Quick Read

- Insurance is making national headlines in 2023 as major providers retreat from writing new policies in large parts of the country and renewal premium prices skyrocket. Elevated asset valuations, escalating rebuilding costs, and larger and more frequent natural disasters have lowered the insurers’ profitability and are likely to result in sustained premium price hikes in the coming years.

- Insurance is a central input to the US economy. As an economically connected and highly regulated industry, the inflationary impacts of disruptions to insurance typically transmit through the economy over multiple years and that is our base case for this cycle as well.

- In our tactical multi-asset portfolios like the BlackRock Tactical Opportunities Fund, we hold a sizeable short to property & casualty insurance within our industry rotation strategy. The historical precedent for insurance industry turmoil to contribute to persistently elevated core services inflation also helps to inform our short duration position in the portfolio.

“State Farm and Allstate Exit California;” “Farmers becomes latest company pulling out of Florida;” “In Louisiana, more than 20 companies have shut down or left the state.” Newspaper headlines like these have appeared with disconcerting regularity in 2023. They call to mind the last large disruption to the US property & casualty insurance market, which occurred in the 1980s and hit the cover of Time Magazine. The 1980s insurance cycle contributed to very elevated core services inflation that concerned policymakers throughout the decade.1 We view the current confluence of challenges for the insurance industry as sufficiently large to pose similar upside risks to core services inflation and also worry about the potential impact on future government bond issuance needs.

Building challenges for insurers

In 2020, many insurers cut policy premiums in response to soaring profitability and political pressure to ease consumers’ burdens. Those lower premiums were invested into bond-heave securities portfolios at rock bottom interest rates that have since soured. That left the insurance industry vulnerable to the post-pandemic challenges of global supply chain shortages, rising physical asset valuations, higher rebuilding costs, more catastrophes, and rising reinsurance premiums. The result was that 2022 was an exceptionally bad year for insurers – industry-wide profits from the previous four years were unwound and it was the least profitable year for auto underwriting in 25 years.2

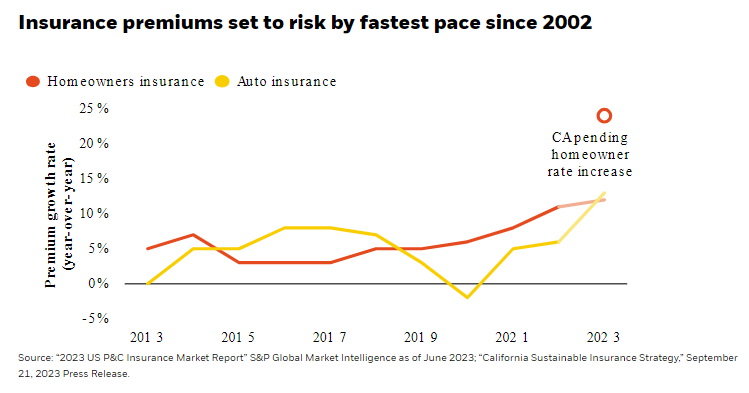

In response, the insurers have looked to regain financial footing by hiking premiums across all lines of businesses, but particularly auto and homeowner rates. Premiums are set to rise at the fastest pace since 2002 – and those estimates don’t even include large upside risks for homeowner policy premiums in California announced in September.3 If this cycle follows the multi-year dynamics of most insurance underwriting cycles, we should expect premiums to continue rising at elevated rates for the next few years until the profitability of the sector is regained. These premium rises will transmit through the economy and elevate upside risks to consumer prices.

Why is insurance so important to the broader economy?

Insurance is central to the economy since it is a necessary input for nearly every step in the production process. Our investment team uses input-output tables that map the cross-industry relationships used to produce goods and services throughout the economy to quantify industry importance. Analyzing the most granular inputs across 380 US industries, we find that Insurance Carriers rank in the top 3% of industries in share of relative importance – on par with critical industries like banking and petrochemical manufacturing. This interconnectedness helps to explain why upstream shocks to premiums and availability matter for economy-wide consumer prices.

When we look at the historical timing of the pass-through of insurance price increases to consumer price inflation, we see that homeowners insurance premium changes tend to foreshadow future inflation to the greatest extent. This makes sense since these premiums are aligned with the costs of insuring physical assets throughout the country. Delayed transmission to the CPI means that the large, impending homeowners insurance premium rises this year and next year poses future upside risks to services inflation in the US.

