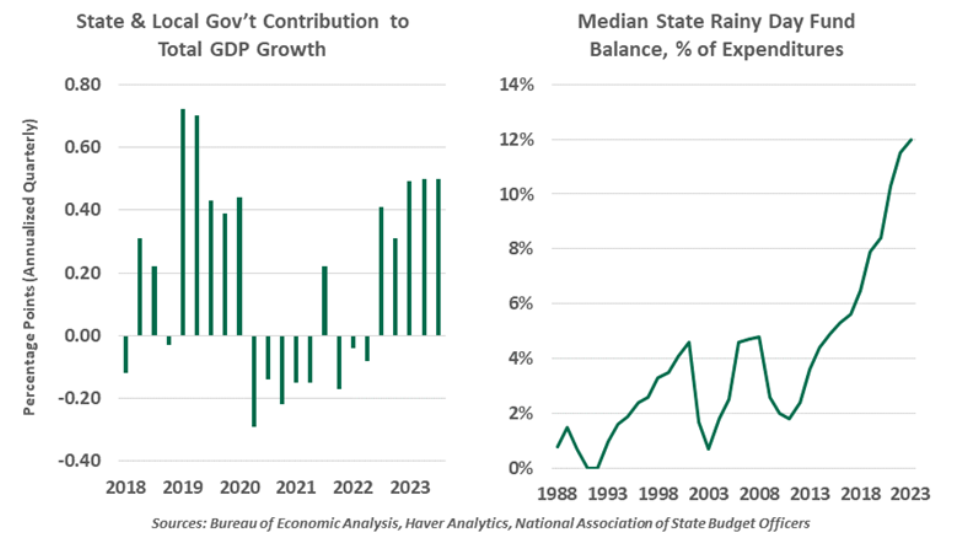

The past year of generally good economic news in the U.S. was led by strong gross domestic product (GDP) growth. One of the central contributors to this cycle has been growth in spending by state and local governments.

While much focus has been on the fiscal status of the federal government, states and localities have generally improved their fiscal positions throughout the post-pandemic cycle. We rely on these levels of government to provide critical public services like safety, road maintenance and education. And unlike the federal government, these entities cannot support their obligations by issuing currency; sustainable finances are important.

State governments take in the majority of their revenues through taxes on sales and income, as well as direct charges for services like vehicle registration and university tuition. States also receive federal funding to administer programs like Medicaid and public schooling. Local governments, meanwhile, receive much of their funding from property taxes.

Across all these funding sources, the booming post-pandemic economy has been supportive of higher government revenues. Elevated consumer and business spending supported sales taxes and fees; booming employment and wage gains accreted to income tax receipts; and higher property values led to larger property tax assessments.

On top of these cyclical boosts, state and local entities saw their funding lifted by temporary pandemic support. Federal supplements for public health, Medicaid, unemployment insurance, public transit, infrastructure and small businesses added to the resources available to state and municipal treasuries.

The added funding improved states’ financial balances; several saw credit rating upgrades. While many of the challenges that have pushed states into difficulty in recent decades are structural and long-running, like underfunded pension programs, the stimulus helped to put strained states on firmer footing—thanks in part to more transfers from the federal government.

While the sources of funds increased rapidly, the uses of funds did not increase at the same pace. All forms of federal COVID relief funds were allocated and disbursed in a hurry, to do the most good at the moment of greatest need. The temporary state programs they funded stretched for longer durations, and states had more time to apply the funding. This has left government treasuries with favorable balances, and all states have added to their fiscal buffers, also known as rainy day funds.

While welcome, the boost is not permanent. As of the end of 2022, 87% of states’ Fiscal Relief Funds had been allocated, and all COVID funds must be spent by the end of 2026. Temporary programs are already unwinding, such as Illinois’ decision to end its waiver of grocery sales taxes. Coupled with the student loan payment resumption and earlier terminations of the federal expansion of nutrition assistance and Medicaid eligibility, the return to the old normal of living expenses has been difficult for households on the margin.

Some entities are facing fiscal cliffs, as temporary federal funding is still a vital lifeline. Public transit agencies have thus far avoided drastic fare increases and service reductions due to federal support, but many will have difficult decisions when budgeting for the next few years. Dollars allocated to infrastructure investment are meant for major new projects and rebuilds, not for operations and maintenance.

As we discussed in our review of household finances, the economy is returning to normal, but normalization will include unpleasant outcomes like more expensive borrowing and higher delinquencies. States are still enjoying a temporary reprieve from budget worries. The spenddown of COVID stimulus will bring back some familiar headlines of fiscal stress. Sustained growth and healthy economic activity will be needed to limit the pain of the transition.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

More 529/College Planning Topics >