David Dali, Head of Portfolio Strategy, provides his 12-month outlook for global equity markets.

Higher Rates For Longer Delays a Recovery in Sentiment

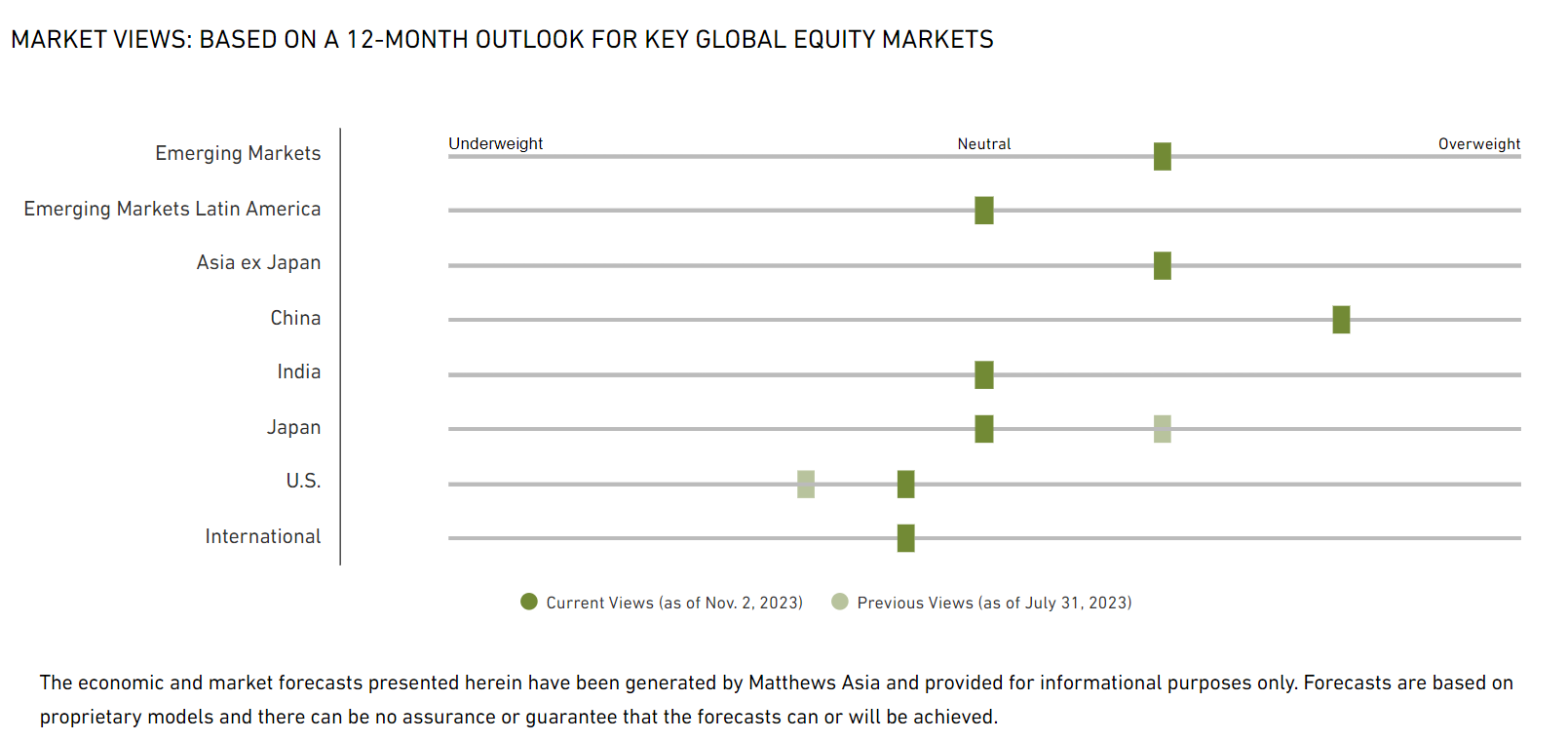

Emerging markets face headwinds from persistent developed-market inflation and the Federal Reserve’s pledge to maintain tight monetary conditions. While the Fed’s ‘higher for longer’ rate strategy may continue to dampen sentiment, China could prove a bright spot as the government ratchets up policy-induced stimulus which should underpin consumer activity and mitigate further property-sector shocks.

