half of 2023 has taken a pause as stock and bond returns face the pressure of higher yields—a backdrop reminiscent of the historic 60/40 drawdown of 2022. Despite a rising expectation for an economic soft-landing scenario, the range of potential economic outcomes remains broad and highly uncertain. Near-term recession risks have decreased, and expectations for recession have been pushed out into 2024. But the increasingly two-sided risks to a US Federal Reserve (“Fed”) committed to keeping monetary policy tight until price stability is fully restored have become more evident.

What does this backdrop mean for the durability of the 60/40 portfolio as we look ahead? Continued macroeconomic uncertainty threatens to put pressure on asset price returns. For portfolio construction, we see this as the stock and bond return correlation has again turned significantly positive in the second half of the year, with the surge in long-term bond yields driving stock and bond returns lower. This underscores the importance of building resiliency with alternative investments that offer additional sources of diversification and potential return in portfolios.

By (1) identifying strategies that seek to deliver differentiated portfolio outcomes like alpha, or excess returns that are uncorrelated to stock and bond returns, and (2) choosing a combination of strategies that are complementary and tailored to their specific risk, return, and liquidity needs, investors can seek to build an additive and effective allocation to alternatives. In this article, we discuss a framework for screening alternatives and key considerations for constructing an alternatives allocation using strategies across the full spectrum of alternatives ranging from private equity, private credit and liquid alternatives.2

Screening for alternatives that target differentiated portfolio outcomes

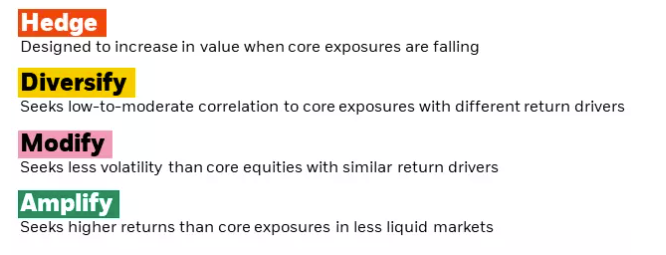

When it comes to selecting alternative investments, there is a wide range of strategies to choose from. The following framework breaks alternatives down into four distinct categories based on the outcomes that they’re designed to provide: hedge, diversify, modify, and amplify.

So how effective are each of these at improving portfolio outcomes? First, it’s important to examine how these types of strategies have behaved over time. Hedges, for example, have a negative beta to traditional asset classes like stocks. This has allowed them to generate returns when used tactically during periods of market declines. But historically, hedges have tended to lose money as markets trend higher over the long run.

Along with the cost of potential portfolio losses, it’s important to determine whether the fees associated with alternatives are justifiable for the value that they deliver. Modifiers move in the same direction as equity markets, but not as significantly. This means that they offer limited upside when broad markets are moving higher, and tend to struggle during equity market drawdowns. In general, they fail to deliver a unique return profile and the exposure that they offer can likely be replicated at a lower cost.

This leaves us with two categories of alternatives that may have the highest potential to provide differentiated outcomes in client portfolios: amplifiers and diversifiers. When carefully selected, these two types of alternatives can be complementary and serve as the foundation of a well-balanced alternatives allocation.

