Both supply and demand of workers will prevent a surge in unemployment rates.

Not long ago, a group of my friends were discussing the worst aspects of taking a trip by airplane. While some bemoaned slow security and stiff seats, one friend offered that the start of the descent was most uncomfortable. For him, the shift to a downward path triggers the risk of air sickness.

I recognized that feeling—not just through my sweaty-palmed recollections of rough descents, but in my reaction to the October U.S. employment report. After more than a year of flying high, the labor market has changed trajectory and created some discomfort.

The October Employment Situation Summary revealed a gain of 150,000 jobs. On its own, that would be a fine figure, but it was offset by a downward revision of 101,000 payrolls to the strong readings in the prior two months. A fall in employment in the household survey pushed up the unemployment rate to 3.9%.

Details within the report revealed further causes for worry. The share of workers holding multiple jobs reached a cycle high of 5.2%, suggesting that more people are taking on second jobs to make ends meet. The number of workers employed part-time for economic reasons (not by their own preference for part-time work) reached an 18-month high. Average weekly hours worked in the service sector stepped down to a post-pandemic low of 33.2, suggesting slack capacity and unproductive labor hoarding. And keen-eyed observers noticed that total employment may have declined if not for an upward seasonal adjustment to estimated business births.

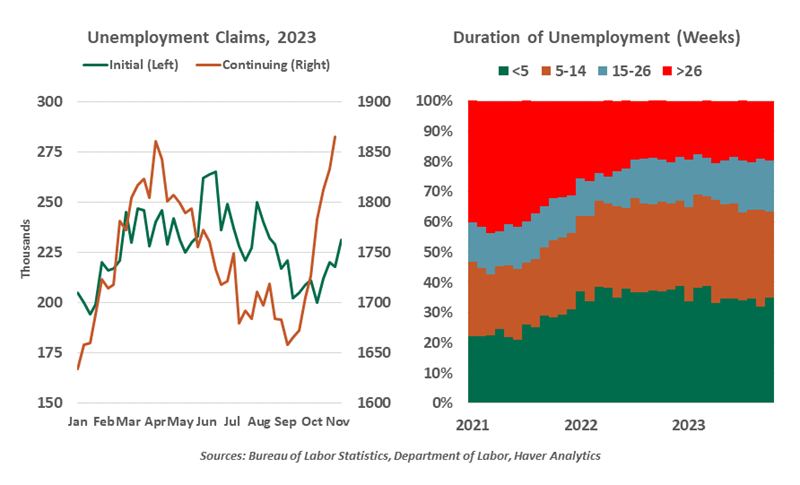

Once a job is lost, it is harder now than last year for job seekers to find their next role. The share of workers unemployed for 15 weeks or longer has gradually climbed to 36.5%, a five percentage point rise since March.

A broader view of employment readings supports the conclusion that the labor market has passed an inflection point. The Job Openings and Labor Turnover Survey (JOLTS) has been widely cited in this recovery cycle as the proxy for excess demand for labor. At its peak, JOLTS estimated job openings were double the number of unemployed persons. Today, job openings remain historically elevated, but job seekers are not having an easy time. The rate of hiring has held flat for three months, and monthly hiring activity has fallen 14% from a peak in November 2021.

The JOLTS panel, like other government surveys, has been impacted by low response rates, introducing more noise and risk of error in official estimates. Alternative data about job openings shows a cooler trend. Indeed’s Hiring Lab publishes a real-time index, which shows job openings in the U.S. have been in a gradual decline in the year to date. LinkedIn also reports a 23.8% decline in hiring over the past year, evident in nearly all sectors.

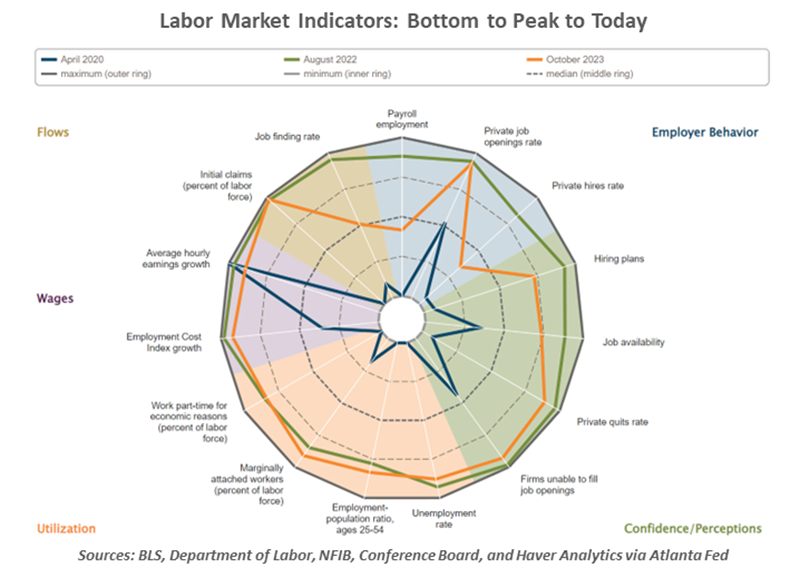

The ”spider web” chart above summarizes the evolution of labor markets since the pandemic began. No single indicator provides a complete picture; the display summarizes fifteen of them, connecting current positions to form an orb. The proximity of the line to the perimeter of the circle gauges the strength of employment conditions.

The blue horizon at the center represents the worst of times, April of 2020. The green line represents peak conditions for this cycle, August 2022. The orange line highlights where we are today, which is not in a bad position at all. Only the pace of monthly job gains and the hiring rate show a noticeable gap from the summit.

The Conference Board’s Consumer Confidence survey asks respondents (in any employment status) whether they perceive that jobs are easy or hard to get. The net share reporting jobs are plentiful has fallen to 39.4%, from a record high of 56.7% in March 2022.

Unemployment insurance claims do not yet show major stress. Initial unemployment claims across all fifty states are holding at very low levels, comparable to the strong labor markets of 2018-19. However, continuing claims show the struggle of those who have lost jobs, edging upward for the past two months.

The discussion of negative developments should be kept in the context of a labor market that is still strong overall. Record numbers of people are employed, and wage gains have exceeded inflation for several months. Prime-age (25-54) labor force participation is holding near 15-year highs, led by employment gains among women and minorities. An unemployment rate below 4% is nothing to complain about, and layoffs are limited. Every journey will involve a descent, and it need not be rough. How will we discern whether we are at risk of missing the runway?

Recessions are only formally identified in arrears, when the start of a widespread decline in economic activity can be pinpointed. The economist Claudia Sahm has suggested that a recession is underway once the three-month moving average unemployment rate rises 0.5 percentage points above its recent low. We are not there yet, but the “Sahm rule” is in play: the moving average of 3.8% is 0.33 points above its spring lows.

Though Sahm stands by her work, she also has noted that the rule is simply a historical pattern. Her research was meant to help governments start countercyclical stimulus programs in a timely manner, not to be a perfect harbinger of economic cycles. So much about the current cycle has been without precedent; pandemic extremes have rendered past economic patterns less useful. We remain confident that higher levels of unemployment will not trigger a downturn.

For many who suffer air sickness, symptoms end as soon as the plane stops moving. Queasy travelers welcome a soft landing. We will as well.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust