Survey of Consumer Finances: Consumers Are Fine

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWe draw important insights from aggregate macroeconomic statistics. But we must bear in mind that macro trends are comprised of millions of microeconomic experiences. Questions like “How is the U.S. consumer doing?” are hard to answer concisely. We know trends in aggregate, but we can’t speak for each of the 330 million people those statistics represent. Reports that give greater detail are thus highly illuminating.

Last week, the Federal Reserve published its triennial Survey of Consumer Finances (SCF), a report that attempts to give a comprehensive and granular view of households’ financial condition. More than a simple survey, the work represents in-depth data collection and two-hour interviews with 4,602 families. The most recent edition represents consumers as of 2022, and allows comparison against the results from three years prior.

To put it mildly, the consumer economy changed substantially from 2019 to 2022. The triennial timing is fortuitous, as the scheduled skip of 2020 and 2021 keeps the most disrupted years out of the sample. The new SCF affords a good view of how differently households are experiencing the economy, pre- and post-pandemic.

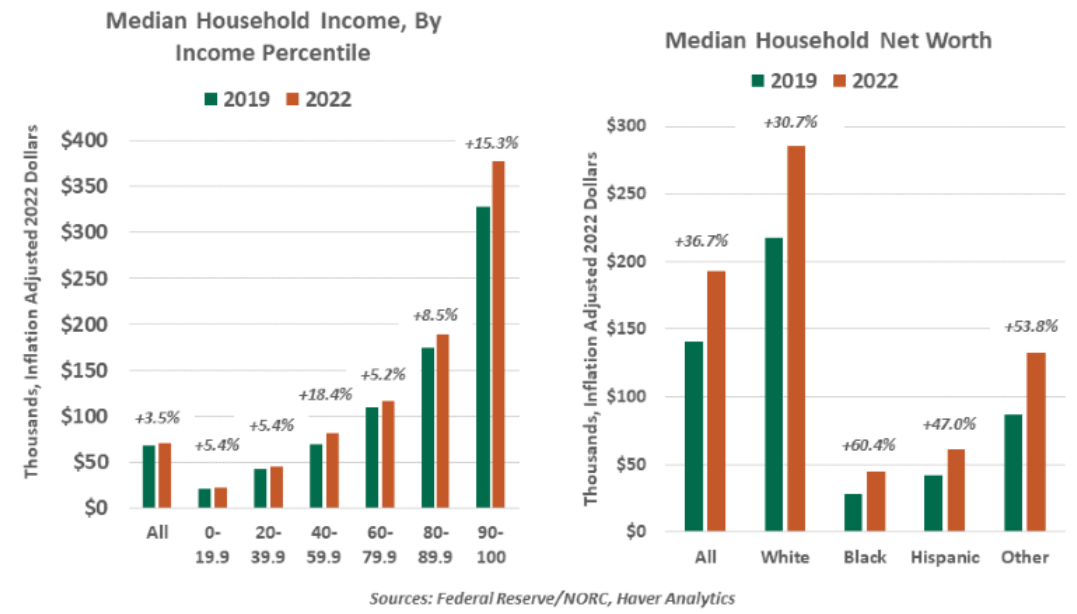

In broad terms, households are better off today. Over that three year span, median family net worth grew 36.7% to $192,900 (in inflation-adjusted 2022 dollars, a convention used throughout this article). Gains in net worth were seen across ages, levels of educational attainment and family types.

The report even showed some evidence of progress toward equality. Black households showed the greatest relative gain in net worth, growing more than 60% in three years. However, on an absolute basis, inequality persists. Black families’ median net worth of $44,900 is the lowest among the racial breakouts, far behind the $285,000 median of white non-Hispanic households. And outside of race, the long tail of wealth inequality was evident in the data. Medians are used throughout the report because high earners skew the averages; when they are included, the overall average household net worth exceeds $1 million.

Net worth is a function of assets offsetting liabilities, and those assets explain much of the dispersion in household fortunes. 66.1% of respondents are homeowners; their property brings their median net worth to $396,200. Renters do not enjoy the same vehicle for asset accumulation, with median net worth of only $10,400.

Households that own businesses also stood out for their wealth accumulation. Median net worth of business-owning households (employing at least five people) was almost ten times that of wage earners. Even sole proprietors enjoy a 25% advantage over wage earners. But the risk is noteworthy, as these categories of respondents all reported higher uncertainty about their income in the years ahead than those with conventional employment arrangements.