Building a balanced alternatives allocation with amplifiers and diversifiers

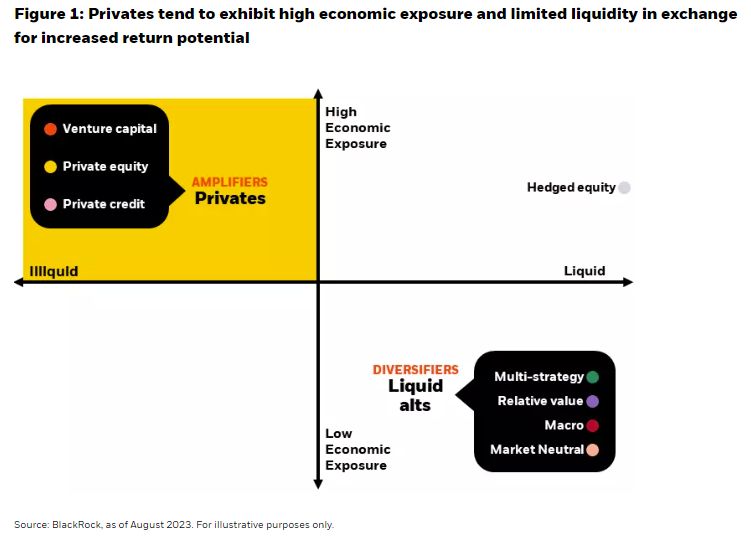

Due to their greater economic exposure and higher business and financial leverage, private assets—both private equity and private credit—tend to exhibit a higher expected return and risk profile compared to publicly traded assets. As a result, they are commonly used as amplifiers in portfolios. The enhanced opportunity set that privates offer has garnered growing investor interest, with more than 36% of US financial advisors surveyed by Cerulli planning to increase private market exposure by 2024.3 When increasing or establishing exposure to private markets, Figure 1 highlights two key considerations to account for—the liquidity profile of privates and the level of economic exposure that they introduce to portfolios.

From a risk factor perspective, private assets tend to exhibit high economic exposure. Why is this important? Returns from traditional asset classes like stocks are also heavily dependent on the direction of economic conditions. This means that private assets may add to existing dominant portfolio risk exposures—potentially reducing overall diversification in exchange for higher returns.

Another important consideration is the liquidity profile of privates. Liquidity constraints on private investments are highly variable, but strategies often come with “lock up” periods, where capital may not be able to be accessed for a significant amount of time once invested—ranging from 5 years, 10 years, or as long as 12 years.4 Some private investments provide more frequent access to liquidity through tender offers which are periods where a limited portion of the strategy’s shares eligible for redemption. But if several investors seek redemptions during the same period, redemption requests may not be completely fulfilled. When allocating to privates, it’s important to consider where they fall on the liquidity spectrum and account for the portion of a client’s overall portfolio that must remain liquid based on future funding requirements.

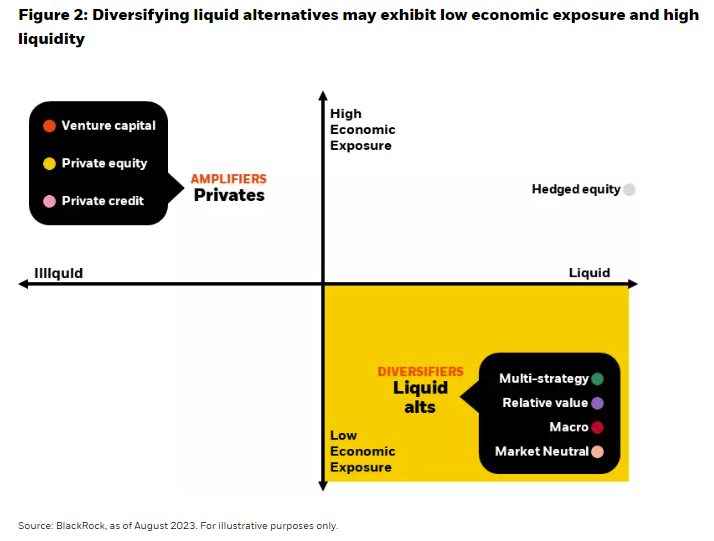

So how can investors balance the need to generate higher returns, diversify portfolio risk exposures, and maintain an adequate liquidity profile? This is where diversifying liquid alternatives can be complementary to private assets as part of an alternatives allocation (Figure 2).