Potential impact on future government bond issuance

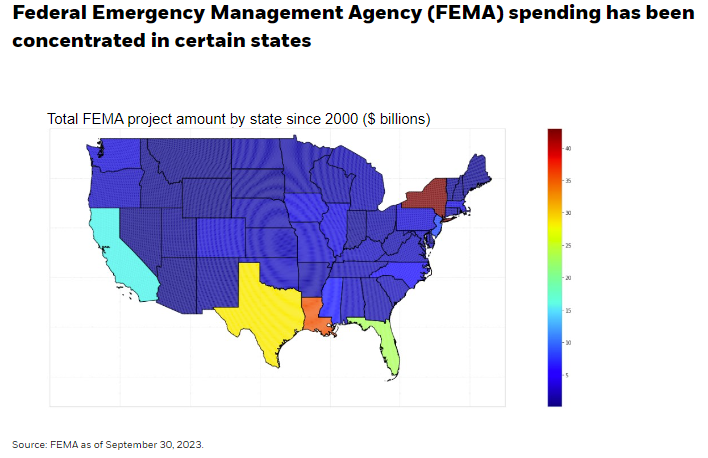

Reduced availability of private insurance will likely make more regions of the country vulnerable to the negative economic impacts from disaster events. The states where private insurers have been reducing policy availability - California, Texas, Florida, and Louisiana - are the same states that have had the highest historical federal disaster relief spending.4 Lower private sector insurance availability in those disaster-prone regions means that we should expect the public sector’s role in the insurance market to grow, which poses an upside risk for bond issuance needs in the wake of future natural disasters.

Aggregate FEMA spending data shows that the US federal government’s insurance spend has tripled in the last 10 years, with FEMA spending approximately $6 billion per quarter on average in the last few years. While this remains a relatively small share of overall government spending and overall issuance, the acceleration in government spending on disaster relief comes at a time when markets have become more concerned with the fiscal deficit. Future hurricanes, floods, or earthquakes will likely necessitate larger government backstops.

What do these views mean for portfolio positioning?

In our tactical multi-asset portfolios like the BlackRock Tactical Opportunities Fund, we seek to deliver diversifying returns that are lowly correlated with stock and bond markets. We do so primarily by seeking out relative value opportunities across different countries in both stock and government bond markets, and also across different equity industries.

Our insights on property insurance contribute to our view that services inflation will remain elevated and necessitate ”higher for longer” interest rates. This leads us to maintain a short duration position in the fund. Within our industry rotation strategy, the fund is short US property & casualty insurance. This is driven by the challenges highlighted in this article, coupled with pricing insights from our proprietary text analysis of sentiment from broker reports, which suggest that downside earnings risks for the insurance industry remain underappreciated by the public narrative and markets.

Source

1 CPI ex food, energy, and shelter averaged 5.4% over the 1980s. Persistently elevated services inflation prompted monetary policymakers to analyze the insurance cycle’s relationship with interest rates and inflation in “The Cycle in Property/Casualty Insurance,” NY Federal Reserve Bank Quarterly, Autumn 1986.

2 S&P Global forecasts that home and auto personal lines of insurance will not regain profitability, defined by the combined ratio, until 2026.

3 Prompted by the exit of many of the largest homeowners insurers from the market, the insurance commissioner recently proposed one of the largest overhauls to the country’s largest insurance market since 1988 to manage the pending policy price rises of homeowner policies that look set to rise by over 20%. Source: https://www.insurance.ca.gov/01-consumers/180-climate-change/SustainableInsuranceStrategy.cfm.

4 As an investment team with a presence in California, we’ve devoted previous research efforts to understanding how fire, flood, drought, and extreme heat impact the local economy.

Carefully consider the investment objectives, risks, charges and expenses of the funds carefully before investing. The prospectuses and summary prospectuses contain this and other information about the funds and are available, along with information on other BlackRock funds, by calling 800-882-0052 or at blackrock.com. The prospectus and, if available, the summary prospectus should be read carefully before investing.

Important risks: The fund is actively managed and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Asset allocation strategies do not assure profit and do not protect against loss. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Prepared by BlackRock Investments, LLC, member FINRA.

©2023 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

Read more commentaries by BlackRock