Emerging Markets

- Emerging markets (EM) have been suppressed as China’s weaker-than-expected post-COVID recovery and a volatile geopolitical environment weigh on sentiment while their economies feel pressure from the Fed’s ‘higher-for-longer’ strategy. Still, China continues to make policy moves to address its economic challenges and a steady cadence of corrective actions has strengthened my conviction that Asian and EM equity allocations may outperform in coming quarters.

- I’ve maintained my Latin America view at neutral given the vulnerability of the region’s largest economies to a potential global slowdown. Tight monetary policy may dampen economic activity but should support the region’s currencies.

- I’m still positive on Asia ex Japan where I remain a slight overweight. As China’s challenges recede, stronger economic growth and a recovery in consumer confidence should support imports from South Korea, Taiwan and Association of Southeast Asian Nations (ASEAN) countries, providing some ballast should a global slowdown take hold.

- China remains overweight as the government has stepped up policy moves to address the current crisis of confidence especially within the property market. At the corporate level, lower stock prices are making valuations increasingly attractive as analysts upgrade forward-looking earnings expectations from this year’s low base. U.S.–China geopolitics have also steadied as recent diplomatic visits show willingness from both sides to engage. Further progress could be made in Xi Jinping’s meeting with President Biden at the Asia-Pacific Economic Cooperation (APEC) summit this month.

- In India, economic growth remains robust and the country has a long runway of potential growth. However, I’m keeping my neutral view. There are several near-term risks to consider including elevated valuations of Indian equities, inflation risks prompting another round of interest rate increases, and the general elections in 2024.

Developed Markets

- Japan is benefitting from a return to reflationary GDP growth and government pressure on undervalued companies to increase payout and buyback ratios. That said I’ve downgraded my view to neutral from overweight given the commitment of other developed markets to tighter-for-longer monetary policy, the potentially disruptive unwind of Japan’s yield curve control (YCC) policy, and Japan’s export vulnerability to a slowing global economy.

- U.S. economic resiliency to rising rates and tighter credit continues. However, the Fed’s recent comments carry mixed signals, suggesting the lagging effects of tighter policy have yet to be fully realized. I have upgraded my view to a slight underweight as valuations have yet to fully price in ‘higher-for-longer’ policy implications.

- I’ve maintained my underweight on developed international investments, with the exception of Japan, due to tightening financial conditions and lower earnings-growth consensus. Additional headwinds include continued volatility in energy prices and the impact of the wars in Ukraine and the Middle East.

David Dali is Head of Portfolio Strategy at Matthews. David serves as a macro thought leader and as a proxy for portfolio managers, providing insights and analytics to clients. He has spent much of his career allocating and investing in equities, fixed income, currencies and derivatives.

Notes

Emerging Markets is based on the MSCI Emerging Markets Index, which captures large and mid cap representation across 24 Emerging Markets countries. Constituents include: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

Emerging Markets Latin America is based on the MSCI Emerging Markets Latin America Index, which captures large and mid cap representation across five Emerging Markets countries in Latin America, including Brazil, Chile, Colombia, Mexico, and Peru.

Asia ex Japan is based on the MSCI AC Asia ex Japan Index, which captures large and mid cap representation across two of three Developed Markets (DM) countries, excluding Japan, and eight Emerging Markets (EM) countries in Asia. DM countries include: Hong Kong and Singapore. EM countries include: China, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

China is based on the MSCI China Index, which captures large and mid cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs).

India is based on the MSCI India index, which is designed to measure the performance of the large and mid cap segments of the Indian market.

Japan is based on the MSCI Japan index, which is designed to measure the performance of the large and mid cap segments of the Japanese market.

U.S. is based on the MSCI USA index, which is designed to measure the performance of the large and mid cap segments of the U.S. market.

International is based on the MSCI World ex USA index, which captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries-- excluding the U.S. DM countries include: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the U.K.

IMPORTANT INFORMATION

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky and volatile than investing in large companies as they may be more volatile and less liquid than larger companies. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Matthews Asia

Read more commentaries by Matthews Asia