Liquid alternatives with a return objective targeting alpha (excess returns from idiosyncratic exposures) while at the same time limiting or eliminating market, beta, factor and directional exposures may help to balance overall portfolio risk exposures. These types of alternatives can be diversifying because their returns should be primarily driven by risk factors that aren’t closely related to economic and market conditions—and potentially even defensive in nature if their alphas tend to be strongest when economic risk is rising. These exposures can be accessed in a daily liquid mutual fund wrapper as liquid alternatives invest in tradeable securities, but deploy different investment strategies to provide diversification and defensive alpha.

The ability to target a diversifying and defensive return stream is especially important as macroeconomic uncertainty remains elevated. Why? The Fed’s commitment to defeating inflation means that policymakers are less likely to materially cut interest rates in the face of slowing growth. As a result, the degree of diversification that traditional bonds can offer in portfolios may be less reliable than in recent decades of below-target inflation. The defensive alpha in some diversifying liquid alternatives can offer an added source of ballast in portfolios for when risk assets with high economic exposure come under pressure.

Liquid alternatives can seek to take advantage of today’s macroeconomic and market dynamics to generate alpha from idiosyncratic risk while limiting market directional risks. This provides the “plus” in the “cash-plus” return targets of liquid alternatives. Security dispersion, or the difference in returns across individual securities, as well as macro dispersion, or the difference in returns across countries, regions, and instruments tends to rise during periods of market stress and volatility. Liquid alternatives that can take both long and short positions may thrive in these high dispersion environments because they can go long securities that may become outsized winners and go short securities that may become relative losers—targeting returns in the cross-section of markets with reduced dependence on market direction.

It's important to note that liquid alternatives can vary widely and not all strategies are effective at playing the role of a diversifier. And like all investments, liquid alternatives come with inherent risks including potential losses and can be highly correlated with other asset classes like stocks and bonds. When identifying a liquid alternative to diversify portfolio exposures, investors may want to consider strategies that exhibit a low correlation to existing portfolio holdings and market beta factors such as overall stock and bond returns. Additionally, a history of consistent returns across a range of market environments, but especially during market downturns, may characterize defensive alpha strategies.

Seeking to enhance portfolio outcomes with alternatives

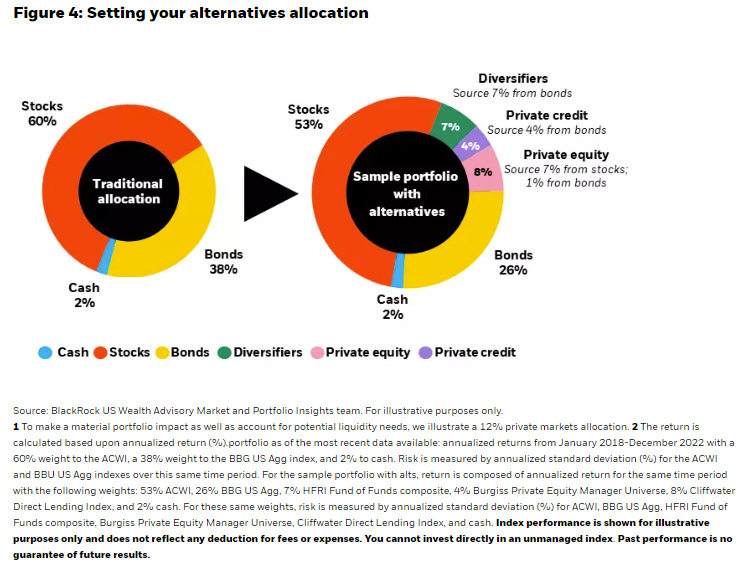

As a starting point for building an alternatives allocation, our colleagues in BlackRock’s US Wealth Advisory Market and Portfolio Insights team designed the portfolio highlighted in Figure 4, adding 12% to amplifiers (private equity and private debt) and 7% to diversifiers from a 60/40 portfolio. They found that over the last 5 years, adding alternatives improved portfolio returns by 1.5% while reducing overall portfolio risk by 0.3%—delivering the intended portfolio outcomes of seeking to amplify returns and diversify risk.

