Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

The mounting fiscal deficit is becoming a louder topic. A deficit can be economically problematic on many levels and its financial hemorrhaging can reach far into the future. It is not as simple as it seems especially given the controversial view concerning its peril and potential solutions. How do repeated deficits and consequential growing debt affect investors? Are there hidden agendas that seek to solve an immediate requisite regardless of future costs? Let’s look at the influences and components of a deficit through the lens of the data and debates that may allow you to gauge the gravity of the situation.

Fiscal Policy versus Monetary Policy

The growing debt, covered by media outlets, typically refers to our national debt. Fiscal policy denotes the actions of the federal government. This is primarily the collection of taxes (the revenue side) and the government’s spending (the liability side). Spending is intended to be on behalf of U.S. citizens' health, welfare and security. The government spends money in many areas which include: defense, Medicare, Social Security, and interest on the debt.

Monetary policy is set by the Federal Reserve System (Fed) which is the central bank of the United States. The Fed has two primary mandates: 1) to maintain stable pricing and 2) to maximize employment. These mandates are carried out through a variety of actions which include setting the Fed Funds rate (the rate at which depository institutions lend reserves to other depository institutions – usually overnight) and influencing the supply of money in circulation.

Deficit

A deficit is created when spending exceeds revenue. A comparison often made illustrates an individual putting purchases on a credit card but not paying it off each month. When the government’s spending exceeds its revenue, it borrows money to make up the difference. This is where the comparison ends though. If an individual’s debt gets too high, it eventually concludes with creditors’ unwillingness to lend more money, and perhaps even leading to a declaration of bankruptcy. The U.S. government borrows money by issuing new Treasury bonds, collecting the proceeds and using the money to pay what it owes. As long as investors are willing to purchase Treasuries, the U.S. government has a willing lender. The problem is that the issuance of new Treasury securities adds to the nation’s debt. A debate exists as some pundits insist that this process can lead the nation to bankruptcy while others argue that printing new money may not have limits.

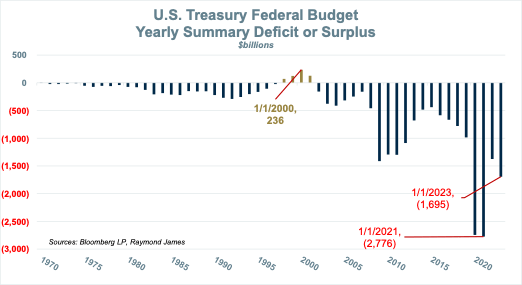

The pandemic brought about record-breaking borrowing levels pushing the nation’s deficit to over ($2.7) trillion in 2020 and 2021. With one month left this year, the deficit is near ($1.7) trillion. The last decade of consistently high deficits has increased the nation’s overall debt as new securities have been issued to pay the deficits. These Treasury-issued securities are the equivalent of the U.S. government racking up credit card debt. Let’s look at how the nation’s debt has risen.

U.S. Total Debt Outstanding vs. Fiscal Deficit

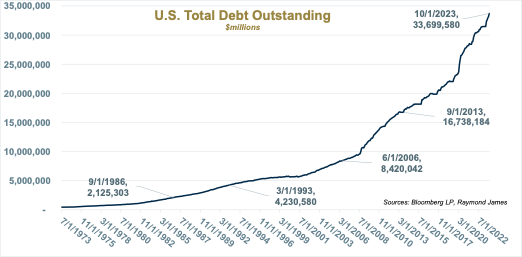

The total debt outstanding is a monthly statement of public debt outstanding for the United States. It includes securities issued by the Bureau of the Fiscal Service (Savings Bonds), Treasury Bills, Notes, Bonds and Government Account Series (debt instruments of the government that finance day-to-day operations, special infrastructure and military projects).

The fiscal deficit is as described above – the annual difference between the revenue collected and the government's spending.

It is hard for us to comprehend the magnitude of these numbers. If you paid $1 billion of this debt off every single day of this year and every single day of the following years... it would take you more than 92 years to retire the debt outstanding. If you worked an average 40-hour work week, 52 weeks a year, you would need to earn $480,769 per hour ($3,846,152/day) and do that for over 92 years.

Keep in mind that there are substantial revenues collected that match off against most of the nation’s expenses. A single year’s deficit by itself might not be problematic. It would be like buying a car and taking some of your earnings over the next few years to pay for it. Our current predicament has been mounting because the nation has not only run a deficit every year since 2002, but the deficits have been consistently massive. In 8 of the last 14 years, the deficits have exceeded $1 trillion.

Certain worldly events can trigger increased spending. The Afghanistan and Iraq wars, the 2008 Great Recession and COVID-19 are three modern-day events that did just that. We are now engaged in the Israel and Ukraine conflicts. These geopolitical events come on the heels of numerous stimulus programs enacted during the pandemic which followed a series of tax cuts. The decrease in revenue coupled with the increase in government spending yields our latest deficit. Something has to give.

The Fiscal Deficit Today

The concern of the deficit today is that it is causing the total U.S. debt to continue to grow. With higher interest rates, no plans to reduce the government’s spending and no plans to increase the government’s revenue stream, it appears this drag on the nation may continue for a prolonged period. During the pandemic, it is estimated that American savings grew by over $1 trillion. People stayed at home by choice and by imposed business and servicing shutdowns. This buffered consumers' present-day spending as their savings afforded the circumstance to spend even as inflation took the prices of many goods and services up over the last two years.

No one knows the breaking point. It can be argued that with greater debt, inflation can become chronic. High inflation eventually degrades the average standard of living since the money we earn would have less and less buying power. Should the government default on any of the debt, the credibility of the nation would radically change and catastrophically change the world’s view of the U.S. as an economic power and currency leader.

The flat stock market takes capital gains away and therefore reduces collected tax revenue. Tax collections are expected to drop ~3% versus last year. However, certain extensions and credits like the employee retention credit and student loan payments will go away as they were enacted as one-time pandemic program aids which will have no impact on tax liabilities going forward. FDIC spending on bank failures is money expected to be largely recouped and payments on loans are expected to be reinstated.

The increase in interest rates affects the budget. Last month, the Treasury reported that net interest on the debt increased to a record $659 billion this year from $475 billion last year. The more government outlay goes to servicing existing debt, the less funds that are available for entitlement and other government programs.

The ways out of this mess are: raise taxes, cut spending, produce more (grow the economy), and to a smaller degree inflation (inflation causes currency to decline – cash now is worth more than in the future – debt is paid with money worth less than when originally borrowed). There will likely need to be some combination of these to create progress. With no political compromise readily being heard, this story will continue to unfold.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Raymond James

Read more commentaries by Raymond James