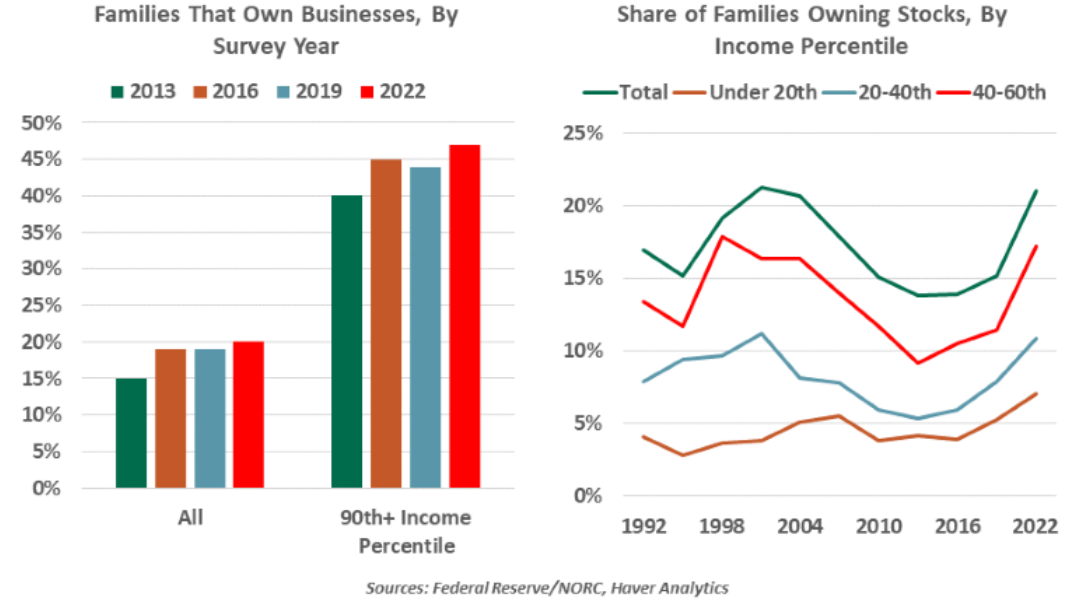

Asset ownership in general improved in this survey. In 2022, 20% of families owned a privately held business, the highest level on record in the SCF. This result is consistent with business applications data that made a level step upward amid the pandemic and has remained elevated. More consumers are creating the potential for future gains in net worth by striking out on their own.

Another pandemic shift evident in the report is the increase in households that own stock directly. The movement toward free app-based trading, the stimulus paid to consumers and greater cultural interest in stock trading has made this a more common holding, growing almost six percentage points since 2019 to 21% of households. Growth was most noticeable among younger and lower-income households. The value of stock holdings per household did not grow in tandem, perhaps reflecting the difficult equity market conditions of 2022. While some newcomers to stock trading were seeking short-term gains, we hope these brokerage accounts provide a lasting savings vehicle for a wider set of households.

Speaking of savings, the share of households with retirement accounts reached a new high of 54.3%, with the median real value of holdings climbing to $86,900. Though there is still room for improvement in participation, this trend reflects some combination of more forethought by savers and more benefit availability from employers, both of which are welcome trends.

On a cash flow basis, consumers are also getting ahead. Median income across all households rose 3.5% to $70,300. Lower-earning households saw real gains exceeding 5%. Strong labor markets have clearly helped those on the lower rungs of the income ladder.

Household earnings grew while debt declined. The median values of mortgages and auto loans fell slightly from 2019 to 2022, while student debt balances held steady in the pandemic freeze. The minor increase in mortgage debt during an interval of major house price appreciation helps explain why homeowners show such strength in their overall net worth.

The lag of the SCF is important. Its insights are a year old. The year to date has not continued the gains of the pandemic: excess savings are depleted for most households, while credit balances are on the rise. Still, recent income gains have exceeded the rate of inflation, and labor markets are still thriving. The peak of consumer optimism may have passed, but most households are not struggling.

The pandemic threw many households off, but the SCF shows that most have recovered very well. The report offers additional background on why U.S. consumers have been so resilient in 2023. We hope that prosperity will continue to grow and expand, but we’ll have to wait three more years for the next SCF to see if our wish comes true.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All