Conclusion

Continued macroeconomic uncertainty makes it more crucial than ever to explore alternative investments that offer differentiated portfolio outcomes. Amplifiers like private assets, are commonly used in portfolios to enhance return potential. Liquid alternatives with diversifying and defensive properties can help balance these amplifiers from both a risk and return and liquidity perspective. When used together, the two may make for a well-rounded alternatives allocation that can help build portfolio resiliency.

1,2 Liquid alternatives are alternative strategies that generally offer daily liquidity by investing in publicly traded securities, but employ different investment strategies to target specific investment outcomes (i.e. lowly correlated returns to stocks and bonds). Private assets refer to alternative investments that offer access to securities that are not publicly traded. This can include private equity (investments made in companies that are not traded on a public stock exchange), and private credit (direct lending to a company).

3 The Cerulli Edge - US Advisor Edition – Trends for 2023 issue, as of January 2023.

4 Source: Prequin, as of September 2022.

Investing involves risks, including possible loss of principal.

Important notes

The Burgiss Private Equity Manager Universe (BMU), contains 5,341 private equity funds (vintages 1978-2022) as of October 2022 with 9/30/22 performance data (most recent performance data available). All vintages were included. All private equity sub-strategies in the BMU were included e.g., Equity Generalist, Equity Venture Capital Generalist, Equity Venture Capital Late Stage, Equity Expansion Capital, Equity Buyout, Equity Venture Capital Early Stage and Unknown as well as Equity Unknown. The BMU reflects quarterly time-weighted returns. The BMU is sourced from quarterly unaudited and annual audited financial statements that private investment fund managers produce for their fund investors. Therefore, there may be survivorship bias given that fund managers have discretion to report, or to discontinue reporting for various reasons (e.g. due to liquidation) and therefore may reflect a bias towards funds with track records of success. To protect the confidentiality of individual funds and their underlying portfolio investments, the published benchmark statistics reports contain only aggregate information. Therefore, the BMU is not transparent and cannot be independently verified given that it does not identify the funds included by name. Private investments in the BMU are typically illiquid. Additionally, any updates to historical data to this data universe, which can include adding a fund and its performance history to the database (“backfills”) and/or updating past information for an existing fund due to late-arriving, updated, or refined information, would be reflected when that group is published for the next performance. The Burgiss Private I Universe Analytics tool recalculates the data each time a new fund is added, therefore the historical performance of the data is not fixed, cannot be replicated, and will differ over time from the data presented in this communication. The BMU is based on data sourced from limited partners of these private funds and calculates results net of fees and carried interest, providing results that are updated and published on a quarterly basis.

The HFRI FOF (Fund of Funds) Composite Index is an equal-weighted index that contains over 400 constituent hedge fund of funds, both domestic and offshore.

The MSCI ACWI Index is designed to represent performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 24 emerging markets.

The MSCI World Small Cap Index is designed to represent performance of the full opportunity set of small-cap stocks across 23 developed.

The U.S. Fund Bank Loan is representative of the Morningstar mutual fund category average.

The Bloomberg U.S. Aggregate Bond Index is representative of the U.S. investment grade taxable bond market.

The Bloomberg U.S. HY 2% Issuer Cap Index is an unmanaged index of the 2% Issuer Cap component of the Barclays High Yield Corporate Bond Index, which is a market value-weighted index of fixed rate, non-investment grade debt.

The Cliffwater Direct Lending Index (CDLI) is an index that assists investors to better understand private credit as an asset class. The CDLI seeks to measure the unlevered, gross of fees performance of U.S. middle market corporate loans, as represented by the underlying assets of Business Development Companies ("BDCs"), including both exchange-traded and unlisted BDCs, subject to certain eligibility criteria. The CDLI is an assetweighted index that is calculated on a quarterly basis using financial statements and other information contained in the U.S. Securities and Exchange Commission ("SEC") filings of all eligible BDCs. Eligibility is set as all assets held by BDCs that (1) are regulated by the SEC as a BDC under the Investment Company Act of 1940; (2) have a substantial majority (approximately 75%) of reported total assets represented by direct loans made to corporate borrowers, as categorized by each BDC and subject to Cliffwater's discretion, and (3) file SEC form 10-Q (or 10-K, as applicable) within 75 (or 90) calendar days following the current Valuation Date. If a BDC meets the eligibility criteria, but has not filed its report on Form 10-K or 10-Q with the SEC at the time the index is reconstituted, asset information from its report will be included in the index at the time of the next reconstitution. This information is derived from sources that are considered reliable, but BlackRock does not guarantee the veracity, currency, completeness or accuracy of this information. The Cliffwater Direct Lending Index (CDLI) is included within this document to demonstrate how private markets perform differently from public markets during the same time period. Note that the indices contain several differences in the way that they are calculated, including the following, and therefore may not represent a fully accurate representation of the private/public credit market. The CDLI is an asset-weighted index based off of quarterly SEC filings required of BDCs, whose primary asset holdings are U.S. middle market corporate loans. SEC filing and transparency requirements eliminate common biases of survivorship and self-selection. The index returns are generally published 75 days after calendar quarter-end. The public indices are rebalanced regularly, typically monthly. The public indices are market-value weighted. Cliffwater’s index is based off of SEC filings with transparency requirements. The CDLI is calculated using financial statements and other filings for the eligible BDCs (so the index’s figures are based on the BDCs’ underlying holdings), thus making it unlevered and gross of fees. BDCs whose filings are the source of the CDLI are regulated by the SEC under the Investment Company Act of 1940.

Key risks of BDMIX: This fund is actively managed, and its characteristics will vary. Stock values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to currency fluctuations, liquidity, and volatility. These risks may be heightened for investments in emerging markets. The issuers of unsponsored depositary receipts are not obligated to disclose information that is, In the United States, considered material. Investing in long/short strategies presents the opportunity for significant losses, including the loss of your total investment. Such strategies have the potential for heightened volatility, and in general, are not suitable for all investors. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility. The fund may engage in active and frequent trading, resulting in short-term capital gains or losses that could increase an investors tax liability. Short-selling entails special risks. If the fund makes short sales in securities that increase in value, the fund will lose value. Any loss on short positions may or may not be offset by investing short-sale proceeds in other investments. Investing in small- and mid-cap companies may entail greater risk than large-cap companies, due to shorter operating histories, less seasoned management, or lower trading volumes. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Asset allocation strategies do not assure profit and do not protect against loss.

Key risks of BIMBX: The fund is actively managed, and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Principal of mortgage-or asset-backed securities normally may be prepaid at any time, reducing the yield and market value of those securities. Obligations of US government agencies are supported by varying degrees of credit but generally are not backed by the full faith and credit of the US government. Non-investment grade debt securities (high yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher rated securities. Investments in emerging markets may be considered speculative and are more likely to experience hyperinflation and currency devaluations, which adversely affect returns. In addition, many emerging securities markets have lower trading volumes and less liquidity. The fund may use derivatives to hedge its investments or to seek enhanced returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

Effective 1/4/19, the Alternative Capital Strategies fund name was changed to the “Systematic Multi-Strategy Fund”. The Fund’s information prior to September 17, 2018 is the information of a predecessor fund that reorganized into the fund on September 17, 2018. The predecessor fund had the same investment objectives, strategies and policies, portfolio management team and contractual arrangements, including the same contractual fees and expenses, as the fund as of the date of reorganization. As a result of the reorganization, the Fund adopted the performance and financial history of the predecessor fund.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change. This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. Reliance upon information in this material is at the sole discretion of the viewer.

The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

Prepared by BlackRock Investments, LLC, member FINRA

©2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

Income is evolving, is your portfolio? Join industry experts as they dive into fixed income markets and a range of income strategies. Register for our next symposium, October 27 at 11 am ET. Click here.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits